China’s Communist Party concluded the Third Plenum of its 18th Congress in November 2013. It was the much-discussed reform mandate that many in the West took to mean another positive step toward neo-liberal reform. At its center was supposed to be a greater role for markets particularly in the central task of resource allocation.

In some places, the Party’s General Secretary Xi Jinping was hailed as the great Chinese reformer. That took it too far, as Xi’s agenda in favor of markets was not really in favor of core capitalists tenets like private property. The central idea governing how Xi wishes to govern is to make Communism work better, meaning recognizing how top-down is hugely inefficient, not to move further away from it.

To many in that Congress it was too much, too far. Xi may be trying to build a better Communism but for many in powerful local Party seats it was received as some level of betrayal of sorts. The central government has encountered resistance to it over the years since then.

Whatever one’s feelings on ideological purity, these measures would not disrupt the central axis of the Chinese economy – the SOE’s (state-owned enterprises). One way to write it as a bumper sticker slogan would be, better SOE’s, better Communism.

In the nearly four years since the agenda was somewhat defined, the results have been, shall we say, far less than desirable. That isn’t really attributable to Xi’s ambitions, or shouldn’t be, instead China was at the time of the gathering of the Third Plenum already gripped by the early stages of the “rising dollar.” Within a few months, the currency exchange rate which was taken for granted for moving in the upward direction would spend instead the next few years doing the opposite and confounding pretty much everyone and everything.

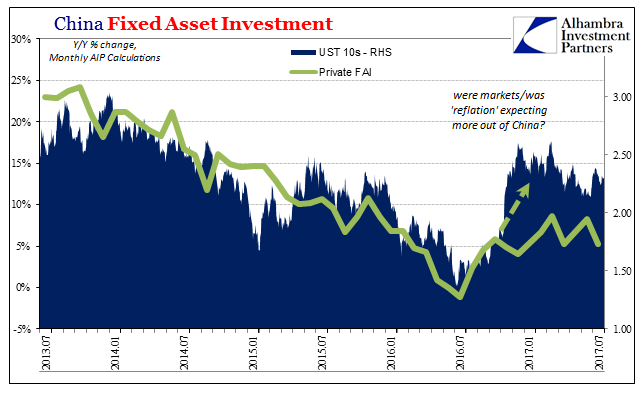

As I wrote in March 2014:

What all this data shows, as opposed to conjecture about the supernatural powers of central banks, is that yuan’s devaluation may be directly tied to dollar shortages. In fact, as I argue here, it is far more plausible that a dollar shortage (showing up as a rising dollar, or depreciating yuan) is forcing the PBOC to allow a wider band in order that Chinese banks can more “aggressively” obtain dollars they desperately need. Worse than that, the PBOC itself cannot meet that need with its own “reserve” actions without further upsetting the entire fragile system.

That proved to be exactly China’s case. The question for the 19th Party Congress set to begin on October 18 is whether or how any appreciation for it might enter China’s political calculation. There are any number of ways in which it might, including an official agenda toward CNY and the dollar.

From all early indications, it appears as if Xi is in position to strengthen his hold on the Party apparatus. He has been given, or has created (several times through the Central Commission for Discipline Inspection, or CCDI, the Party’s corruption policy), the opportunity to appoint loyalists and those with close past working relationships at all leadership levels, including the all-important local party positions. Twenty-three of the mainland’s 31 provincial regions have new Party leaders, while 24 have been given new mayors or governors.

Of those, 15 had in the past worked with Xi at various points during his career rise to General Secretary. Another 14 worked for those considered Xi’s political allies.

Therefore, the primary impediment to what is in all likelihood an intact reform agenda is not politics but reality. When the 18th Party Congress gathered, it was universally expected that China would emerge eventually as the same China in economic terms as the one that had existed and thrived before the Great (and global) “Recession.” For the 19th, there has to be a reckoning with how there is no possible path for China to get back to that state.

More than that, there remain serious downside risks even from here. It is downplayed here in the West, but when aren’t these risks downplayed here in the West? As the wonderfully named David Dollar wrote for Brookings back in April, “in the year of big political decisions, [China’s] economy appears stable.”

