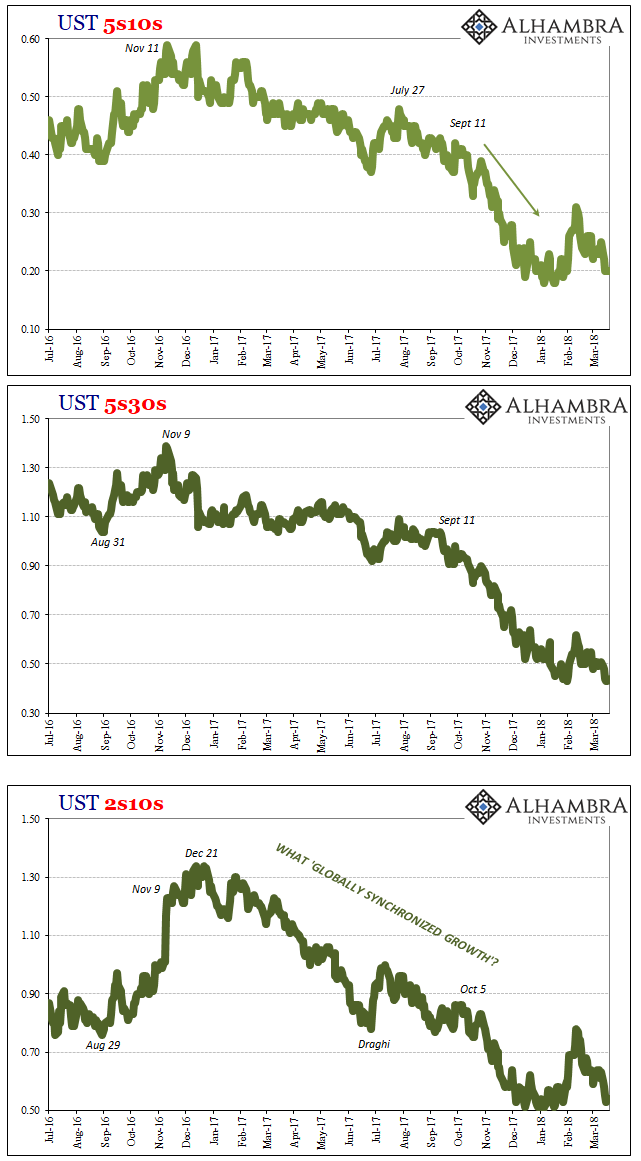

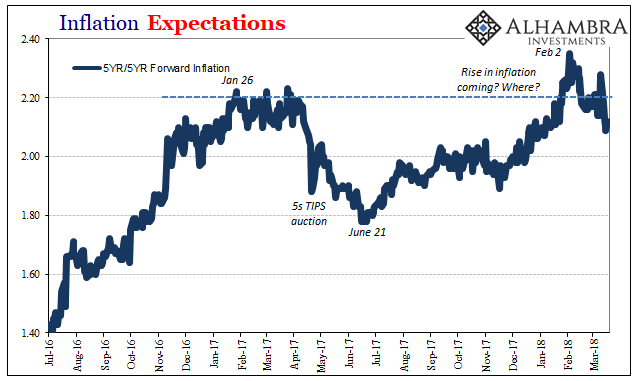

Tomorrow, it is widely expected that the FOMC will vote for another 25 bps “rate hike.” The long end of the UST curve is already just as unenthused as ever, while the short end expects higher yields on money substitutes. The result is the very familiar collapse in the yield curve, one that like both of the prior “rate hike” regimes (1999-00; 2004-06) leads to economic conundrums the monetary policy committee no doubt will continue to debate in total intellectual darkness.

Two decades is, apparently, insufficient to expect progress on the topic.

The funny thing is that it was nearly two decades ago when Paul Krugman of all Economists proposed the very symptoms this and other central banks now face. In 1999, Dr. Krugman was obsessed with the idea of a liquidity trap – a condition whereby no matter how much the money supply may be increased the result in a real economy was “pushing on a string.”

He began his talk with the usual disingenuous compliment:

We live in the Age of the Central Banker – an era in which Greenspan, Duisenberg, and Hayami are household words, in which monetary policy is generally believed to be so effective that it cannot safely be left in the hands of politicians who might use it to their advantage. Through much of the world, quasi-independent central banks are now entrusted with the job of steering economies between the rocks of inflation and the whirlpool of deflation. Their judgement is often questioned, but their power is not.

Krugman then goes on (and on) to question their power. He describes, essentially, the case where they are, surprise, powerless. This liquidity trap situation manifests in several key indications.

If, for whatever reason, the natural real rate of interest is negative, then the economy “wants” inflation. You may well ask why and how it should happen that the natural real rate is negative; but just for the moment suppose that it is. Then the economy will find itself in a liquidity trap as long as the private sector does not expect sufficiently rapid inflation.

