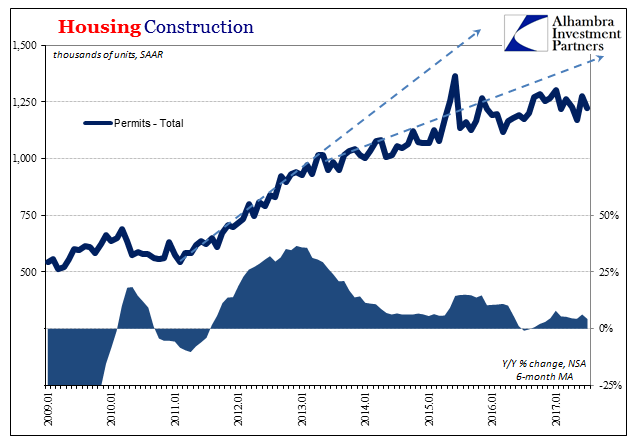

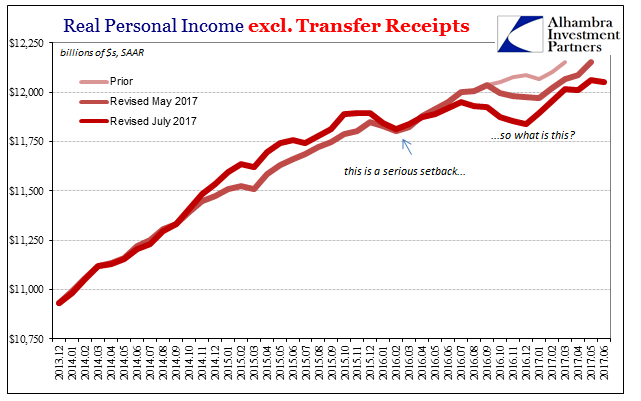

Housing construction continues to lag in 2017. Total permits in July fell on a seasonally-adjusted basis to 1.22 million. While not a huge decline, it continues to undershoot the post-taper trend that began in 2013 (after the mini-bubble wave crested from the trough of the housing bust). The break in that trend dates, unsurprisingly, to late 2015 and the near-recession downturn that developed. There has been very little growth in construction since, indicating the effects of wider macro weakness (incomes).

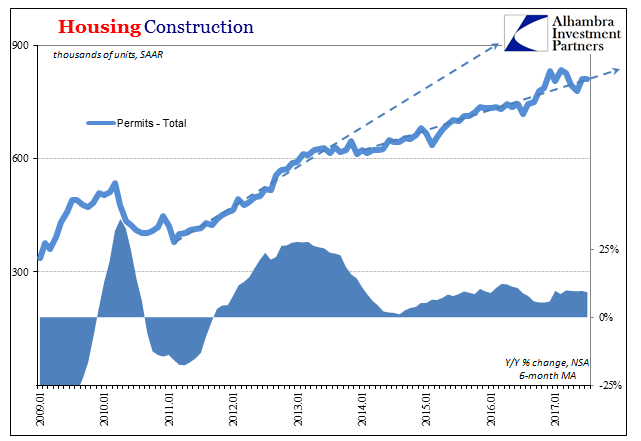

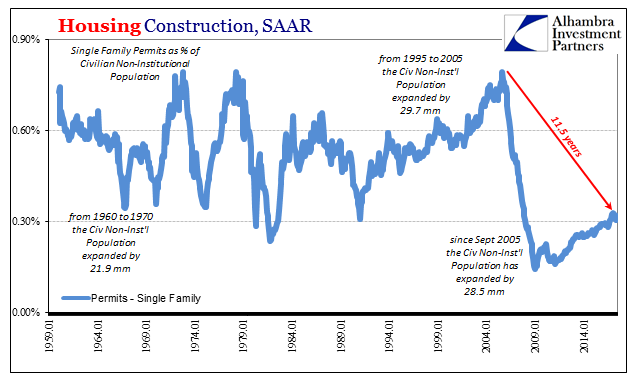

The single family segment continues mostly in a low amplitude pattern. As the bulk of the housing industry, it provides the baseline for overall conduct. The real weakness of it becomes apparent when adjusting for the population. Single family home construction was obviously overdone in the middle 2000’s, but after almost twelve years the rebound in new housing stock remains suspiciously low.

