Five days ago, the Bank for International Settlements (BIS) published its Quarterly Review letter. Contained within it were the usual articles and releases of data that accompany every issue. There was the opening piece encouraged, as always, by the “strong outlook” though puzzled how it isn’t translating into inflation. And bowing to the enthusiasm and interest in things like Bitcoins, there was an article about central banks taking a look at cryptocurrencies and the technology behind them.

Oh, and they found $13 to $14 trillion in offshore debt that doesn’t exist on any accounting statements except their footnotes (thanks again to M. Simmons).

To be specific, BIS researchers Claudio Borio, Robert Neil McCauley, and Patrick McGuire didn’t find debt so much as obligations in largely FX derivatives that are in every way just like it. As they stipulate in their study:

These transactions are functionally equivalent to borrowing and lending in the cash market. Yet the corresponding debt is not shown on the balance sheet and thus remains obscured.

Judging by the utter lack of mainstream acknowledgement and attention we might be tempted to write off the discovery as unimportant mundane trivia. That’s one way to look at it, but a more realistic one is that it’s easy to understand the implications, and they are not good for the members of the media but especially the central bankers who have informed them.

To start with, that possibly $14 trillion is on top of $10.7 trillion (again, offshore denominated in dollars) that has been found, tabulated, and then recorded. Thus, it is no small thing where borderless debt jumps from $11 trillion to $25 trillion with a mere publication. That it further takes the form of esoteric and exotic derivative contracts between parties and counterparties almost exclusively in an interbank context is another serious consideration.

Every day, trillions of dollars are borrowed and lent in various currencies. Many deals take place in the cash market, through loans and securities. But foreign exchange (FX) derivatives, mainly FX swaps, currency swaps and the closely related forwards, also create debt-like obligations. For the US dollar alone, contracts worth tens of trillions of dollars stand open and trillions change hands daily. And yet one cannot find these amounts on balance sheets. This debt is, in effect, missing.

But it’s not missing and it never was. It’s out there and it is working and doing things, playing some large, perhaps majority role in the global economic condition. These trillions can only be categorized as “missing” because the world’s monetary “experts” never bothered to look for them. That doesn’t make them missing, it shows monetary authorities as utterly incompetent and clueless. Content with their own indoctrinated ignorance, they have conducted their policies with only a third or less of the monetary picture in hand. It isn’t hard to fathom why things have turned out as they have in too often globally synchronized fashion.

If there is and was so much inside these offshore shadows, and there was always every reason to suspect there was, how do we know it’s not ruining economic growth? What supports those $25 trillion and how? Where does it all come from, because that might matter, too? As I wrote in another context today:

It’s surely far more than that [$14 trillion], too, given that this particular study is limited in its scope to just FX and derivative transactions like it. How does one calculate, for instance, the effects of negative securities lending parameters on global collateral flow? Or, the VaR effects on capital or risk budgets for any bank’s balance sheet deriving from interest rate swaps, or more so changes in their price and availability? The net result of all that might make the difference between $14 trillion hidden and a pitiful global economy, and $20 trillion and actual recovery; or $5 trillion and a repeat of something like 2008. It’s not missing debt so much as monetary math that no balance sheet was designed to catalog.

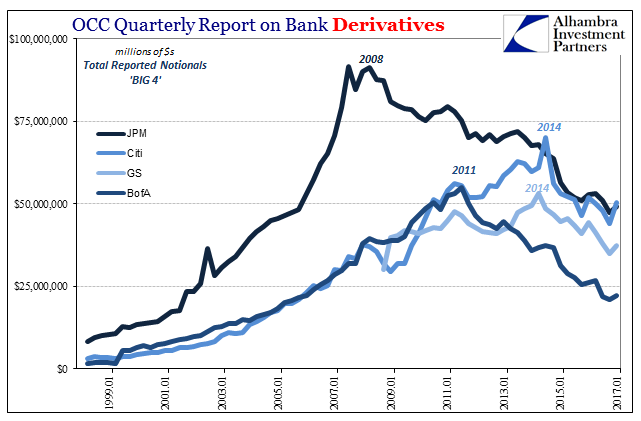

That’s ultimately the point, meaning that our current regime of just accounting statements is decades behind (see the graphic at the bottom of this post). We can’t even say that balance sheet statements are in their infancy because that is really an incorrect categorization; traditional balance sheets are perfectly mature and capable in cataloging the way the banking/monetary world worked in the 1950’s.

It is 2017 and the eurodollar system began offshore more than 60 years ago. Yet, we know so very little about it (an obvious understatement given the sudden unearthing of $14 trillion). Because of the way tradition dominates we don’t really know what we don’t know. We have no idea the size of what’s there, nor do we really know all the fanciful ways in which it all might work and fit together (or, as likely the last ten years, doesn’t fit together much anymore).

Janet Yellen can stand there adjusting her monetary levers and claim simultaneously that inflation is a mystery to her and her cohorts while also that the financial system is resilient and in no danger or malfunction whatsoever, but why should we believe her? There are at least $14 trillion, dollars, out there that she didn’t even know about five days ago; and more than likely she has discounted them as either immaterial or someone else’s problem already.

Janet Yellen as Ben Bernanke says there is no reason to suspect the monetary system for what ails the world. She does so from the position of what is on the accounting statements.

It was called in the 1970’s the Case of the Missing Money by Stephen Goldfeld. Again, it wasn’t ever really missing, nor has it been in the last two or three decades as things really got strange. It was all right there in front of anyone who might look. You just had to be good at parsing footnotes.

I may have to retire my use of the term “eurodollar” as not quite descriptive enough (which it isn’t and hasn’t been). There are tens of trillions buried within the thousands of pages of annotations and appendices that nobody reads, or if they do they overlook their significance. These are footnote dollars. They may not qualify for in the consideration of economists, but they have had far more of a hand in shaping the world as it is than a Janet Yellen could ever hope to.

Until she, too, starts reading the footnotes.

Stay In Touch