Like so many financial prices, copper’s is tied to both money and economic fundamentals. They call it Dr. Copper for a reason, good as it has been in suggesting ahead of time the direction for the global economy. China is as central for the setting there as well as in “dollars.”

During the early days of the “rising dollar” I wrote that copper was one clear indication being pulled downward by both. China’s economy was slowing, especially the export side, not accelerating as had been anticipated. The narrative during Reflation #2 was the same as it has been throughout Reflation #3 more recently; global growth would rescue any laggards. They only added “synchronized” to the latest one to really emphasize just how much they mean it this time.

From April 2014:

The ongoing disaster in trade demonstrates the miscarriage of that strategy (on both ends), namely not anticipating orthodox failure across every jurisdiction to deliver promised resurrection. There has been no American surge to reignite the export “miracle”, while Europe tries to convince itself and the world that not shrinking counts as a recovery. Now the Chinese are in a nearly impossible and precarious position.

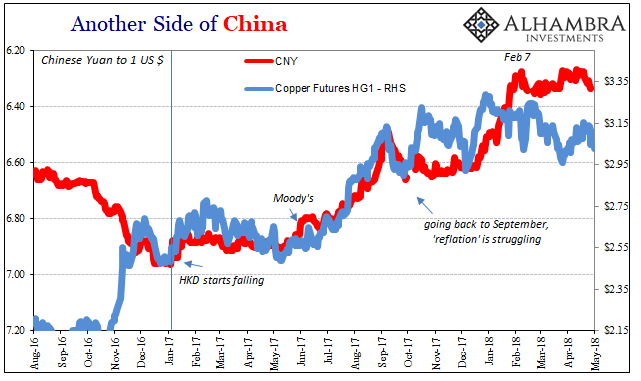

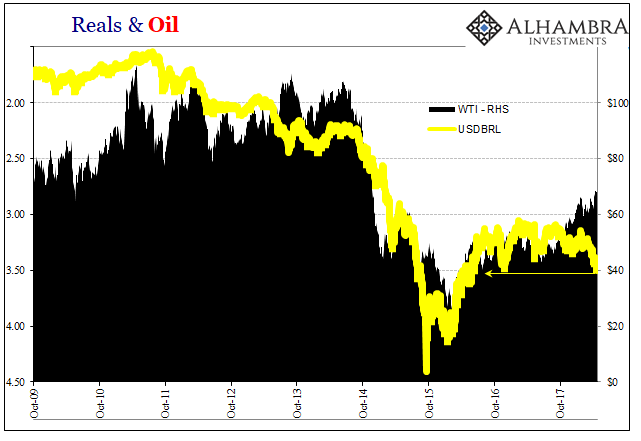

I have argued before that behavior in the yuan, the recent “devaluation”, was not initiated at the behest of the PBOC to punish “speculators.” Rather, it seems far more likely that it was a dollar problem, one tracing through both global trade and finance.

That all continued, economy and eurodollars, all the way into early 2016. The downturn was serious enough here in the US, but it was decisive in China.

It might not have seemed that way early on in the turn (I know I didn’t see it that way). As “reflation” was reborn in the middle of 2016, it also took on both proportions dollar and economy. The monetary component of “reflation” was pretty straightforward – less funding pressure meant the “dollar short” in China and elsewhere was less impacted by a somewhat alleviated “dollar shortage.”

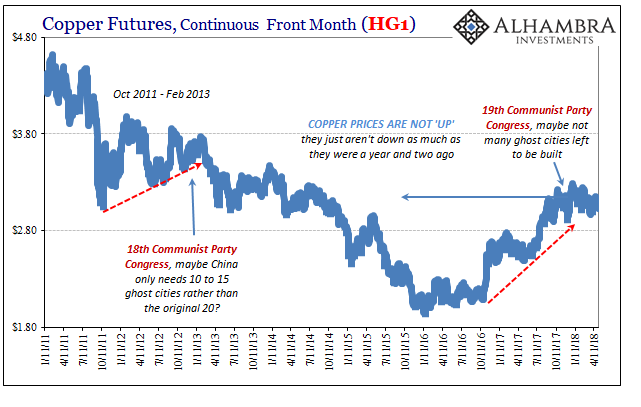

As esoteric as all that is, it’s been the economic piece of copper that has been less more misunderstood in my view. Copper is China FAI, and China FAI is all about ghost cities.

