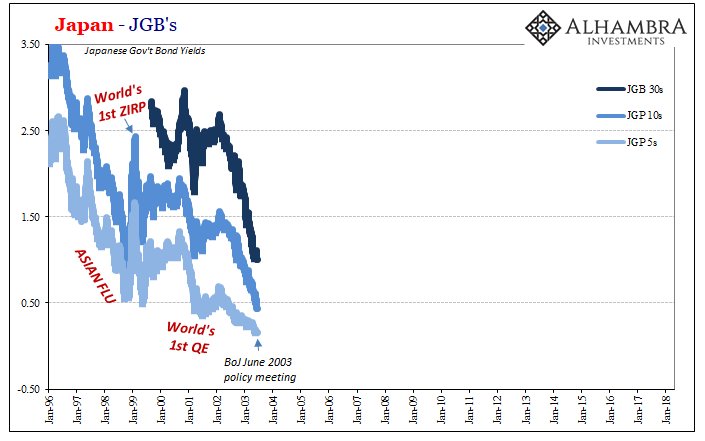

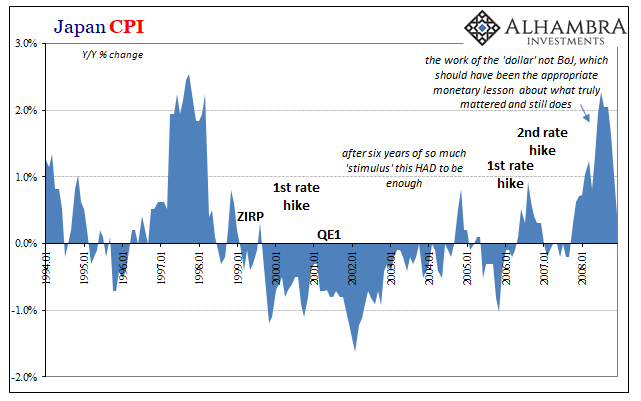

File it under the things they wish you would never find out. On March 25, 2003, two years into what was supposed to be a temporary intervention, the Bank of Japan gathered for another policy meeting to discuss what they might do. They had launched the world’s first ZIRP in February 1999, ended it August 2000 with a “rate hike”, and then on March 19, 2001, embarrassingly reversed course. This time it would be the world’s first QE.

By March 2003, it was clear it wasn’t working. Japanese central bankers discussed ways in which they might go further. BoJ’s Deputy Governor at the time, Kazumasa Iwata, wanted the Bank to introduce an explicit inflation target. It would commit the central bank to unlimited “easing” for as long as it took, satisfying the criticism from some mainstream Economists.

He was opposed by Governor Toshihiko Fukui who had just ascended to the top post.

While Fukui was “sympathetic” to the idea, he said, “I have a basic doubt that we cannot control expectations.” Rough translation aside, Fukui would know best about monetary policy not working as designed from being measured in academic models.

But the Japanese had already gone with something else. Beginning January 2003, the Bank of Japan started intervening more heavily in foreign exchange; only it wasn’t really the BoJ or at least its policy behind the transactions. The Bank was acting at the behest of the Ministry of Finance (MoF), as it was required to do. The latter decided on yen policy using the former to carry it out.

When BoJ officials reconvened in June 2003, on the 10th and 11th of that month, the minutes record two important developments.

In the foreign exchange market, the yen depreciated as market participants became sensitive to a possible market intervention and as some U.S. economic indicators improved. The yen is currently traded in the range of 117-119 yen to the U.S. dollar.

MoF had not acknowledged its entry into yen manipulation, but the markets by June had already suspected that’s what was going on. By that time, they didn’t really need official confirmation because it was pretty clear they were in there to a considerable degree and in a sustained fashion.

