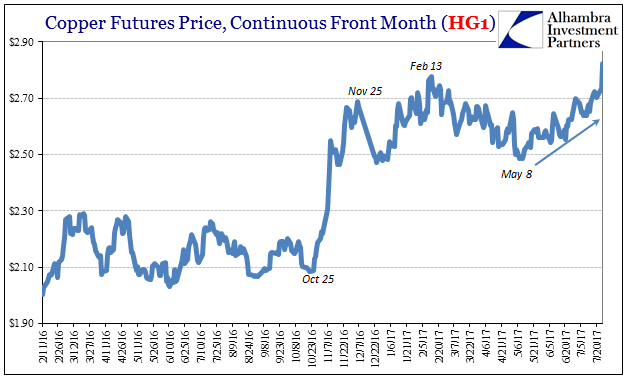

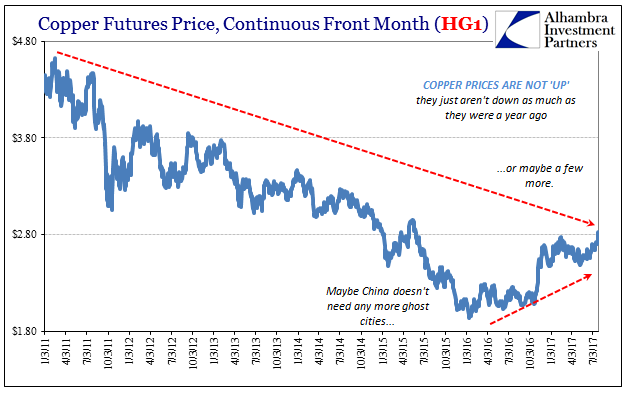

Copper prices are up very sharply today, igniting across markets a reborn “reflation.” Treasuries along with eurodollar futures have been stuck in anti-“reflation” for quite some time. Copper, on the other hand, is not just now breaking from the pack. Going back to May 9, this important economic indication has been so far steadily bucking the trend.

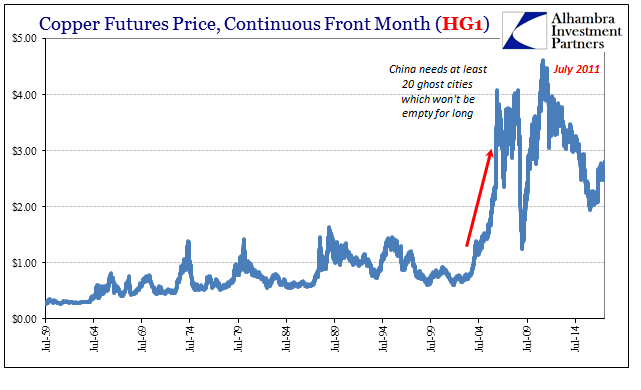

When we talk about Dr. Copper it is important to settle on terms. When the price surged way out of historical proportions back in 2005, it was assumed that was in relation to the US housing mania. But 2005 was the top of that bubble, not the start. Instead, copper was reacting to the other part of the eurodollar-driven global imbalance – EM construction, especially China.

The first of China’s so-called ghost cities was begun around that time, with Communist authorities shifting state investment toward urbanization at the fastest possible rate. From the perspective of 2005, continued rapid growth was expected indefinitely. The export/industrial engine of China’s economy required workers, meaning the migration of hundreds of millions of subsistence farmers out of the rural fields and into modern cities already awaiting them.

Thus, copper’s peak in early 2011 coincides with perceptions (including those relating to global money) about how many new “ghost cities” China might still have yet to build. If the global recovery after the Great “Recession” was to be delayed, the Chinese might not need in the foreseeable future much more by way of new construction. The price of copper is therefore in large part a proxy for China’s view of that paradigm (especially given copper’s role in construction finance as collateral).

That perspective had only dimmed through the “rising dollar” period as it was realized there was the nontrivial economic risk the world economy might not recover at all. Copper sank all the way back under $2 during the worst of the 2015-16 downturn the metal was no longer pricing as a recession.

“Reflation” in copper terms, therefore, is and so far has been about just what that might mean. In other words, how will the Chinese react to a truly changed economic paradigm?

One possibility is that authorities will be provoked to try to bubble their way out. Another is that the internal Chinese economy can replace as its center the once all-important manufacturing business (rebalancing). In both those possibilities there is required RMB. Any possible change in PBOC policy, public or not, can be a catalyst toward shifting baselines, low as they might be at this point.

Publicly the central bank is still neutral; in reality, CNY suggests something else; at least for RMB. The currency exchange rate has risen against the dollar more resolutely since Moody’s dared downgrade China’s debt back in May. But the start of CNY’s appreciation was May 9.

