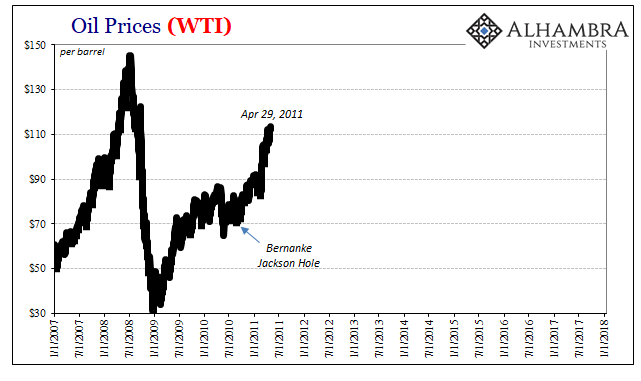

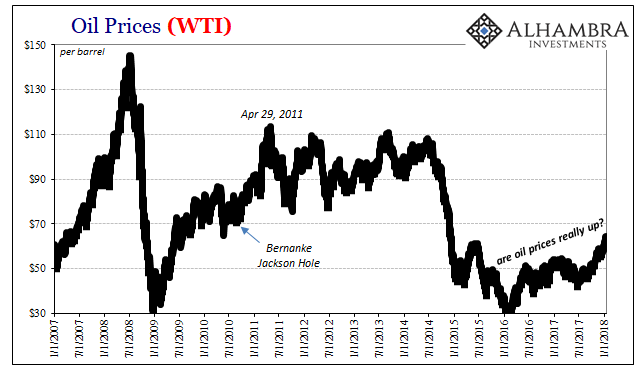

On April 29, 2011, the US benchmark oil price (WTI) surged above $113 per barrel. It wasn’t just American oil prices, either, as other benchmarks around the world were on a huge run. It was the highest for crude oil in three years, going back to the weeks immediately following Lehman. At that price, more so the parabolic trajectory, it seemed a no brainer that full and robust recovery was on the way.

