Observing the eurodollar system as I’ve done for so many years, you have to be prepared for curve balls thrown at you. Just when you think you’ve got it clocked (sometimes literally), something changes and it all gets tossed out the window.

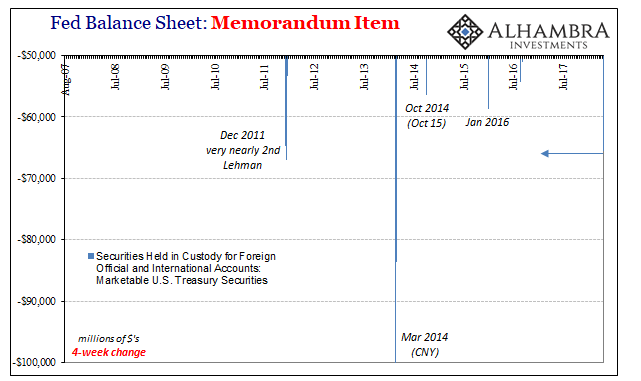

About a month ago, the Federal Reserve reported a sharp drop of UST’s in custody on behalf of foreign agents. I noted then, and remain convinced now, that was something like a collateral call. It happened the week of April 18.

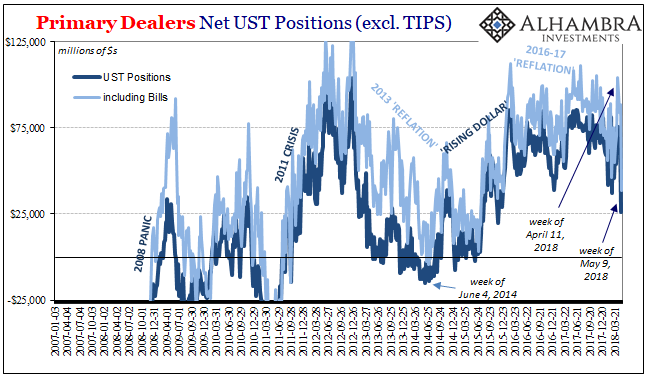

Not surprisingly, the same data shows over subsequent weeks the amount of UST’s in custody continued to decline sharply. The four-week total (through the week of May 9, the latest available) is about -$66 billion. That’s an enormous drop, a level in the same class as other episodes where global liquidity problems were obvious.

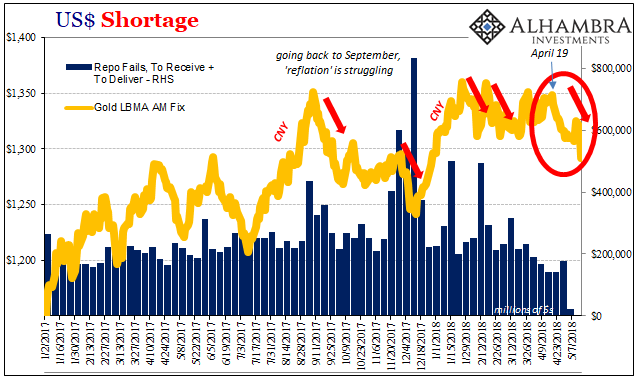

Not only that, gold prices have been exhibiting the same repo-related tendency (crashes) dating back to that same week. Yesterday, gold fell below $1,300 for the first time since the last trading day of last year. It’s the same anti-reflation/collateral deflation pattern we’ve become accustomed to.

