Progressive New York Magazine columnist Jonathan Chait writing for the leftist New Republic in 2010 prophesied that if the Republicans took Congress that year and Obama won a second term two years after, “the House will vote to impeach him before he leaves office.” He was confident enough to make such a prediction because that is post-Nixon politics; they got our guy, we’ll get your guy. After Clinton’s unsuccessful turn of being the next “your guy”, we spent the eight Bush II years listening to all the same Hitler comparisons while the D’s dreamed up ways to impeach W, hoping to at least pin some “war crimes” to his record.

What Chait wrote in 2010 about Obama wasn’t truly about Obama; it was the rather obvious statement of the state of American politics.

Wait, you say. What will they impeach him over? You can always find something.

I really don’t mean to make politics intrusive in this way, not the least of which because in my view there isn’t nearly enough difference R to D, or D to R. They fight each other for turf and nothing changes as a result.

The flurry of hysterics today forces at least some political equation to be front and center for our analysis. It may seem like markets are increasingly uneasy about a Trump impeachment, but I think that is the wrong political framing. Putting growing market pessimism into the context of “reflation”, what is more likely driving anti-reflation today in particular is not that Trump may be gone by vote of Congress but rather that he will be seriously wounded politically such that all the various things “reflation” was counting on are less likely to ever happen.

Tax reform? Impeach Trump. Replace Obamacare? Impeach Trump. Gutting the regulatory state? Impeach Trump. Democrats under that glare of mainstream media perspective will be hard pressed to work in any bipartisan consensus to do what is really necessary. Reform the global monetary system? It was a dream of a dream long shot in November, now there is no chance at all. I doubt there is any way the President could even fire Janet Yellen now, not that it would really matter.

From the bond market to eurodollar futures, this is really about “reflation” potential, where the politics is perhaps a larger part of it than it had been in, say, 2013. If Obama had been so seriously weakened at that time, would it have made any financial or economic difference? Not really. There still would have been ongoing QE3 and that in all likelihood would have still led to the same “reflation” trends as they were; deserving the quotation marks and all.

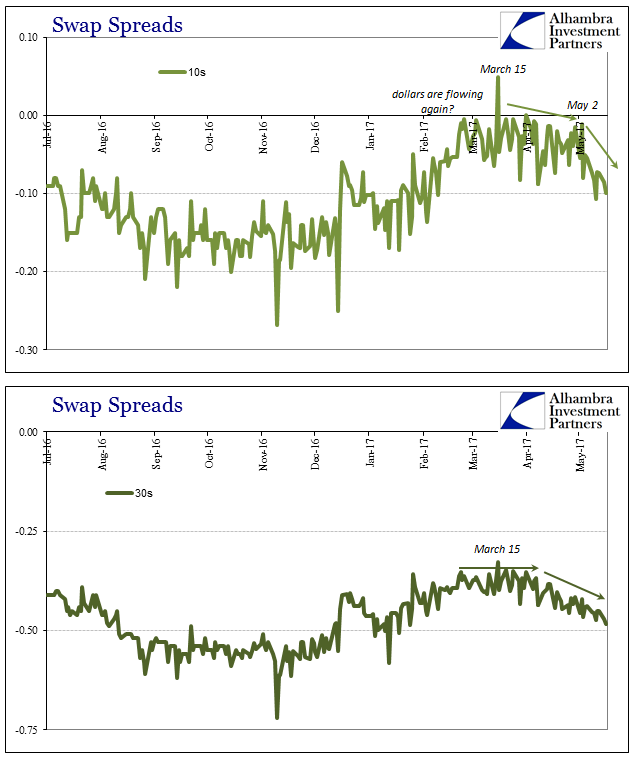

The most recent anti-“reflation” trend dates back to March 15, which is a date that holds no political significance. It is, instead, related to far more concerning monetary shifts, though not related to the Federal Reserve and monetary policy, either. As noted yesterday, China is on the clock with CNY, meaning they have put the rest of the world on an unknowably long countdown to who knows what. While we can’t possibly predict the length, we still can easily observe its presence.

Throughout the first few months of this year, derivative conditions and spreads attenuated in various facets; cross currency basis swaps, particularly yen to dollar, decompressed sharply likely as a result of Japanese banks growing tired of being the center of “dollar” dysfunction (thanks China). Interest rate swap spreads, the difference between the quoted fixed leg swap price and the same maturity US Treasury yield, likewise decompressed indicating a small improvement in offered balance sheet capacity (the real global money supply of the eurodollar system) from the big dealers. Some attempted to make more of this than what it was, again, small improvement, but overall it was “reflation.”

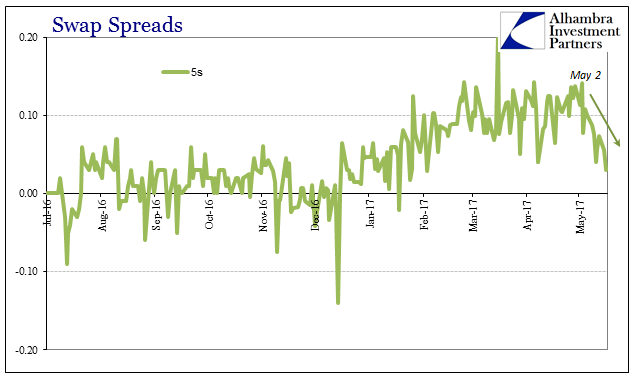

In late February, swap spreads, at least, abruptly halted their decompression. By March 15, the date of China’s probable “ticking clock” striking zero, they started to compress (meaning more negative) all over again. On May 3, that slightly more negative trend picked up pace, including at the 5s which are now threatening to dance with zero all over again for the first time since the “ticking clock” started back in mid-December.