I wrote last year:

Thus, copper’s peak in early 2011 coincides with perceptions (including those relating to global money) about how many new “ghost cities” China might still have yet to build. If the global recovery after the Great “Recession” was to be delayed, the Chinese might not need in the foreseeable future much more by way of new construction. The price of copper is therefore in large part a proxy for China’s view of that paradigm (especially given copper’s role in construction finance as collateral).

It was widely believed, and publicized, before the Great “Recession” that there might be as many as 25 additional ghost cities (that don’t stay empty for very long). The economic and monetary disruption in 2008 caused some to worry about delays, but as EM economies like China’s appeared to be insulated from any fallout copper sprung back to life from its brief 2008 crash. It registered an all-time high in July 2011.

Then the second crisis happened. Dr. Copper (as other commodities) could tell that this renewed eurodollar issue wasn’t just European, and had as little to do with PIIGS as the prior one had to do with subprime. It would be economic and global, too.

By the time of the 18th Communist Party Congress in 2012, there was still some optimism about a worldwide comeback, or at the very least an effective Chinese response (as was talked about during the handover to Xi Jingping). What happened by April 2014 was both the monetary and economic sense it wasn’t coming.

Copper’s reflation in later 2016, then, more and more appears to have been something similar. Eurodollar issues faded, and globally synchronized growth was born and became widely accepted. Until last September.

We are in many ways back to April 2014 again. “Dollar” issues have really resurfaced and have been stubborn about it, especially as they may relate to China’s participation in the eurodollar system. Then there was the 19th Communist Party Congress that, for the unbiased, dispelled any official notion of future acceleration. In many ways, the Communists were careful in announcing a worldwide “L” – and then have so far lived up to it.

It’s not just copper that has struggled, of course. Gold has, too. In many ways, there are similarities in each’s coverage of the intersection between money and economy. Copper may be exposed more to China’s ghost cities, but gold captures some great deal of inflation expectations. Both are definitely tied to eurodollars.

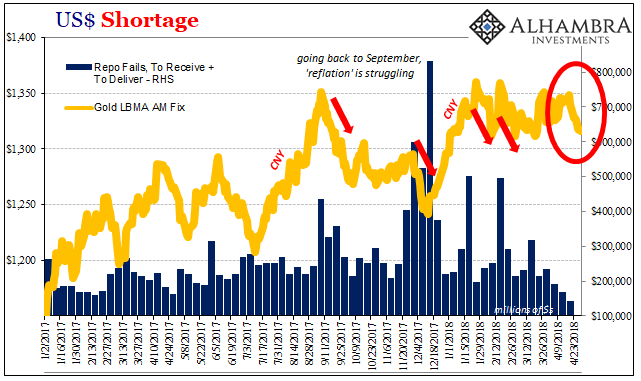

And both metals have struggled going back to early September. In hindsight, and some foresight, it may have been a warning for what was to come – and may yet still. I wrote at the start of last October:

To go back a few weeks when the first big jump in fails was published, the significance of it was potentially as an escalating warning about systemic liquidity, collateral and otherwise. After all, if something unknown is clogging, removing, or just plain disrupting collateral flow it’s not likely to be an isolated case; and certainly not for three weeks running.

Three weeks (and perhaps longer) simply confirms that this is some kind of warning.

That’s a big enough period of time to traverse, more than sufficient sample size, to now more reasonably determine a sizable shift in money and economy. It’s a growing sense of yet another case of globally synchronized disappointment.

Stay In Touch