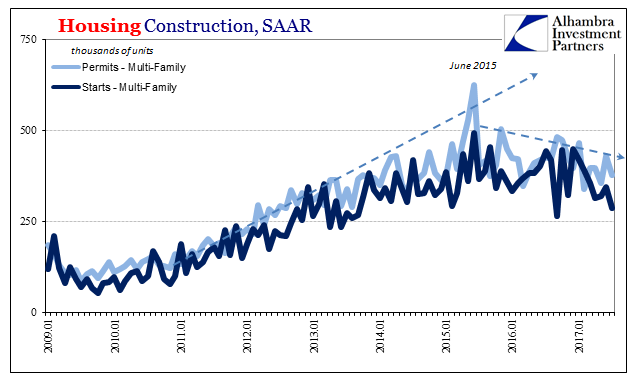

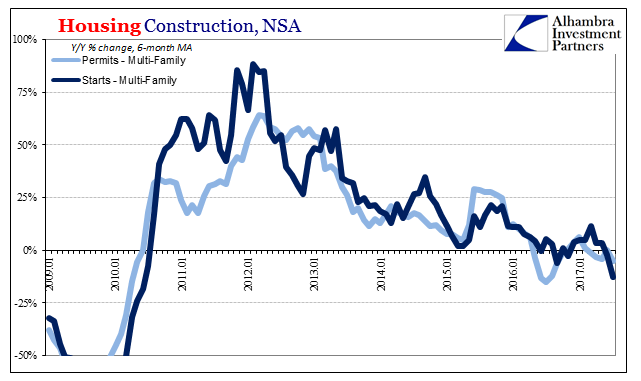

The real drag on construction recently, however, is from the multi-family segment. Going back to the summer of 2015 again, the number of new apartment projects has been steadily if gently reduced. Again, that is certainly an economic factor related to actual labor market conditions beyond the unemployment rate. The number of new starts in this part of construction industry is now declining at an average (6-month) 13% rate, the worst results since the housing bust.

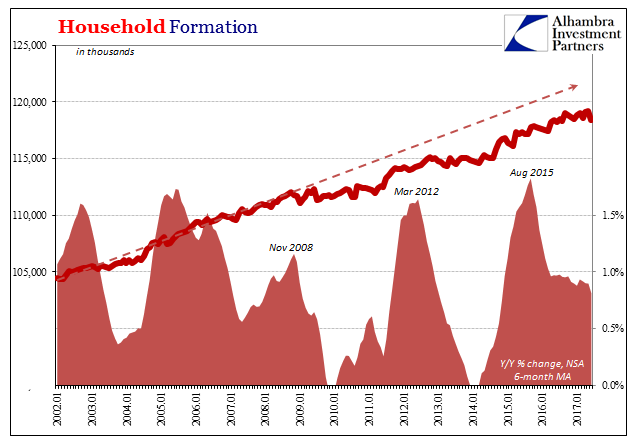

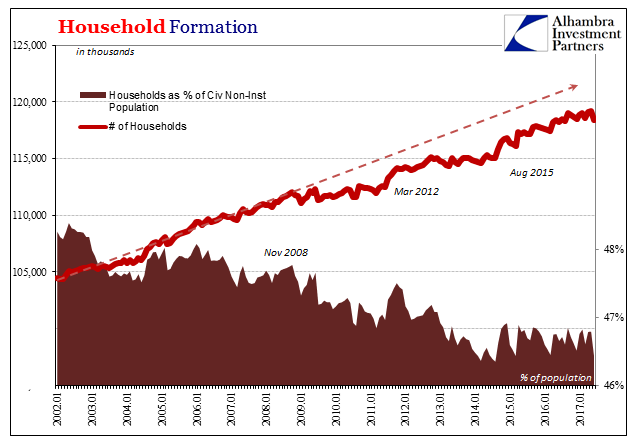

The Census Bureau gives us a further sense of this difficulty with its estimates for Household Formation. The emphasis for new homes is both a demographic as well as economic issue. While Baby Boomers may be retiring and moving out or reducing their home size, younger Americans should have been making up most if not all the difference over the last ten years.

Instead, however, the level of Household Formation and the rate at which it is growing mirrors the trend in the general labor force. Beginning at the worst parts of the Great Recession (once again no surprise), the estimated number of new households slacked off and has yet to recover almost ten years later.

The reason for that is like the rest of the economy Household Formation has largely followed the contours of the mini-cycles that have made up this “recovery” period. The near-recession in 2012 as well as the one in 2015-16 interrupted the rebound, keeping the level of total households below the pre-crisis trend (thus, it would seem, requiring less new construction for the given population).

Household Formation is again on the downswing matching the timing and pace of softening in the labor market due to the economic effects of the “rising dollar.” That must be showing up in moderating rents and rental demand, which would explain fewer new apartment additions since 2015.

This trend also coincides with the “plateau” in auto sales as well as the clear lack of momentum in the rest of the economy. Though it may not count officially as a cyclical peak, the downturn starting two years ago was clearly a serious one whose negative effects, unlike in a traditional business cycle, continue to linger. And quite different than how the economy has been described all this time, home construction is responding to Americans continuing to be worse off in absolute (long run) as well as relative terms (short run).

The stereotypical millennial stuck in his or her parents’ basement is not popular imagination, nor is it the fault of those young people becoming adults during the worst economy in generations. To the FOMC, recovery is now defined as 2% GDP growth being slightly better than the much reduced 1.8% “potential.” Actual recovery is where actual living standards and conditions materially change for the better for more than just a few. It’s been so long since that was even plausibly the case, most people have forgotten what growth was – and why so many young now find a welcome message in socialism in all its forms.

You really can’t blame them facing such a bleak future (for even those who manage to move out and up after landing a job, opportunity even for these lucky ones is not like what it once was). How might any of us respond to all this after hearing constantly that this last ten years counts officially as economic growth and recovery? If I believed that I would look for alternate political and social arrangements, too. It’s another 1930’s parallel that goes unappreciated in the coarsening and hardening of most top-down discourse.

Stay In Touch