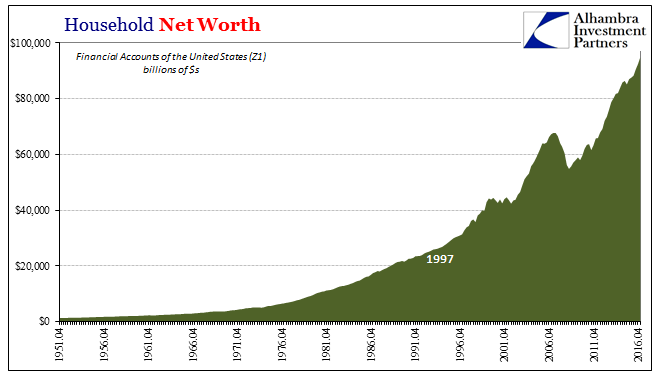

US Household Net Worth rose to a record $94.8 trillion in Q1 2017. According to the Federal Reserve’s Financial Accounts of the United States (Z1), aggregate paper wealth rose by more than 8% year-over-year mostly as the stock market shook off the effects of “global turmoil.” It was the best rate of expansion since the second quarter of 2014 just prior to this “rising dollar” interruption.

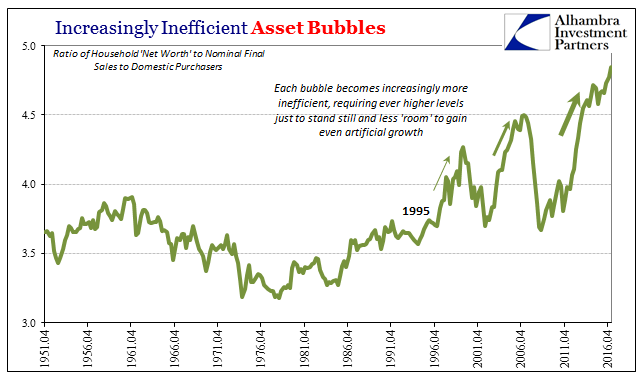

At such a high level, though, the ratio of net worth to spending has skyrocketed. That means the so-called wealth effect doesn’t appear to have any effect whatsoever. In Q1 1995, Household Net Worth was a quaint $27.3 trillion compared to $7.6 trillion in (nominal) Final Sales to Domestic Purchasers. That’s a ratio of $3.60 in “wealth” for every $1 in (nominal) spending. The latest estimates now suggest $4.85 in “wealth” for every $1 in (nominal) spending.

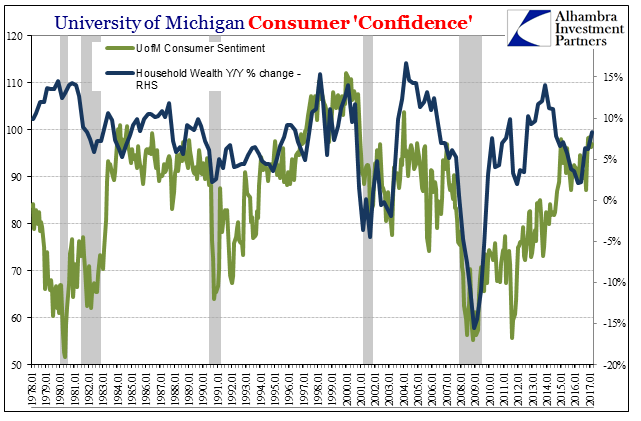

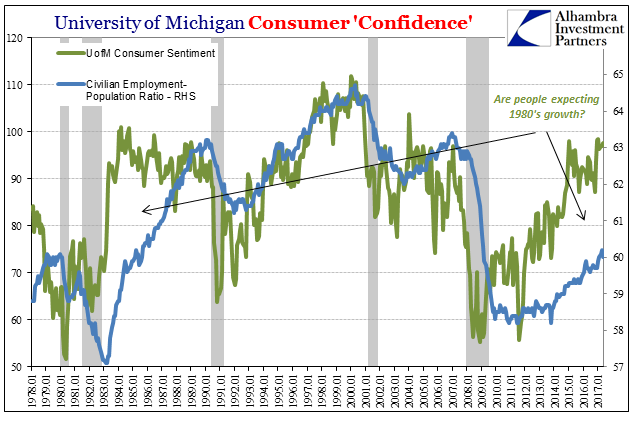

There isn’t even a detectable relationship between growth of net worth and consumer confidence. The theorized channel between asset prices, primarily, and economic growth in boosted “aggregate demand” is through the mood of households. Investors are largely consumers even if clustered toward the upper income strata, so economists believe that higher asset prices increase their confidence so as to loosen their purse strings even if otherwise they might be more cautious about spending.