No matter what the Fed, BoJ, or any of the others might do in this situation, it won’t provoke the inflationary response. Why? Dr. Krugman proposes the time horizon, or time constraint.

Monetary expansion is irrelevant because the private sector does not expect it to be sustained, because they believe that given a chance the central bank will revert to type and stabilize prices. And in order to make monetary policy effective, at least in a simple model, the central bank must overcome a credibility problem that is the inverse of our usual one. In a liquidity trap monetary policy does not work because the markets expect the bank to revert as soon as possible to the normal practice of stabilizing prices; to make it effective, the central bank must credibly promise to be irresponsible, to maintain its expansion after the recession is past.

You should immediately recognize the outlines for monetary policy over the last decade in that above passage. This is what used to be called “forward guidance”; the realization that markets are rational and therefore will respond to inputs not just immediately but how they are expected to affect the longer term.

To overcome this problem, any central bank facing a liquidity trap should go big, leaving no doubt about this intention; “credibly promise to be irresponsible.”

This was done several times over during the last ten years, and in several very different locations. The US central bank scaled up QE’s until reaching QE3 (then 4) promising initially for it to be open ended; Japan’s expanded their lengthy list of prior QE’s to include QQE in 2013; and the ECB after driving its money corridor floor to NIRP then finally relented on quantitative easing that remains ongoing three full years later. Central banks have spent the last ten years trying their best to be irresponsible.

Each of these programs were applauded and received enthusiastically as filling the role Dr. Krugman proposed. The initial rounds of QE in the US, for example, provoked sharp criticism largely predicated on fears that it was too much – just as was intended – and would lead not just to inflation but the runaway variety. Those condemnations have entirely disappeared.

What all that means is that the US and global economy continues to behave according to the symptoms set out in Krugman’s 1999 liquidity trap thesis; from the perceived negative natural real rate of interest to the lack of inflation and follow-through from it. His proposed solution to the central bank “power” issue has likewise been met; though, to be clear, his later writings particularly in 2015 and 2016 declare otherwise. It is, as he wrote then, never enough for central banks.

This is has left them with what amounts to magic number theory to explain how meeting all the liquidity trap conditions whichever economy remains anyway in what appears to be the same liquidity trap.

In other words, this is no time to be timid because everything that he [Krugman] and others like him promised didn’t work, which to them means that it didn’t work because it wasn’t big enough even though when they planned what didn’t work they said then that it was bigger and better than the time before that. There is apparently no economic ill that the “right” amount of policy can’t fix, even if that ill is policy. Unfortunately for the world, economists obviously aren’t permitted to know what the “right” amount of policy is until they actually see whether what they did do was it (I am not making this up). Why not just dispense with the façade of science and discipline and just throw darts? It’s as likely as what they are doing now to come up with the magic number answer.

In other words, they were credibly irresponsible in 2009; then 2011 happened. They were even more credibly irresponsible in 2012-13, then 2014 happened. By 2015, magic number theory was everywhere. They are always described in the future tense as if they will be the biggest and baddest ever conceived, only to be remembered in the past tense as they weren’t big enough.

The more scientific conclusion might instead be one which recognizes how all the 1999 conditions have been met – and the result is still the same, even as far as 2018 now. Thus, is it not possible that central banks are powerless no matter the number?

That’s the part people have a very hard time with. After all, Krugman stated in 1999 what everyone believed. The question is whether they still believe it; or enough do.

In other words, let’s flip his thesis on its ear. His idea was that under these circumstances a central bank must display its power; no more moral suasion or self-fulfilling prophesies. What if it does deploy all its capabilities, and nothing happens as it was supposed to? The central bank credibly promises irresponsibility and in the process proves its irrelevance, a point driven home by numerous iterations across very different local economic conditions/systems.

That situation would lead us back to the symptoms of Krugman’s liquidity trap; “In a liquidity trap monetary policy does not work because the markets expect the bank to revert as soon as possible to the normal practice of stabilizing prices.” Or, in this situation, monetary policy does not work because markets have been shown exactly how monetary policy does not work.

We are left with the inescapable conclusion that central banks are, indeed, powerless. Why?

Also from 1999:

CHAIRMAN GREENSPAN. I must say that I have not changed my view that inflation is fundamentally a monetary phenomenon. But I am becoming far more skeptical that we can define a proxy that actually captures what money is, either in terms of transaction balances or those elements in the economic decisionmaking process which represent money. We are struggling here. I think we have to be careful not to assume by definition that M1, M2, or M3 or anything is money. They are all proxies for the underlying conceptual variable that we all employ in our generic evaluation of the impact of money on the economy. Now, what this suggests to me is that money is hiding itself very well.