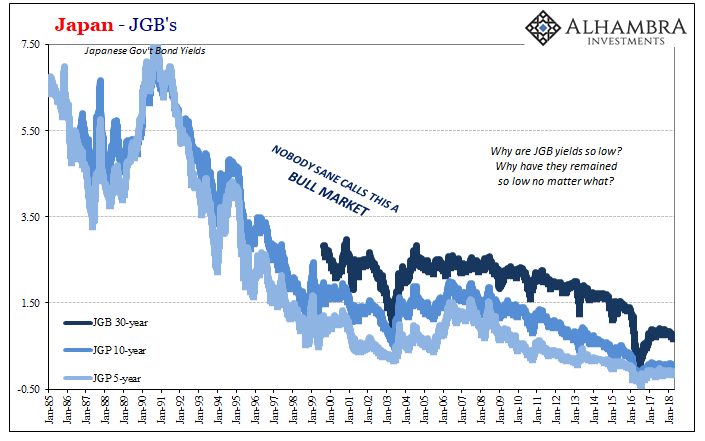

Before that particular policy meeting, Japanese government bond (JGB) yields had been falling precipitously. It wasn’t a straight line, of course, as nothing ever goes that way, but despite ZIRP, QE, and then double QE, the JGB yields kept up their bearish outlook.

Whether it was MoF’s more forceful commitment to weakening the yen (which ultimately failed) or whether it was the improving economic outlook in the US (and therefore, by extension, globally synchronized growth), for whatever reason the JGB market reversed at that moment. Likely a combination of perceptions of monetary policy, combined with yen policy, alongside the improving economic picture, what followed was perhaps the first BOND ROUT!!!

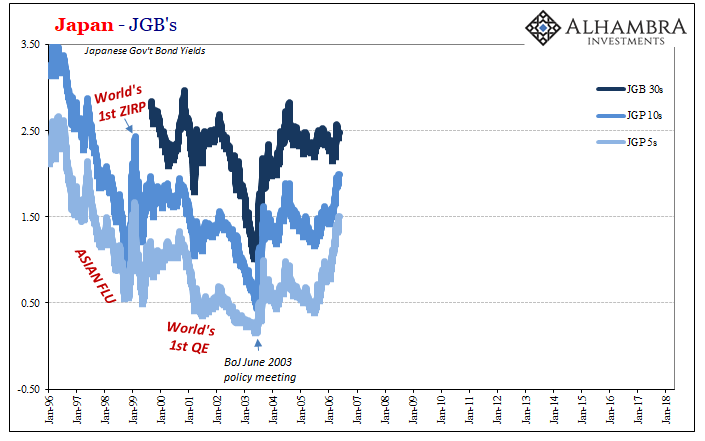

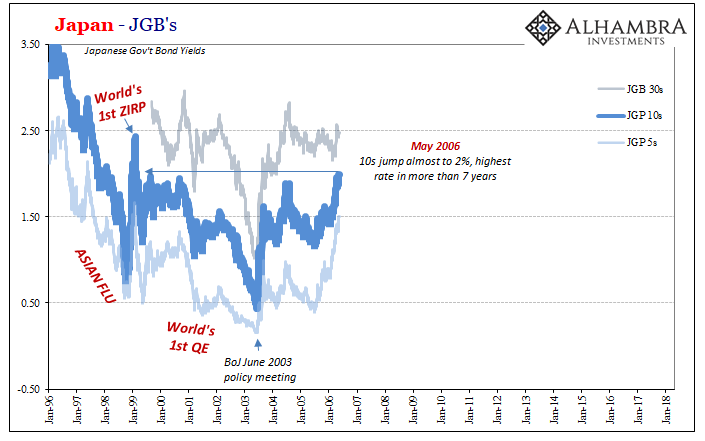

It didn’t go in a straight line, either, but by spring of 2006, three years later, the JGB 10s was poised to strike above a major round number. It had come close on a couple of occasions, and on May 15, 2006, the 10s closed at a calculated rate of 1.996%. It was the highest yield in 7 years to that time, and everyone knows that once that happens and you come close enough to break above a psychological barrier like 2%, or, say, 3%, that means the bull market is over. Dead. No going back.

