The folks at MacroVoices inform me that due to popular demand (yeah, I didn’t know, either) they are accelerating the scheduled releases. Part 1 played in late August, which you can find here. Part 2 will be available this Thursday. Though still in the early days, Part 2 really starts to get into the transformations and how they work (as well as more about that missing money).

I’ll publish the link when it becomes available.

I don’t have any dates for Parts 3 & 4 yet, but bring your accounting for when they come up.

How Dollar becomes ‘Dollar’

-Bankers’ Acceptances

-The Evolution of Eurodollars

-Where do Eurodollars come from?

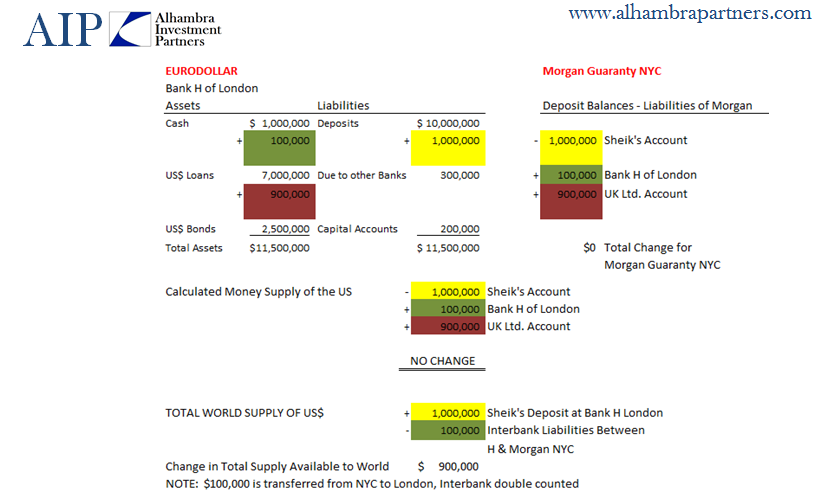

-Money as interbank liabilities

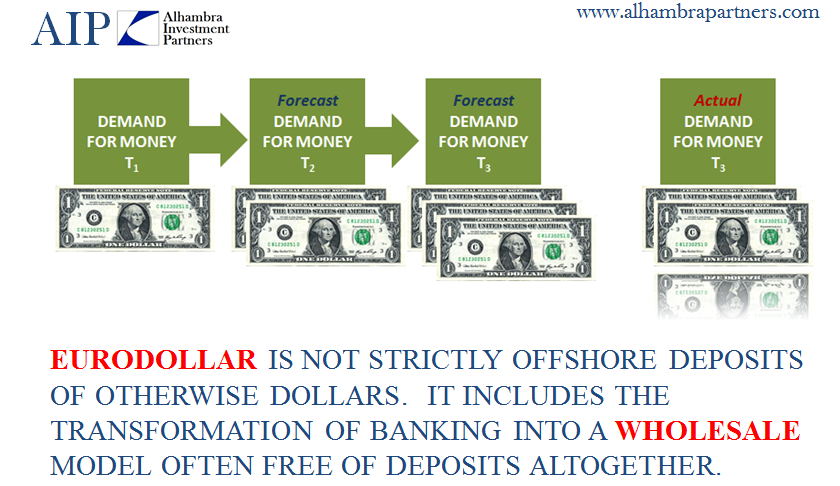

-What exactly are Eurodollars?

-Transformation of banking into a wholesale model

INTRODUCTION: A LOST DECADE

The downside of a “dollar” as a opposed to a dollar is that so much is now unobservable in the form of bank activities that never see the light of day (again, the bank at the center). Since we cannot even define a wholesale “dollar” we cannot think to even attempt its measure as it amounts to chasing a phantom.

A Brief History of Money, Part 1; Part 2; Part 3

We Know How This Ends, Part 1; Part 2

Understanding Eurodollars, Part 1, Part 2, Part 3

There were two major evolutions in money and banking that seem to fall outside the orthodox narrative. The first was a shift of reserves and bank limitations from the liability side to the asset side. The second was the rise of interbank markets, ledger money, as a source of funding rather than required reserve balancing; replacing the old deposit/loan multiplier model.

Far More Important What Is Not There Than What Is

For the most part, the concept of leverage is straightforward and intuitive. In physics, a lever is something that multiplies force to gain mechanical advantage. That is why the word was transported to finance as it means to multiply the effort of a small capital base. The “mechanical” force applied in the form of financial leverage used to be borrowed money or currency, but in the modern wholesale format the multiplication attains not only different forms but also added dimensions.

Of Modern Money And Multipliers

My purpose here is not to get too far down the rabbit hole, but hopefully far enough that you get a sense or at least a taste for this stuff and more so why it all exists to the degree it does. From that, the issue of truly modern money can be revealed. It all starts with accounting.

It’s the antithesis of the pre-crisis eurodollar system, where then these institutions believed no risk was too great because there would only be reward, but today global banking has been turned totally around to all risk with no reward.

If You Believe There Was Too Much Money During The Monetary Panic, Then Why Not Heroin

As I point out all far too frequently still, September – December 2008 was not the first period in which the federal funds rate had fallen below target in serious fashion for an extended length of time. The very first instance was August 10, 2007, which in many ways was a complete precursor of all these systemic discrepancies.

Currency Elasticity Only Applies Where There Is Currency

And that is the relevant point to our conditions right now. The money markets seem to follow policy decision only under benign conditions. Past some unknowable threshold, money markets become money market(S) with the Fed strictly powerless to enforce any kind of order and restorative measures to bring them all back into singular and seamless function. That makes its primary job of lender of last resort fully indefensible and untenable, which explains a great deal as to why we are where we are.

Currency Risk That Isn’t About Exchange Values (added August 28)

Not All Swaps Are Created Equal, Part 1; Part 2 (added August 29)

Rough End of A Collateral Century (added July 28)

You can appreciate the willingness of Chinese monetary authorities to incorporate this odd arrangement; before the 1990’s, China’s economy was a basket case of authoritarianism as well as unevenness. That uncertainty was the dominant view of the currency, as well. Thus, to peg CNY meant to do so credibly, and what better short cut than to “back” CNY by “dollars?”

Stay In Touch