The results of this intellectual as well as operational deficiency are what look like a liquidity trap. The Fed is constantly pushing on a string, except it isn’t pushing at all; policymakers have been fooled by their own monetary blindness into thinking they have been. The market, aware of the difference after repeated attempts, begins to ignore or at least factor monetary policy as it really is – as is only rational (score one for irony).

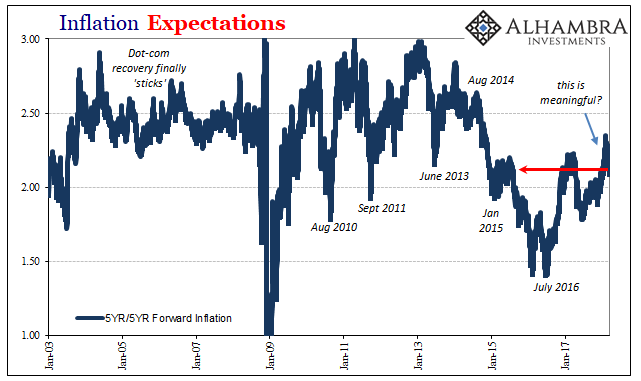

Nobody in an official capacity could figure it out because officially it’s still 1999 where “their judgment is questioned but their power is not.” That was, in essence, the “rising dollar” of 2014-16. The bond market began (in 2010 and 2011) to question the whole idea of monetary power and concluded they don’t have it.

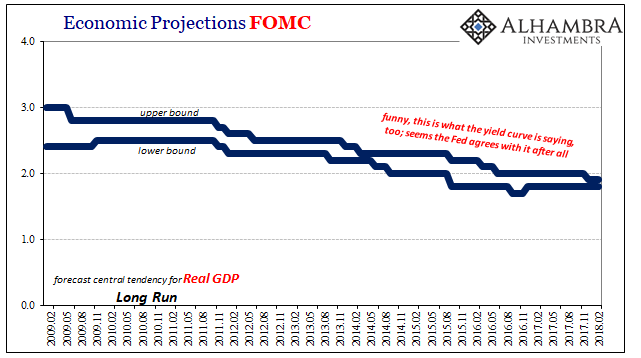

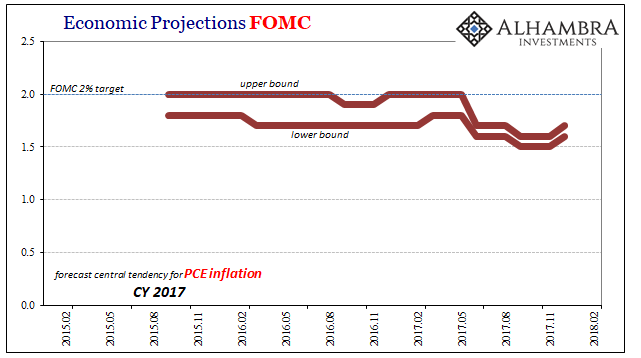

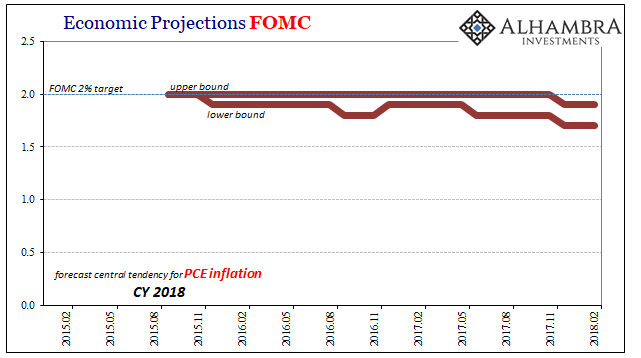

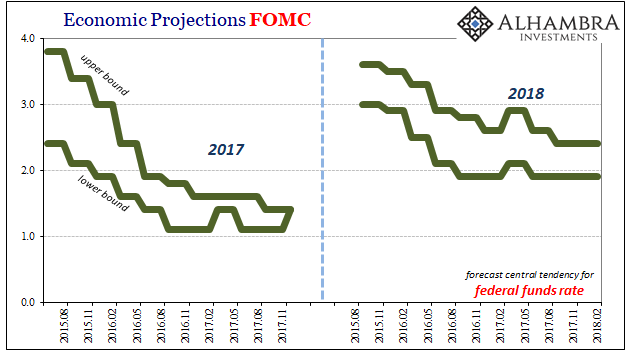

The Fed will raise its policy rates tomorrow for the sole reason that it’s been ten years and what else can they do? You may think they expect this globally synchronized boom that’s been going around often hysterically, but they really don’t. Their projections are, to put it mildly, for nothing other than the same string.

They’ve stopped pushing on it, and you really can’t tell the difference.

Stay In Touch