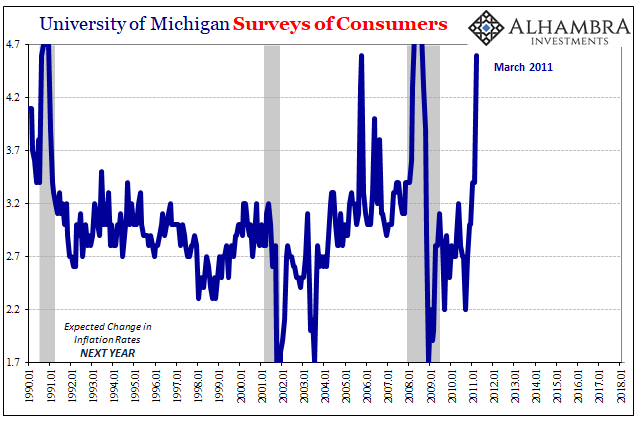

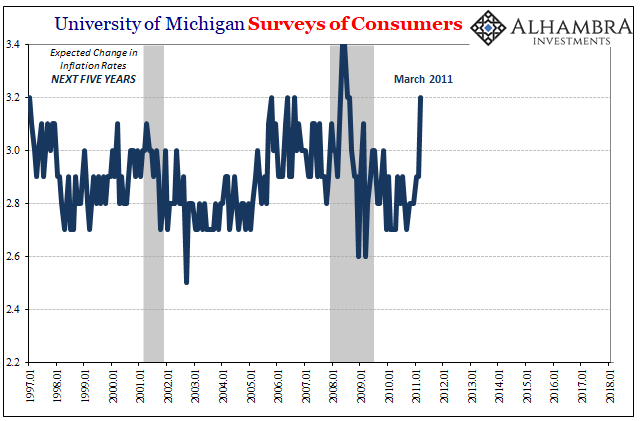

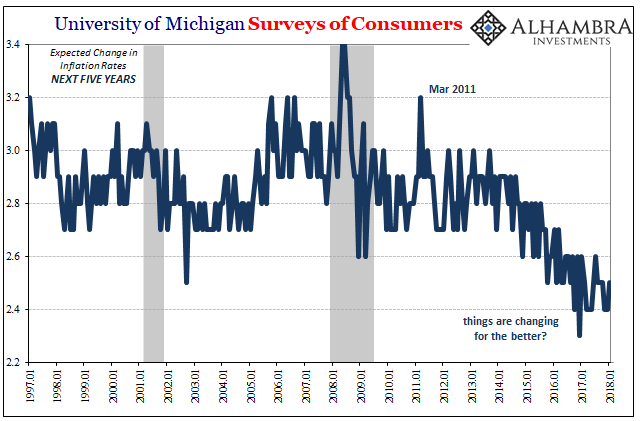

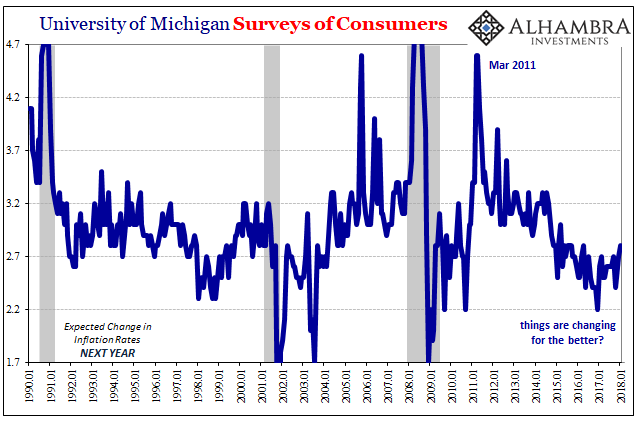

The increase in oil prices were felt far and wide. Consumer surveys, for example, registered spikes in inflation expectations. The University of Michigan’s Surveys of Consumers unsurprisingly registered the same idea as WTI. For the month of March 2011, expectations of inflation one year ahead had surged to 4.6%. Longer-term, inflation expectations five years forward climbed to more than 3%, appearing to suggest some risk inflation expectations might anchor toward the upside.

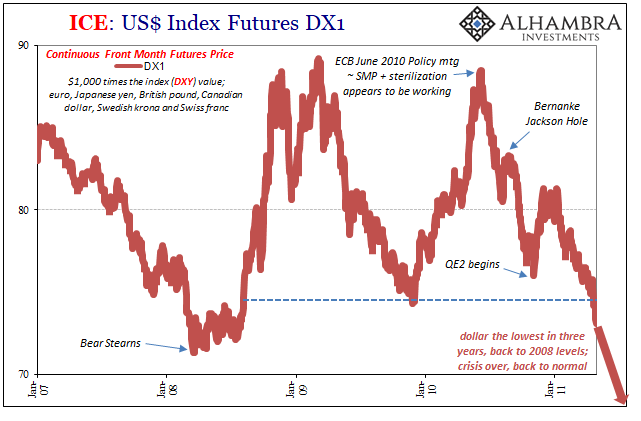

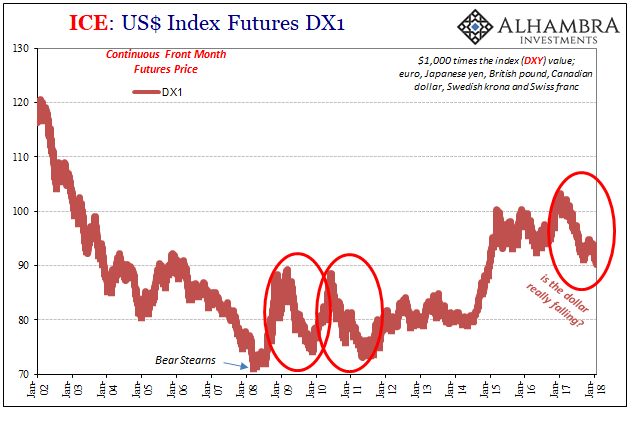

The dollar, as noted earlier today, was at the end of April 2011 falling to a level also not seen since 2008. These multi-year highs/lows seemed in every way to indicate normalcy; and not just the possibility of it but that the probability was so high it was all but guaranteed. There was perhaps more to worry about on the upside than any longer on the downside.