The asset bubbles of late are clear enough on the chart immediately above, especially the differences surrounding the Great “Recession.” The housing bubble led to massive gains in (paper) wealth that didn’t translate fully into spending growth. And then afterward, the roaring stock market gains of the early “recovery” period were way out of line with the surveyed consumer mood. It is only recently that sentiment has caught up with wealth.

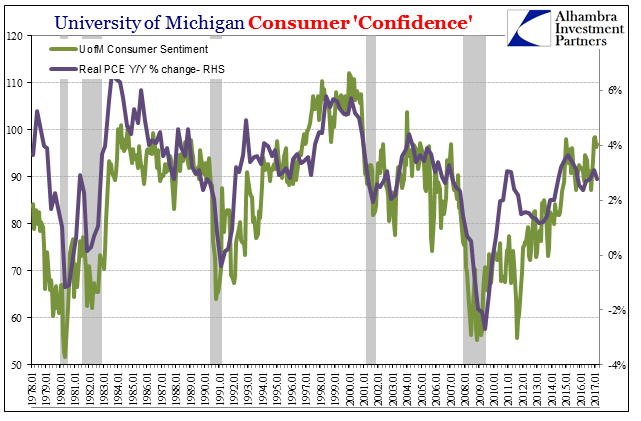

There is a much stronger relationship between at least the GDP version of consumer spending and confidence, meaning that “aggregate demand” in this channel is clearly not a product of the “wealth effect.” When then-Federal Reserve Chairman Ben Bernanke wrote on November 4, 2010, in the Washington Post justifying a second QE he was unusually explicit on this score:

And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.

The economic problem for paper wealth, consumer confidence, and then aggregate demand through stimulated spending is more than just the breakdown in that theoretical chain. None of these relationships have in the last eight years ever referenced the size of the contraction in the first place. Even the tighter relationship between Real PCE and the University of Michigan’s Index of Consumer Sentiment is misleading.

“Further economic expansion” in 2010 was an entirely different matter than it may be today. In a true recovery, which Bernanke was then trying to assure, there is a burst of unassailably high growth that makes up for the contraction immediately behind. The US economy instead resumed a growth trajectory at a lower level (reflected in lower confidence as well as spending) but without ever having filled in that great gap produced by the Great “Recession.”

In other words, these are all measures and means of describing and alleviating second order effects without ever addressing those of the first order. I know it’s a tautology but it must be stated; you don’t get a recovery without the recovery first. The focus on the post-crisis growth rate misses the point of having never addressed the crisis. It is the difference between non-linear and linear, the latter showing growth while the former demonstrating a shrunken economy still shrinking.

Thus, the disparity between “wealth” and economy will only grow so long as asset prices are largely focused on those second order changes and extrapolating them in a straight (linear) line far out into the future. In linear terms, it seems plausible that the atrocious economy of the last ten years will have to at some point just end. Rising consumer sentiment and even wealth, though unrelated, might seem to even increase the possibility. But that is really nothing more than circular logic.

Instead, the big economic problem in the first order becomes clear through other comparisons that better reflect the non-linear nature of the problem.

Because the global economy starting in 2007 was subjected to “dollar” decay and has since shrunk without many people realizing it, there are any number of drastic imbalances that present challenges of measurement or even just raw intuition. Wealth is at an all-time high while the global economy is stuck in depression, which sounds like a paradox. It really isn’t, as the deficiency in the first place starts with the incorrect perspective provided by mainstream economics, including every angle of Bernanke’s theory of “stimulus.”

People, again, know there is something wrong, but what is it? Where once there was a dot-com bubble, there is now a Depression Bubble Paradox. Two decades ago, stock investors bet on even better economic conditions without ever understanding the real nature of their contemporary economic conditions. Today, they see ahead the end of the stagnation though similarly they have no idea why there was stagnation in the first place. In both cases, valuations become so stretched wagering on a future positive (non-linear) shift that will make the present, and those valuations, nothing but minor inconveniences. We know how the first one ended, and by examining the eurodollar we have at least a rational basis to detect reasonable possibilities for the second.

Unfortunately, from that first order basis of eurodollar erosion this latest bubble isn’t likely to end in full recovery; at least not first.

Stay In Touch