Except that was it. It never did get above 2%, and frankly it wouldn’t have mattered if it did. There were already problems with the narrative long before May 2006. The JGB 30’s, for instance, had peaked back in 2004 and like the UST 10s throughout the middle 2000’s acted the same conundrum.

Japan’s economic recovery at that time was no economic recovery at all. The BOND ROUT!!! was based on perceptions that BoJ officials had finally gone far enough (with an yen assist from MoF), and more than that knew how to get the economy going once they explored policy limits (if only the BoJ discussions had been made public sooner). This should all sound entirely too familiar.

It’s been all downhill again ever since. The BoJ even went so far in 2006 as to hike rates, and the again in early 2007, but like 2000 it was all predicated on bias and subjective interpretations particularly about inflation. I wrote in October 2016:

Just like 2000, however, there was still a great deal of uncertainty about “deflationary pressures” in Japan. In 2004, the CPI had turned positive, seemingly confirming the solidness of the recovery; reaching as high as +0.8% in November 2004. But that was all short-lived, as just three months later in February 2005 the CPI was negative once more. By November of that year, it was down as far as -1.1% all over again as if QE hadn’t changed anything since 1999.

In the grand scheme of things, that BOND ROUT!!! in the middle 2000’s wasn’t even all that much to have gotten excited about. It could have, I suppose, represented the start of something like normalization. But it wasn’t really as much of a rout as it was made out to be. The proportions of it were really quite small in context.

You do notice that diminutive “V” pointed at the middle of 2003, center chart, but overall it doesn’t represent anything substantial. It was more minor shift from an extreme bearish position up to 2003 that Japanese officials didn’t know what they were doing and that there would be considerable negative consequences because of that.

Starting June 2003, aided in no small part by the Federal Reserve’s decision to lower the federal funds target rate to 1% a few weeks after the BoJ meeting, these markets shifted only slightly their perceptions about the long run. Maybe there was some small chance global central bankers might figure it out. Or even just random good luck the economy would grow.

They didn’t. It didn’t.

