I wrote earlier today that I believe Ben Bernanke one of the smartest men around. Whatever you might think of the usefulness of his career work, it is quite clear it was accomplished with some great talent. He occasionally offered some good, novel insight.

I’m not so sure about Janet Yellen. While her trademark deer-in-the-headlights look could have been explained as the profile of an uneasy public performer, the track record of her work even in academic Economics terms has been unremarkable. Her contributions to FOMC policy meetings, for example, show little other than those of a faceless bureaucrat who long ago learned that creative thinking would be a hindrance to career advancement.

Despite all that, Yellen just may be far superior to Bernanke. It is too late to save the already enormous costs, but Yellen has proved on several occasions to be open-minded in a way her predecessor never was and still refuses to this day.

Bernanke doesn’t make mistakes. His career is littered with them, of course, and big ones, too. But through Bernanke’s eyes as he writes often now at Brookings he had done nothing wrong. The world as it became, he says, did so because of outside factors far beyond his mere mortal control. Bernanke has become the exemplar of Milton Friedman’s ancient observation:

In years of prosperity, monetary policy is said to be a potent instrument, the skillful handling of which deserves credit for the favorable course of events; in years of adversity, monetary policy is said to have little leeway but is largely the consequence of other forces, and it was only the skillful handling of the exceedingly limited powers available that prevented conditions from being worse.

Friedman passed away before the idea of “jobs saved” was given its modern form, but here he was in 1963 describing the Fed in the 1920’s and sounding as if he wrote it as a damning epitaph for Bernanke’s whole Fed tenure in the 21st century. What’s so cutting about it is that it recognizes that there is, in fact, possibly something else. We have been made to believe after Greenspan that the central bank is all-powerful, but it isn’t and never really ever was.

What really happened was far simpler and more consistent with basic human nature. In another Friedman quote, the monetarist explains somewhat his disdain for what was often carried out in his name and why his earlier quote still applies so much for the 2010’s as the 1920’s (and all time in between):

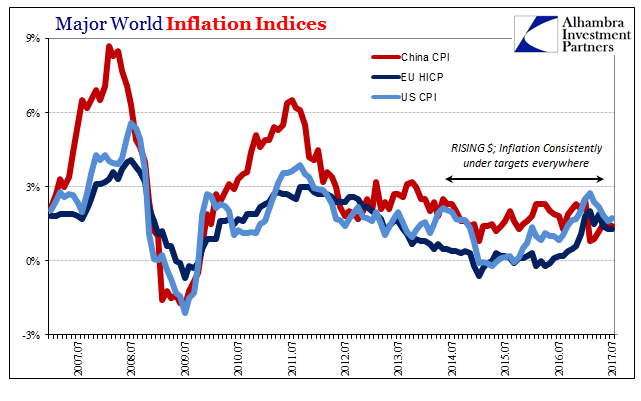

We’re in a period like the 1960s, when no one paid any attention to the money supply. Then we got inflation. By the 1980s everyone was obsessed with the money supply. Now they’re forgetting again. And it will turn around and surprise them.

He made the statement with regard to Japan in the 1990’s, and sure enough here we are with global Japanification creeping into a second lost decade for the world economy. Bernanke who many believe a disciple of Friedman really isn’t; as Fed Chairman he proved Friedman correct instead in how little of money he recognized in its modern forms.

Janet Yellen hasn’t really improved on Bernanke’s performance except to at least consider publicly that maybe the Fed’s performance has been less than ideal. Last year, she admitted in a speech that just maybe Economists don’t really know what they are doing. Yesterday, she added what may be painfully obvious to the rest of the world but still noteworthy for a Federal Reserve Chairman.

My colleagues and I may have misjudged the strength of the labor market, the degree to which longer-run inflation expectations are consistent with our inflation objective, or even the fundamental forces driving inflation.

On the one hand, it is difficult not to yell in frustration given how easy it has been to see why. They tried for years, almost ten years, to dismiss those 15 or 16 million “missing” potential laborers as immaterial to the US economic condition. I won’t get into here the myriad technical (sounding) reasons why they tried, needless to say in common sense terms if an economy sheds that much labor and then refuses to hire it back at any point after there can only be serious, lingering economic problems.

I wrote in November 2014:

It really is that simple, in that without a debt-fueled substitute of requisite “strength” (the student loan bubble and auto loan bubbles, for example, are not nearly of “sufficient” magnitude nor, it appears, intensity to fully replicate the homes-as-ATM’s effect) there is nothing to drive spending above simple earned income. That is a huge problem given that income continues to follow upon a much lower trajectory than anything seen in the post-war era.