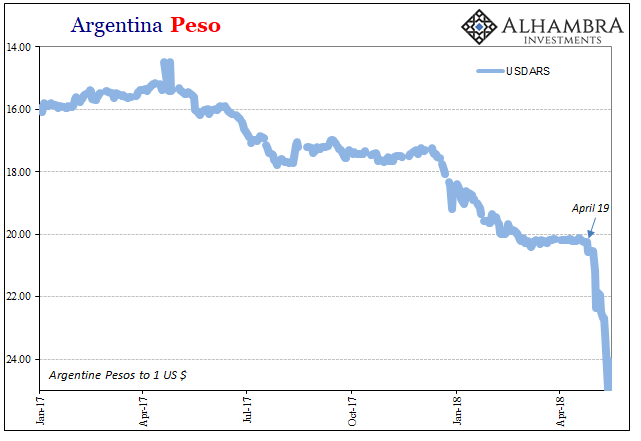

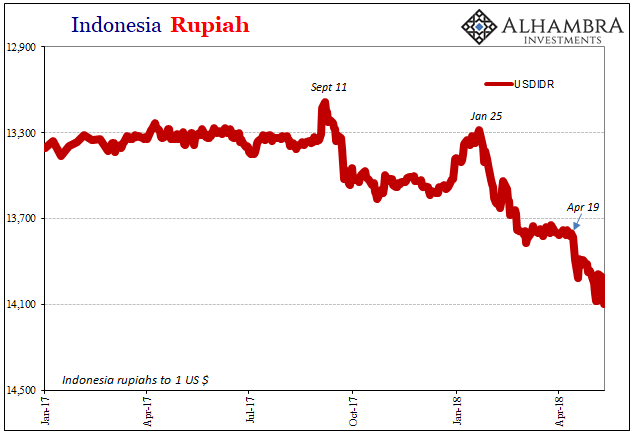

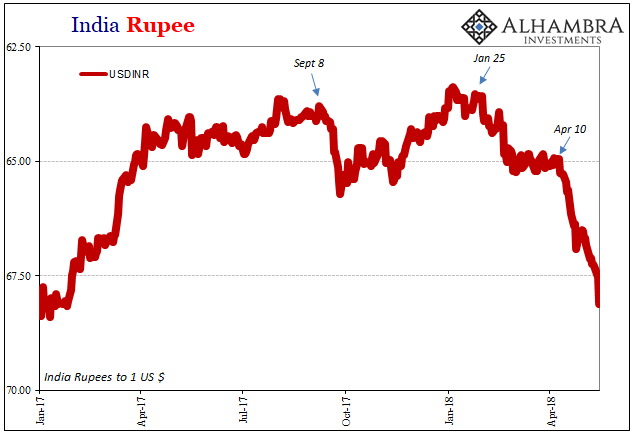

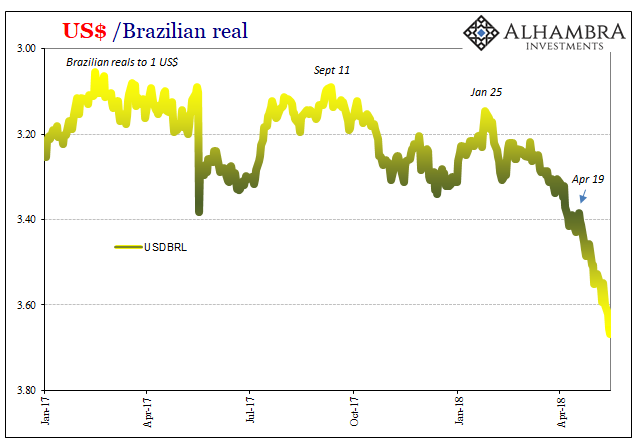

As if we needed more evidence, this latest currency crisis (and it is now a crisis) spreading across the world traces its origins to the same week. The Argentine peso, for one, had been merely falling prior. Since the week of April 18, it has crashed. The same goes for others like the rupiah and real.

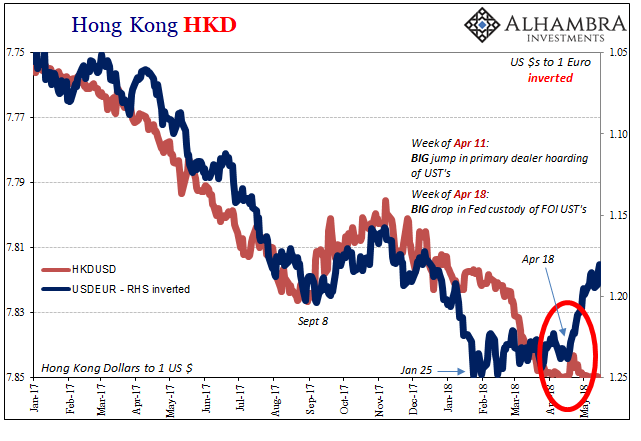

It’s also the week when EUR turned and HKD exhibited the heaviest HKMA interventions. We know without a doubt that something turned really bad the week of April 18, but what was it?

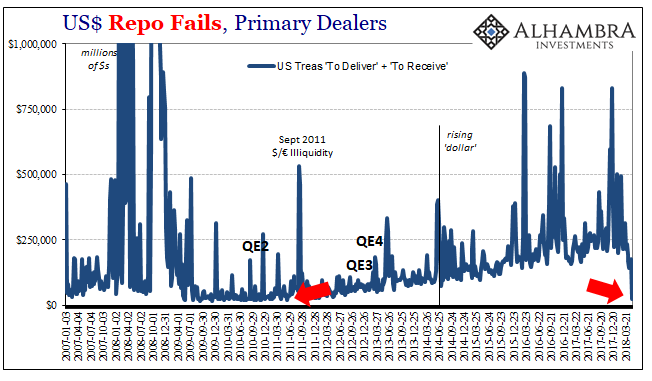

With the euro now trading under 1.18, I figured it was a safe bet that we’d later find out during this period since mid-April there would have been another spike in repo fails. Fails aren’t necessarily a coincident indication. At several times in past eurodollar events, they have led, at others lagged. Given the surge in indicated dealer hoarding in the week prior, the week of April 11, a jump in fails at some point seemed almost guaranteed to go along with this increasing “dollar” mess.

Quite the contrary.

FRBNY reports today that there were practically no repo fails last week. The total combined (“to receive” plus “to deliver”) was $22.9 billion; not $229 billion, as had become almost the baseline, but a level so low we’ve not seen it in the fails data for seven years going back to just before the outbreak of the 2011 crisis.

This is some pretty weird stuff. Perhaps it was a misprint or typo in the FRBNY data. While that’s not impossible, it would have had to been applied to both sides (“to receive” as well as “to deliver”) making it less likely. But the New York branch also reported a serious collateral de-hoarding coincident to what I’m going to call the week of no fails.

The pattern itself is not unprecedented. In 2008 as well as 2011, when some of the truly worst stuff was going on repo fails were not a pressing issue. They had in both cases preceded all that, and indicated systemic problems that were likely breaking out in that way. Again, as a coincident indication they weren’t always there.

What’s unique, obviously, is the scale of the decline this time around, particularly in how it is such a clear change from what’s been standard operative conditions – as well as the specific period in which this has happened. The week of May 9 saw some of the biggest currency declines since the last “rising dollar” and they hit practically everyone (including to limited extent CNY).

Is this overseas capacity being asked to contribute collateral strictly to domestic participants? A one-way collateral call that offshore can’t meet? It might explain the different direction reported for overseas collateral stock from what the limited view domestically (and repo fails only apply to what repo market transactions are reported by primary dealers operating in US capacities) is suggesting. There aren’t a lot of answers here.

Another possibility is intervention. But who? Certainly not the Fed and not likely any of the ECB, SNB, or equivalent (BoJ and BoE would be the two most likely candidates, especially the former given TIC data). To whom? Through what channels?

As if we needed any more to investigate, it has gotten real interesting yet again.

Stay In Touch