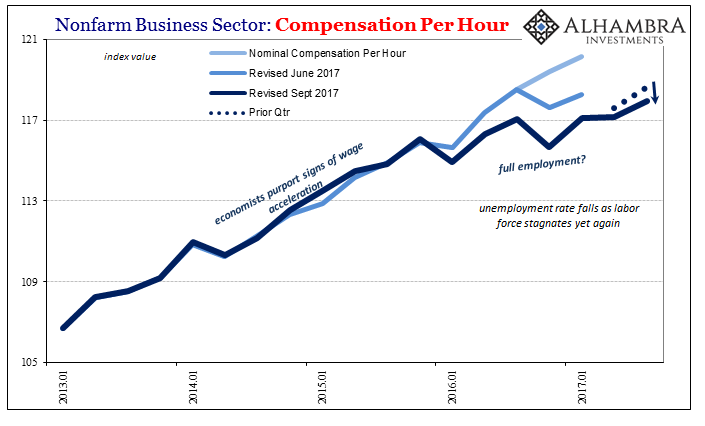

Though the BEA revised GDP slightly higher for Q3 2017, the government agency took hourly compensation out to the woodshed. On a quarterly basis, this metric of labor market wage pressures is often quite volatile. In Q4 last year, for instance, nominal hourly compensation was -4.5% Q/Q (annual rate), followed immediately by a 4.9% gain in Q1 2017.

For Q3 2017, the BEA had originally figured a 5.1% rise Q/Q for the same series. It has now been revised to just 2.7%, a much more serious downward revision than it might otherwise appear. Given the noisiness of the series, and what that likely represents in the real world, these positive quarters are more than necessary to balance out the bad ones in order to equal, over time, sustained growth. Instead, what the revised data shows is that the good periods have become both less frequent and less good.

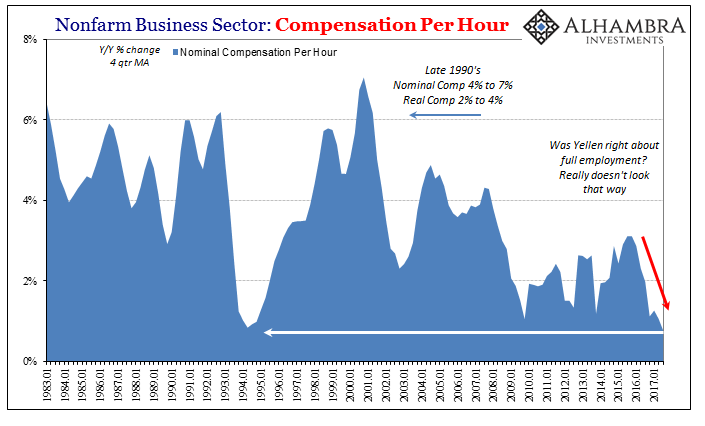

With the latest revisions, nominal hourly compensation, the factor most directly tied to the unemployment rate (the real one, which is not necessarily the version published by the BEA) is growing on average at the lowest pace since 1994. The 4-quarter year-over-year change is less than 1% now, which is worse than at any point in 2008-09.

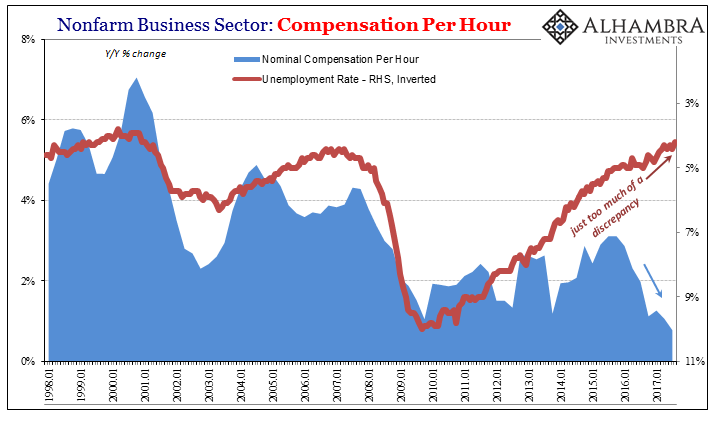

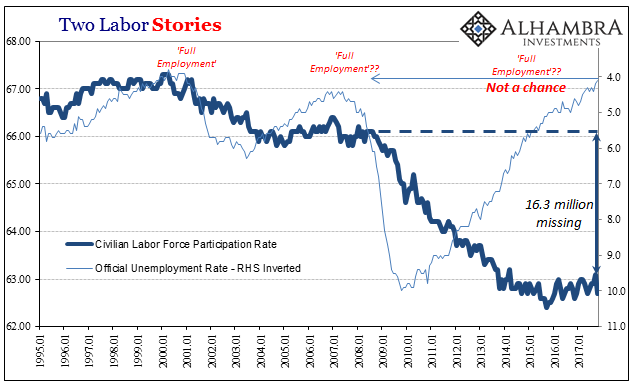

Now that doesn’t mean the economy is falling off a cliff or is about to, only that the labor market is much, much weaker than is otherwise indicated by most of the BLS statistics – including those trying to measure slack. For Economists and policymakers (redundant), this is all taking place at the very same moment the unemployment rate has dipped significantly below all estimates for where full employment “should” be.

This is a contradiction that cannot stand; either the unemployment rate is the correct view, or this wage and compensation data is. It cannot be both any longer.