That view, widely shared, however, ignored a whole lot that turned out to be everything. It isn’t surprising that the ECB, for example, “raised rates” on April 7, 2011, and then again on July 7. Central banks were largely responsible for creating the narrative in the first place. The blind spot that had developed was/is a symptom of this very corrupt top-down process.

Given the way things turned out, clearly “something” was missing. On April 28, 2011, the Bureau of Economic Analysis reported advance estimates for US GDP. They weren’t terrible (it would take subsequent benchmark revisions to get them to that level) in the initial runs, but they weren’t good, either. It would become a persisting, and crucial, theme for much of the rest of that year.

It was at that moment in time, essentially, a tug of war between two starkly different viewpoints. The one that prevailed in the mainstream was of the heroic central bank successfully overcoming irrationality and exogenous factors even Walter Bagehot himself would struggle to get past. That was WTI, stocks, and inflation expectations, where in all those there was this perception that not only was monetary policy going to be successful, it might end up being too successful (just like the expectations that drove WTI in the middle of 2008).

On the other side, of course, was the nagging feeling that despite the myths and legends, the constant mainstream accolades, maybe they really didn’t know what they were doing. There was, after all, 2008. As late as early 2011, central bankers were still quite busy doing things that in early 2007 would have seemed totally unlikely. The introduction of a second QE is not a positive indication for the first, nor of QE as a concept.

The difference between those two competing sets of expectations was economic growth. If the first view prevailed, as many markets were expecting, the economy would take off so as to match the rhetoric surrounding it. If it was instead the second view, there could follow only resumed caution and, worse, severe monetary recriminations.

The FOMC in late July 2011 was faced with the latter and only the latter. Though their deliberations were left in private, in truth they didn’t need to be made public. It was a rather simple process even though it cut directly against the recovery narrative – economic failure meant the resumption of funding difficulties, the confirmation that even the best central banks could come up with wasn’t nearly enough (or even minimally effective).

BRIAN SACK, MANAGER, SYSTEM OPEN MARKET ACCOUNT. I would actually like to argue that the declines on Monday [August 1, 2011] were not entirely driven by the downgrade. I think they were a continuation of the decline in sentiment and the concerns about economic growth that we had already seen develop very intensely over the previous week. The downgrade did seem to add to those concerns…And I do think that a lot of the pessimism about the outlook is partly related to this idea that there aren’t many policy tools to address the weakness in the economy. My point would be that the downgrade just added to that, but I think the primary driver of all this is really the revision to the economic outlook. [emphasis added]

On July 29, 2011, the day that the 2011 crisis truly started, the BEA had released revised figures for Q1 2011 GDP along with the advance estimates for Q2. The former had been dropped to just 0.4% growth, while the latter was initially placed at just 1.3%. The weakness in Q1 had got everyone’s attention, though many were willing to wait and see if it would turn out to be nothing more than a noisy quarter. A second straight weak one? Not so much.

What really stung the most was how those particular quarters fell entirely under the auspices of QE2. If it was “stimulus” it wasn’t immediately stimulating. It actually brought up again all the lingering doubts as to whether these policymakers really could do much, or knew much.

