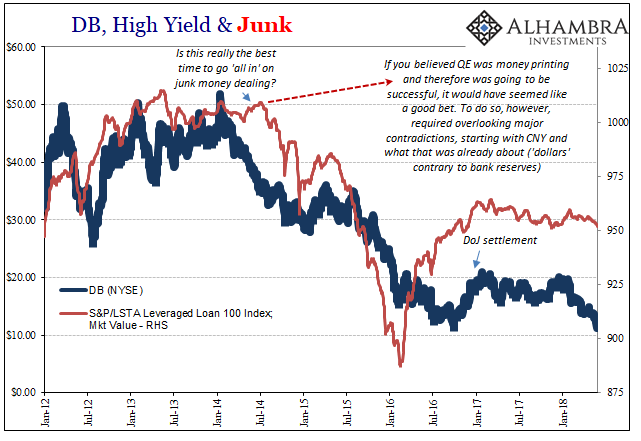

You need only go back a little less than two years for an example. In later 2016, Deutsche Bank was a huge problem everyone was discussing if only because they couldn’t avoid it. Despite “reflation” then gripping much of the world, the German institution stood out for all the wrong reasons.

Those were easily dismissed as nothing other than an impending fine for housing bubble era wrongdoing. The US Department of Justice was going to slam the bank with an enormous penalty and its potential size was supposedly the reason investors were getting nervous. Rumors were swirling that it could be more than $10 billion, perhaps $14 or $15 billion. At that level the bank’s capital stance would be severely threatened (and might trigger coco’s and such).

In January 2017, Deutsche settled for $7.2 billion. It would pay $3.1 billion in civil penalties (under FIRREA) while also covering $4.1 billion in “relief” to various affected parties (such as homeowners). A serious forfeit, but nowhere near as much as had been feared.

After falling below $13 per share (on the NYSE) in September 2016, DB’s stock rose as prospects for a reduced settlement gained in perception. By the time it was announced, the stock had recovered to more than $20. End of story?

Not quite. As I wrote in September 2016:

While attention is rightly focused on Deutsche Bank it is only so because the bank is the most visible symptom being the most vulnerable participant in this “something.” DB is just an outbreak so prominent that the mainstream can no longer pretend there is nothing worth reporting – but they can still obscure why that might be, focusing on the canard about the DOJ settlement. This is a systemic issue, one that is as plain as Deutsche’s stock price.

That’s ultimately what’s important to understand here. The DOJ issue was as residual seasonality, 2a7 money market reform, and everything else. Media attention starts from the premise that everything is good and great, and never deviates from it. Therefore, whenever something comes along that challenges the narrative there is an intense, often desperate search to explain it as something other than it is.

It doesn’t matter if it reaches into the bizarre or absurd, so long as whatever can sound plausible ends up looking benign. DB was in trouble because of long ago transgressions that have nothing to do with its current capabilities and certainly cannot sully the outlook of the awesome future the world’s genius technocrats have laid out for everyone. It always sounds legit, which is the point.

But it is not true. It never is. I’m not claiming Deutsche is the next Lehman, either; they aren’t. That’s the other side to this issue, those who immediately go to the other extreme.

The bank’s struggles are real and they are, in fact, systemic in nature. DB isn’t alone in that regard, but, as I wrote in 2016, they sit at the more visible end of the spectrum. News broke recently that their US operations were secretly placed on a Federal Reserve watchlist. The irony of all this is beyond tragic, since the bank finds itself in this situation because it had followed too closely the overall macro narrative developed by that very central bank.

I wrote a few weeks ago that what got them into so much trouble the last few years was they did what Ben Bernanke and Janet Yellen proposed they do. They believed in the recovery and committed to it.

Recall early 2014. The Fed had already started to taper its final two QE’s and expected that economic risks were shifting in the economy’s favor; so much that central bankers began to think about not just their exit but one fraught by potential overheating. The very thing they talk about today they near shouted about four years ago…

But DB wasn’t just buying junk bonds or leveraged loans and storing them in inventory. They were no investment fund, they were seeking to reclaim at least some part of the past pre-2007 glory. They were going all in on US junk money dealing, the FICC parts that allowed the explosion of leveraged loans all around Houston and beyond.

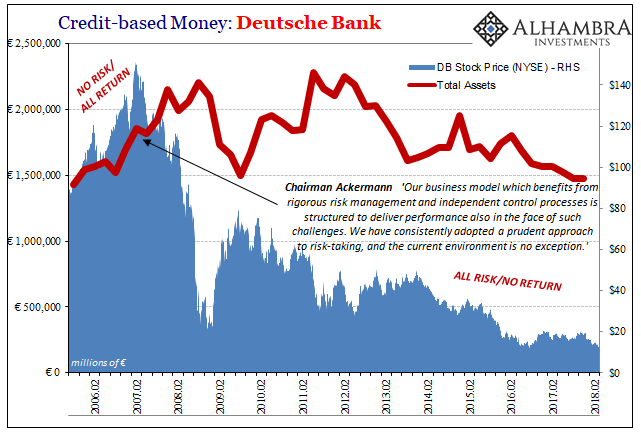

Today, the bank’s press release contains all the words and reassurances that contrarily conjure up all the wrong sorts of ideas. It says the bank is “very well capitalized” and “has significant liquidity reserves”, the very things you are forced to say when people really start to question your capitalization and liquidity reserves.

Only this time in May 2018 it can’t have anything whatsoever to do with the Department of Justice. Not that it did two years ago, either. It never is what they say. The truth is much simpler, and more depressing. We’ve never recovered from 2008. Some banks learned long ago the full range of what that means, still the hard way, while others are being subjected to the hard lessons of modern credit-based money.

It’s hard to believe now but in May 2007 DB’s stock was trading for more than $150 per share. It did so on the premise that eurodollar banks were valuable franchises (in the 2009 words of Ben Bernanke). The stock has lost almost 90% of its value over the last eleven years not because of civil fines, money market reform, or Dodd-Frank regulation (or whatever anyone in the mainstream might dream up next to “explain” why it can’t be a broken money system), rather the global system irreparably changed on August 9, 2007. There are consequences to that for Deutsche Bank still to explore, and those are very much related to those for the global economy as a whole.

Stay In Touch