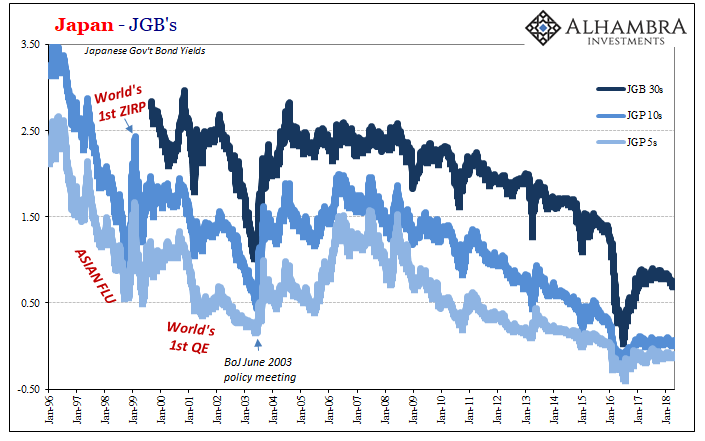

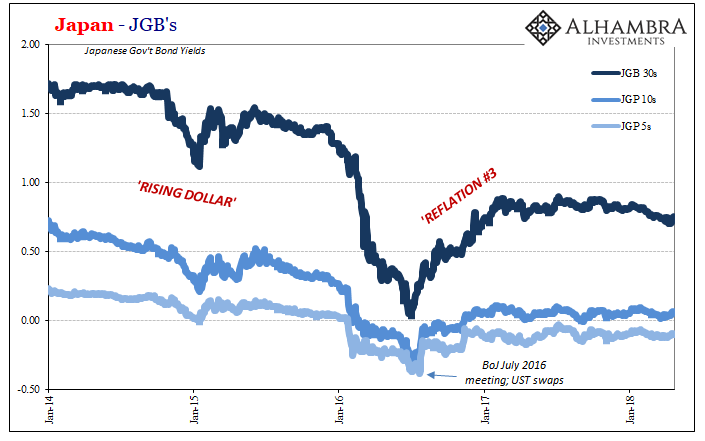

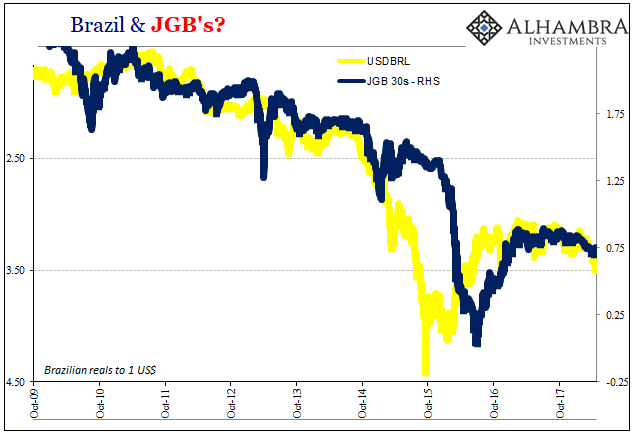

Thus, if there is one market in the world that knows about BOND ROUTS!!! and numerous such false starts on recovery, it is JGB’s. That’s not good news for Reflation #3 globally, and this renewed globally synchronized growth narrative. At least when it appeared in the middle 2000’s, there was a massive and expanding credit bubble (based on eurodollar mania) to create a plausible interpretation. In the 2010’s? All there is is narrative.

In all-too-similar circumstances, the JGB 30s peaked awhile ago. Positivity based on whatever in July 2016, again probably a combination of hope that central banks would finally get it right alongside some economic improvement and expectations for more, didn’t really last very long nor did it get very far. It’s a repeated minor “V” that’s actually closer to an “L.” Not good.

Further, around September and October last year, it appears to be rolling over. And the pattern is one we recognize in a lot of things that really shouldn’t (by orthodox conventions) be so closely correlated.

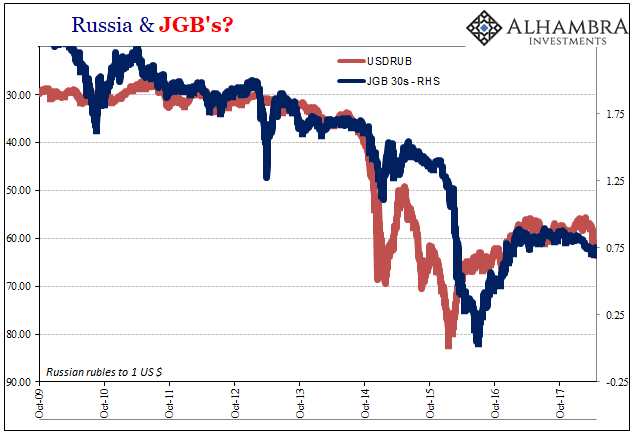

It’s easy to dismiss JGB’s history as nothing more than Japan’s accumulating problems that have only to do with Japan. Even if that was true, meaning that the Japanese economy was an island of isolation, there would still be the startling unease caused by just how closely US monetary officials have styled themselves after BoJ actions (after criticizing them so heavily in, get this, June 2003). We are them, only about a decade or so behind.

That’s ultimately what the JGB market has been saying all along. It didn’t matter what the BoJ had done, nor did it matter for more than a few years that the economic outlook might have appeared brighter, in the end nothing actually changed. The economy remained mired in a massive depression, a slump without end. JGB’s were signaling that there is an economic case where recovery isn’t guaranteed no matter how much time might pass – a circumstance far beyond the business cycle.

Call that a bull market if you want, but no sane person would. It’s a global paradigm the entire planet would cheer for its end. For that to happen, though, something meaningful has to change. Not tax cuts, not the next genius central bank idea, and surely not Jerome Powell’s sunny disposition and outlook for inflation. They are always sunny, and they always see inflation. Occasionally the bond market gets pulled in, too. It never lasts.

Stay In Touch