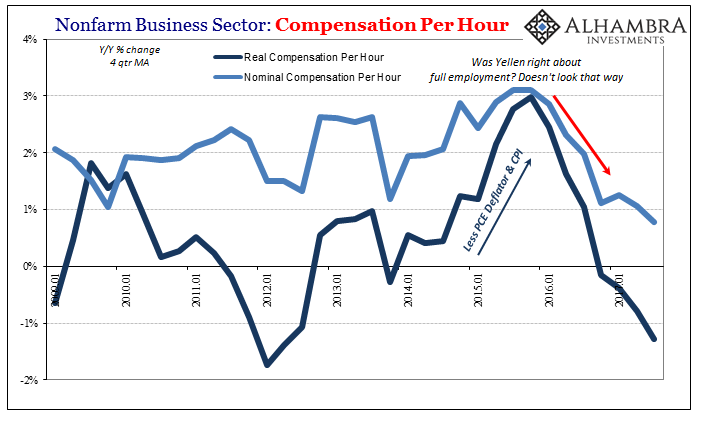

Because of the lack of growth for wages in nominal terms, real hourly compensation has been negative (year-over-year) for four quarters in a row, a full year. That length of time is sufficient to overcome any questions that might arise given the short run noisiness of the data. American workers are much worse off for the 2015-16 downturn.

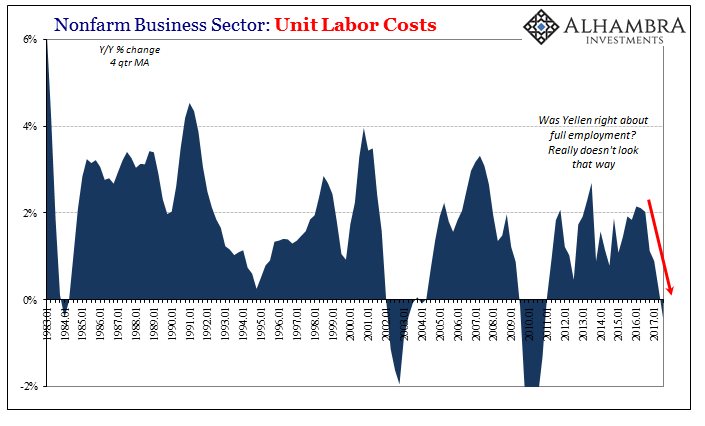

The BEA also estimate that unit labor costs, revised lower for Q2 and Q3, too, have contracted (Y/Y) in three out of those last four quarters. The only positive was barely above zero in Q1 2017. The 4-quarter average here is now negative for the first time since 2010 back when the Fed was introducing its second QE to make sure something like this could never happen.

If the unemployment rate was anywhere close to accurate, we would have seen especially unit labor costs absolutely surge over these same four quarters, if not going further back in time to when it originally hit and fell below 5.5% two years ago. Nominal compensation, the significant part of labor expenses, would have likewise jumped not just to more normal levels but to have exceeded them to a considerable degree.

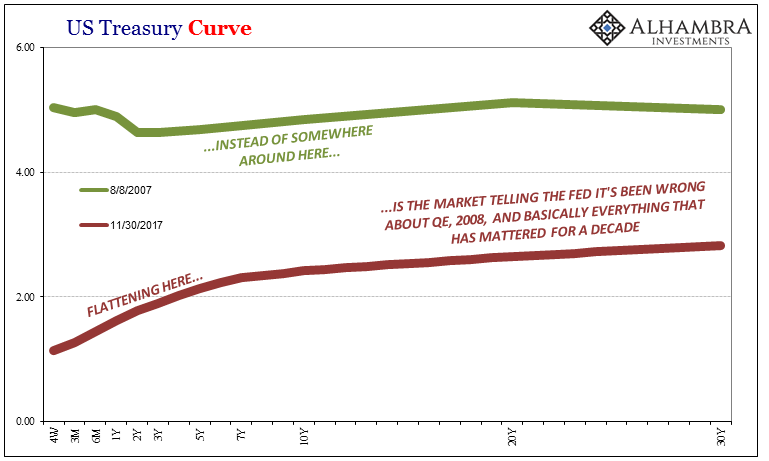

This is in essence the very disagreement between central bankers and the bond market’s long end. The former, no longer in lockstep about all this it needs to be pointed out, continue to project a rise in inflation based entirely on the view of the unemployment rate as the definitive economic statistic. If it really was that way, then they would be correct; interest rates would have to rise, substantially, too, for bond investors to be compensated not just for higher inflation but more so the better economic growth, therefore opportunity, such a trend would represent.

Instead, the yield curve collapses simply because the long end has all the data stacked right against the unemployment rate, all uniformly declaring (no longer a debate) that it can’t possibly be a relevant indication. There is no uptick in inflation now or one expected in the immediate future because the labor market isn’t good now, and more than that hasn’t come close to healing yet from all that occurred ten years ago. There is no wage inflation because the economy shrunk and then remained shrunk.

The unemployment rate at 4.1% does economists no favors. Because it’s so low, it has to right now put up or shut up. There can be no more waiting for wages. It should have already happened long before it ever got this far, but even if you believe in “transitory” factors this is their final curtain call. But we already knew how this was going to turn out; the bond market (and more) told us years ago.

Stay In Touch