James Comey was not fired as FBI director until May 9, so it is difficult to associate this “dollar” tightening, which can be construed as unease, as the two go hand in hand, with Trump’s political status. The combination of swap spreads along with eurodollar futures tells us instead that the real money markets (again, balance sheet capacity) are being squeezed by something and that the intermediate and longer term implications of resumed “dollar” problems create an outlook more like 2015 than what was supposed to happen in 2017, maybe 2018 at the latest.

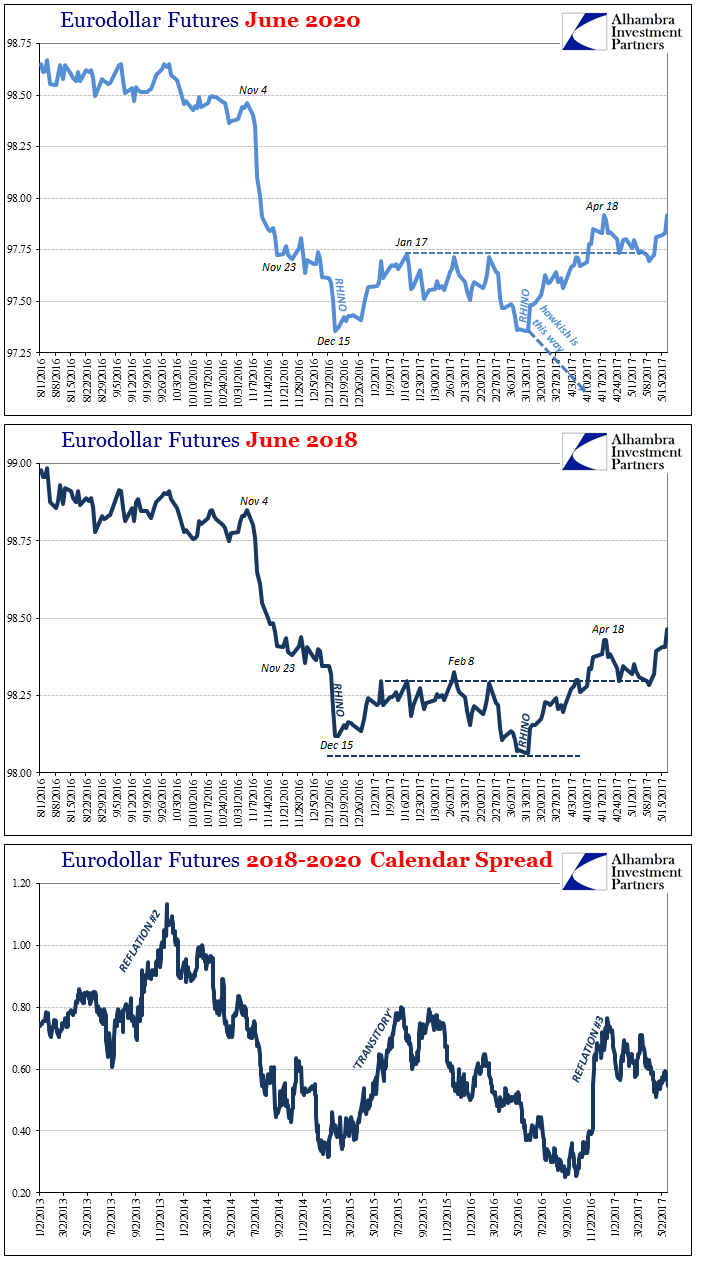

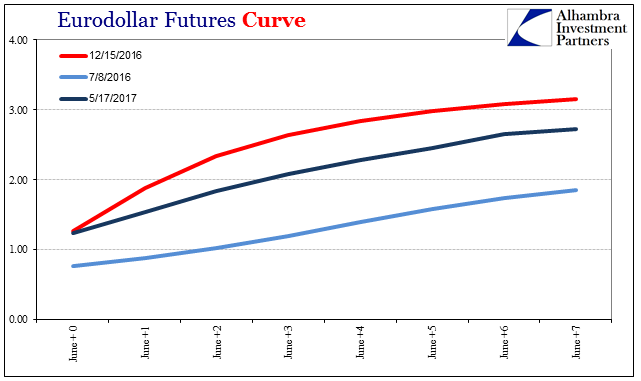

The eurodollar curve is perhaps the best illustration of the turn back toward last year’s mid-year pessimism. Though nominally prices are lower across the board, the curve shape is far more reminiscent of last July than last December. The Fed may “raise rates”, but it doesn’t really account for much beyond the extreme front end (and not even as much there as is always claimed).

“Reflation” is struggling largely because there wasn’t really all that much to it to begin with. Sure, it was more so about what could go right tomorrow, but even so it had to bear some relationship with today. The economic and monetary circumstances of today aren’t really any different than they were yesterday, a harsh and hugely disappointing reality but true nonetheless. Therefore, for “reflation” to ever work would mean it being so impressive as to overcome that immense starting handicap; when it was more likely this collective “dollar” millstone was so heavy as to bring down even the best executed non-monetary aid.

A politically isolated Trump is like smothering “reflation” in the crib before it ever gets its long shot opportunity. Nothing changes, so back and forth we go R to D, D to R while the world economy burns, and quite a few societies go up in flames with it.

Stay In Touch