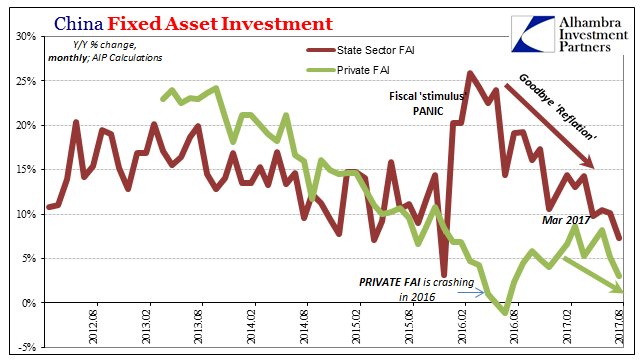

During the long slowdown of investment growth, there was always a worry of how far it was going to go. Now it seems to have stabilized at a low level. In the past four quarters, investment contributed 2.4 percentage points of growth. The other source of growth on the demand side is change in net exports.

Mainstream economic thinkers simply cannot breakout of their binary world; for them, if there are positive numbers an economy is growing, and therefore the only downside is minus signs. They cannot comprehend gradation and what that means for a place like China whose demographic challenges we cannot even begin to understand from our own experience. They must grow or face far more political instability than what we can imagine; in many ways, the Chinese system is so very fragile but for its economy.

Not only is China slowing in population, its population is aging. This kind of demographic shift requires allocating far more resources to non-growth oriented services like healthcare, while also changing the nature of China’s workforce. These sorts of massive challenges are far easier to face when your economy grows at 20% faithfully than when it struggles to get 7% (including serious questions as to the veracity of that 7%).

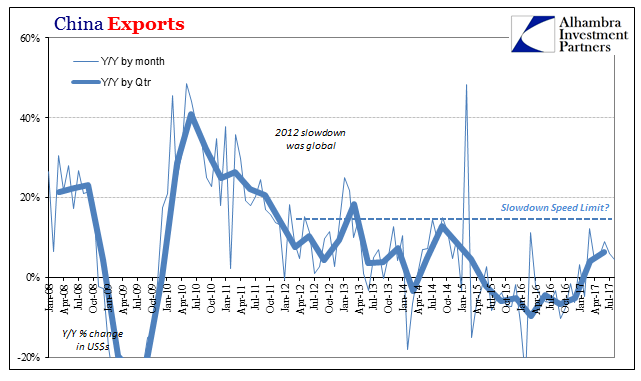

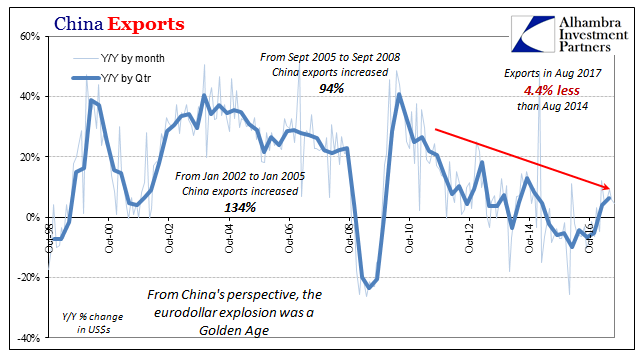

And their economy continues to get no help whatsoever from “global growth.” It was fashionable earlier in the year to mistake a minor shift in sentiment for a meaningful change in the global economic condition (as Mr. Dollar did). Several months on, it is increasingly clear if unsurprising to find even the small improvement did not spark anything greater than small positive numbers (China’s exports in August, for example, rose just 4.5% year-over-year).

I believe that is why officials in China have turned toward a new CNY policy, or at least emphasis. It’s not a peg like the central bank had enforced before, because a peg would be both a betrayal of Xi’s agenda while at the same time, I think, practically impossible to enforce (too costly). They are trapped in a small corner but for that one mistake – believing in 2009 and again in 2012 that the global economy did, might, or could actually recover. Now China proceeds from a much weaker position, already beset by enormous inefficiencies (including bubbles) delivered by the orthodox textbook response to a recession that wasn’t a recession.

Unlike the sharp state of denial that prevails here and in Europe, I don’t believe China has surrendered to the illusion central bankers have perpetrated elsewhere. They can’t afford the luxury of fooling themselves the way Economists have. It will be interesting to see if that changes much or anything next month.

Stay In Touch