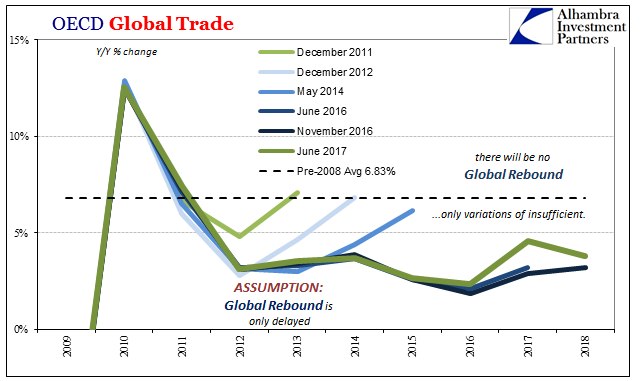

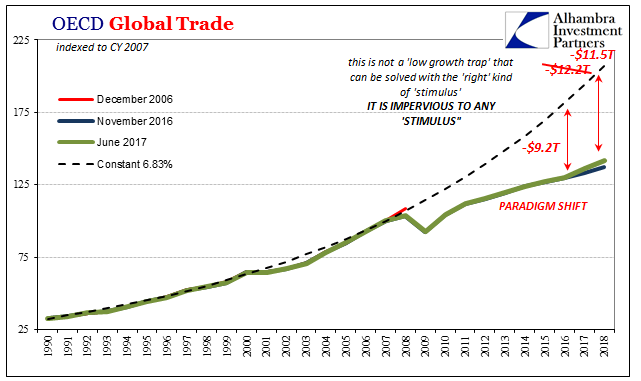

There really isn’t any other basis for copper’s behavior this far in 2017. Many if not most economic projections are still more favorable, but that really doesn’t mean all that much. The OECD, for example, raised its global trade outlook for 2017 and 2018 at its last update last month.

In November, their economic models projected $23.5 trillion in total world trade (volume) in 2017, and $24.3 trillion in 2018. As of June, those estimates were upgraded to $24.0 trillion and $25.0 trillion, respectively. A $700 billion upgrade for next year sounds terrific and surely substantial, but in context it is revealed as both a rounding error as well as a repeat of these intermittent bursts of upgraded optimism that always fail (“reflation”).

Even with minor improvement this year, the OECD does not expect it to last or more importantly to be lasting. Instead, they are projecting variations of all-around insufficient growth; some years, like this year, could be less painful than others, but stuck always way behind.

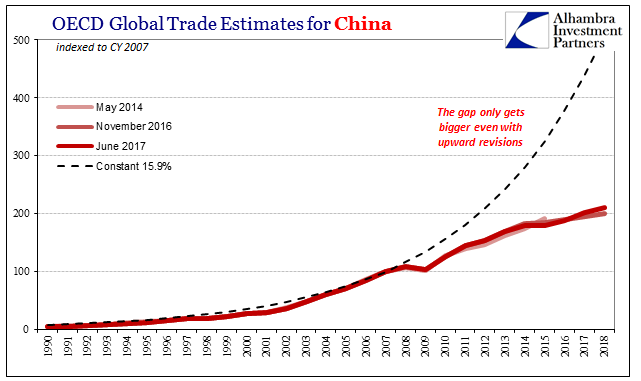

They project for China an even greater uptick in trade than the world in general. It is still not much more than a barely noticeable change, and is not expected to last much beyond 2017.

There aren’t a whole lot of new ghost cities required of the old Chinese economy in these figures (which are very likely the best case, given the history of the last decade where time and again the real economy consistently underperforms them). It could be that copper investors, like those in global stocks, see only what they want in extrapolating a lot out of a very little improvement; turning a molehill of variable deficiency into dreams of a mountain of true recovery. In that respect, central bankers and the media especially in the West have done little to deter such thinking (see: Mario Draghi, June 27).

That might be overthinking it too much. Copper prices really aren’t that far off the recent lows, like oil closer to that position than past highs. If last year the global economy seemed to warrant only a couple new Chinese ghost cities, then this year it might appear as if two or three more rather than the initially planned twenty could eventually be built. A positive RMB environment would seem to be the initial stage for it.

As usual, however, that all depends on even minimal growth levels from here being finally uninterrupted by (monetary) circumstances. We’ve seen all this before too many times, including as advised by Dr. Copper only a few years ago. From a low of just a bit over $3 in October 2011, copper at first surged ahead and then settled back into a volatile uptrend all the way until February 2013 – and the primordial conditions of what would be the “rising dollar.”

Copper, as many markets, is trying to investigate the possible upside scenario to what is global stagnation, malaise, or depression. We already know the downside, for China and all the rest.

Stay In Touch