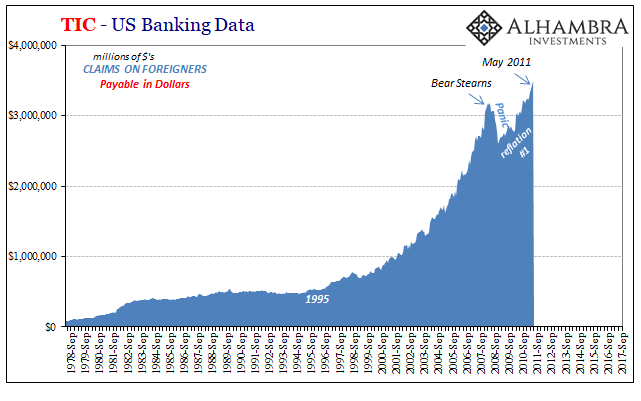

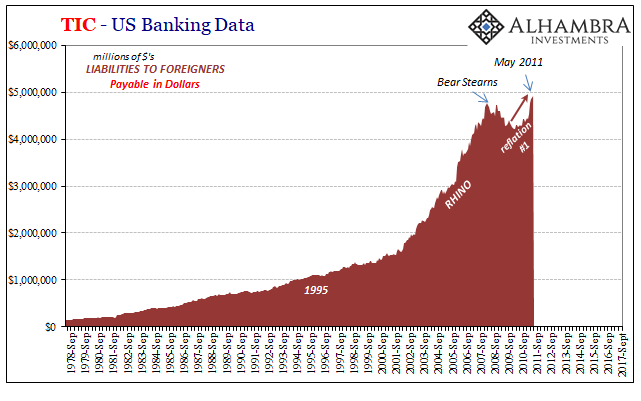

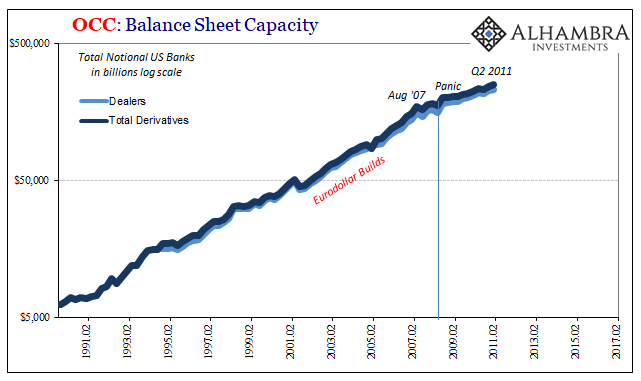

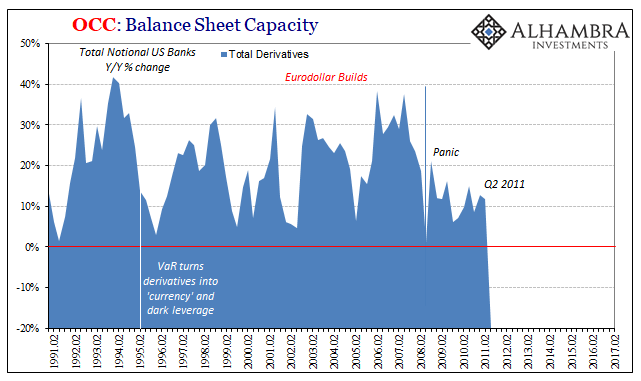

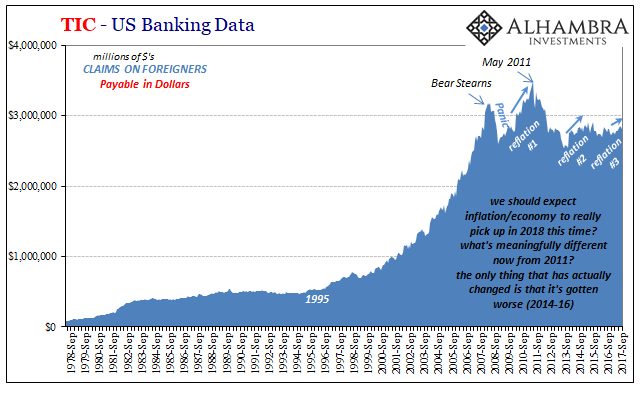

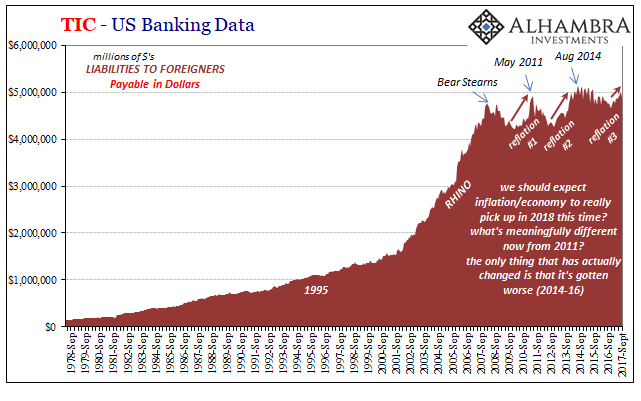

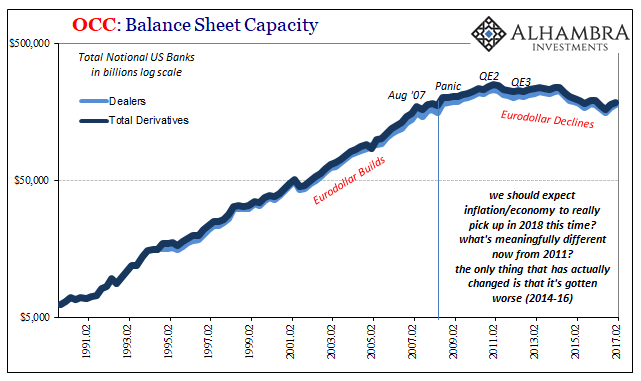

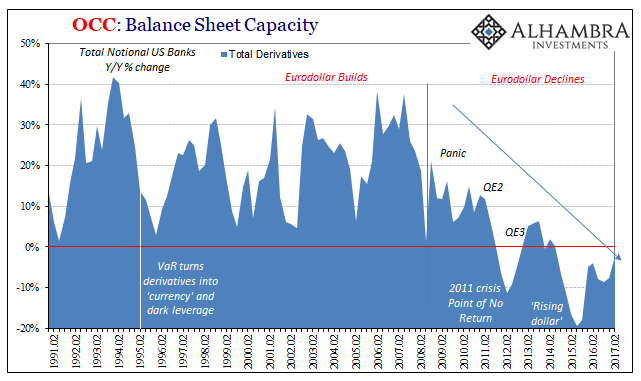

In truth, however, none of this was unexpected, though it was, and still is, constantly written that way. Though oil prices were enthusiastic, making Economists happy and therefore setting inflation as well as economic expectations, monetarily speaking there was considerably less to be thrilled about. Rather than calm doubts about recovery, there was a lot about the eurodollar/wholesale system that didn’t look at all right in the aftermath of 2008.

At that time, the more esoteric eurodollar stuff was looking up, at least, but it wasn’t actually recovering. The exponential trend that had existed up until the middle of 2007 was clearly interrupted, and though monetary growth in these shadow places had resumed it was far less than it had been. It was a hugely important omission, almost entirely ignored in the burgeoning euphoria over heavier monetary policy experimentation. Again, the contrast is simple but striking; the more central banks felt they had to do, there more there was to actually do. Coming on four years after the whole thing started, why were they still so active? It was a question central bankers and economists refused to consider let alone answer.

The economy was missing because the money was missing. Without either, perceptions about monetary policy being this over-potent inflation demon were, to put it mildly, betting on straight bias. Many believed because they wanted to. That’s not rational analysis.

As much as there is similar the past year has shared in comparison to 2014, there is also a lot about 2011 echoed in here, too. Commodity prices are up again, but they aren’t really up. The dollar is falling, but it isn’t really down. Inflation expectations are better, but today they are still extremely low, nowhere even in comparison to 2011. And “dollars” are still just as hard if not harder to come by. And that problem has now spanned the entire globe (Asia and EM’s were largely, but not entirely, left out of 2008 and 2011).

The world learned a lot over the last six and a half years, particularly 2014-16. It’s nice that things appear to be improving, and may actually be in a real sense. That, however, still fails to add up to a meaningful difference, so long as we are stuck with the shadows. Even these market prices that were once all in on the mainstream narrative aren’t nearly so sure anymore. The burden of proof has always resided on those figuring the upside. It’s taken some time for that to sink in, and for quite a few it still hasn’t.

You just can’t talk about growth forever. It’s nice to hear about a boom, but after a while there has to be a boom; a real one.

Stay In Touch