Not for lack of trying, mind you. The Fed wanted and welcomed another credit-fueled bubble but couldn’t get one. Despite trillions of asset purchases, including almost two trillion dedicated to MBS, the credit market just would not re-ignite. The US economy was thus left naked without marginal debt supplementation for earned incomes stripped in 2008-09 of such huge capacity and utilization.

Why was that? Why didn’t monetary policy work?

After all, the Fed is largely blamed for the last bubble. Everyone still believes that through nothing more than a 1% federal funds rate there was this housing bubble and mania of epic proportions.

And yet, with seven years of a zero interest rate policy (ZIRP) augmented by four QE’s (believed to be money printing in the public imagination) totaling almost four trillion, nothing; nada. How can this difference be explained?

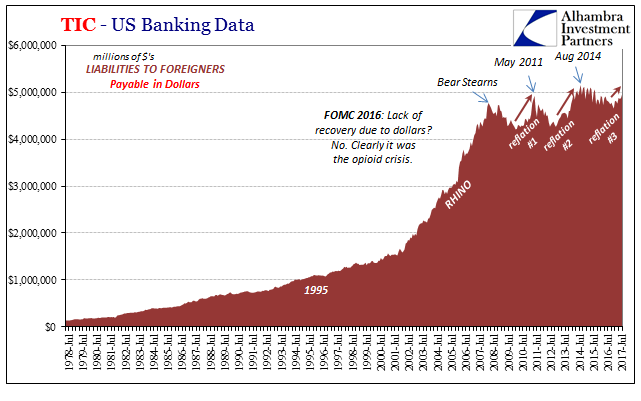

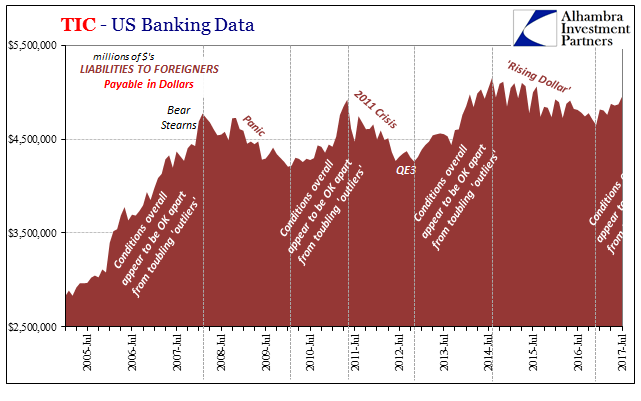

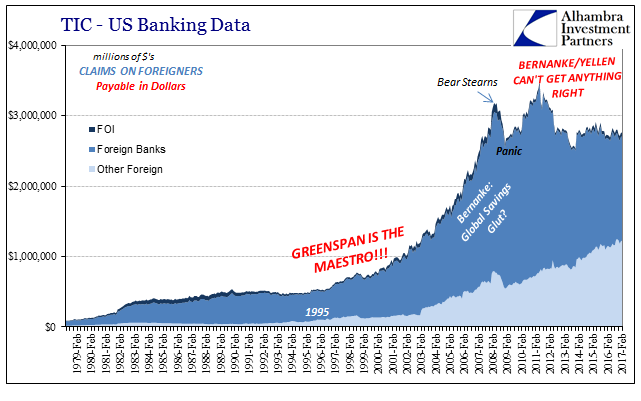

You often hear terms like balance sheet recession or suggestions of changes in consumer behavior to offer something plausible (sounding) to that end. They don’t really fit because the contours of the economic trajectory over the last ten years follow very closely instead “dollar”, “dollar”, and once more “dollar.” In other words, the 2008 panic wasn’t the limit of monetary problems, it proved to be merely the opening act.

What really happened was Japan, as Friedman described of it and Economics at the end of the 20th century. The central monetary agent for dollars had long ago forgotten money and sure enough it did “turn around and surprise them.” The Fed didn’t give us the housing bubble, it merely took credit for it while it was believed to be an economic positive. The something else was always the eurodollar system, both on the way up and now on the way down.

If Bernanke had been nominated and had accepted a third term in 2014, does he admit in 2016 and 2017 what Yellen has been forced to? I highly doubt it. And for that little but substantial difference she is a far better Fed Chairman than he was or probably ever could be. It doesn’t add up to a good one, but the standards here are, given by the conditions of the last decade, very low.

To leave it on a somewhat positive note, the way out of all this mess is clear. Inflation and money are essentially the same thing expressed in different places. If the Fed admits it doesn’t know a thing about inflation, then they are essentially admitting the same thing about money. If they now go looking for the one, they will have to go looking in the other, too. They will be amazed at what they will find, maybe enough given time to make a real difference. If we have that much time.

Stay In Touch