The FOMC is almost certainly going to raise the federal funds corridor today. The only question is whether IOER and RRP will go up by the same amount. The issue with federal funds as an offshoot or reverberation of what really matters (offshore) should take center stage, but it won’t. Instead, the Committee will pretend this is about wages.

They really have no alternative, at least not any realistic one. The only factor whereby these “rate hikes” are consistent with a general overview of successful economic policy is the unemployment rate. Yes, the CPI hit a six-year high last month, but that doesn’t mean it was high nor, more importantly, does it describe a situation where it might remain this way.

Policymakers know very well that the only chance they have of reaching the second part of their mandate (stable prices) is if the first part (employment) has legitimately been met already. But it’s never really been about unemployment, rather their mandate is for full employment. It’s a binary outcome at this point; either they get everything or they’ve accomplished nothing.

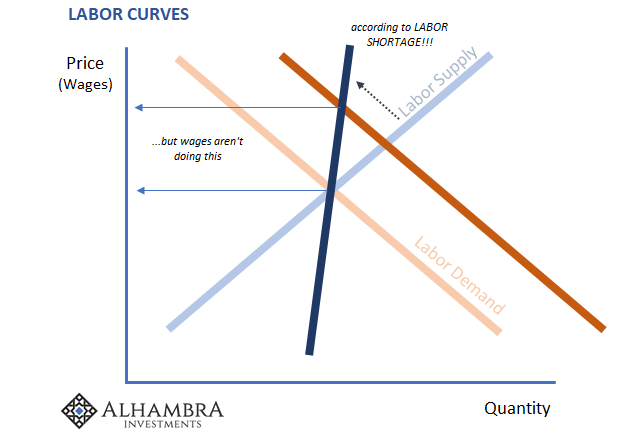

For it to be the former, then a ridiculously low unemployment rate requires accelerating wages. As described last week, this is basic economics that can’t be denied as easily as IOER’s tortured past.

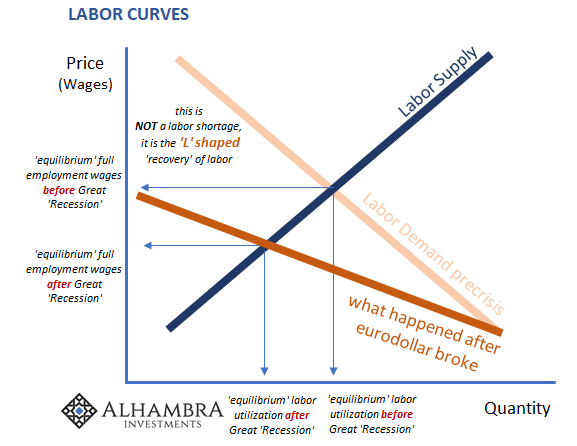

If we are in shape to become the first chart shown above, then things better change quickly, else time (further) proves the second. Again, there are only two options now after more than a decade of this: either there is a labor shortage due to demographics or a skills mismatch; or, the economy started shrinking eleven years ago, shrunk precipitously ten years ago, and then never came back for reasons we might be wise to studiously clarify.

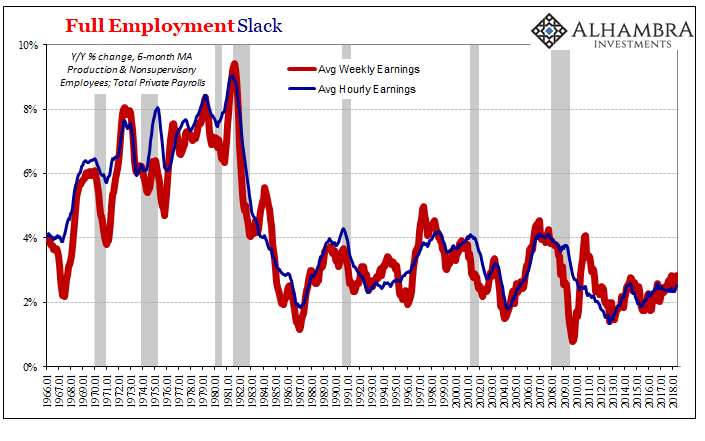

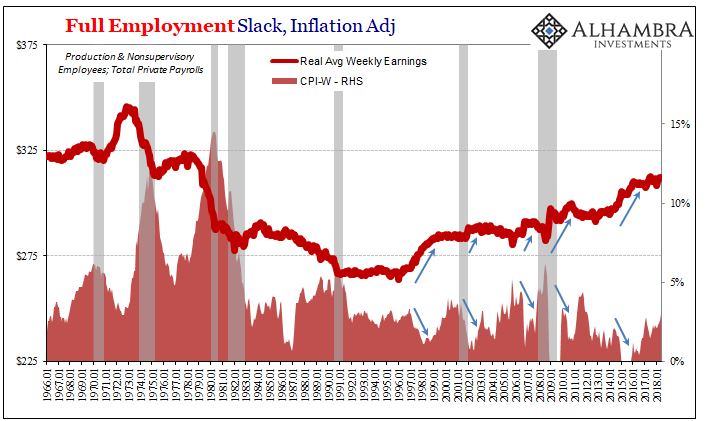

All of the employment data lines up against the unemployment rate. All of it. Wage and compensation figures are uniformly weak. They were worse during the downturn of 2015-16, but like inflation expectations (TIPS) or oil prices being higher than those comparisons it doesn’t mean things are good. Less bad than really bad may still be bad.

Aside from the unemployment rate’s mainstream relationship with the Phillips Curve, in truth wage pressures haven’t been inflationary in decades. You might understand to some degree why central bankers might be skittish and therefore over-commit to the ideal of inflation fighting, to resurrect the legend of Paul Volcker wherever possible.

It hasn’t been an issue since the seventies, not really anyway. And even then the contribution of wage pressures was in keeping going what was already a desperate monetary imbalance.

The US labor force is beset by an entirely different set of circumstances. There has been a tendency toward low pay and now participation. Policymakers are looking at this labor market in the wrong way. It’s not their first time doing so.

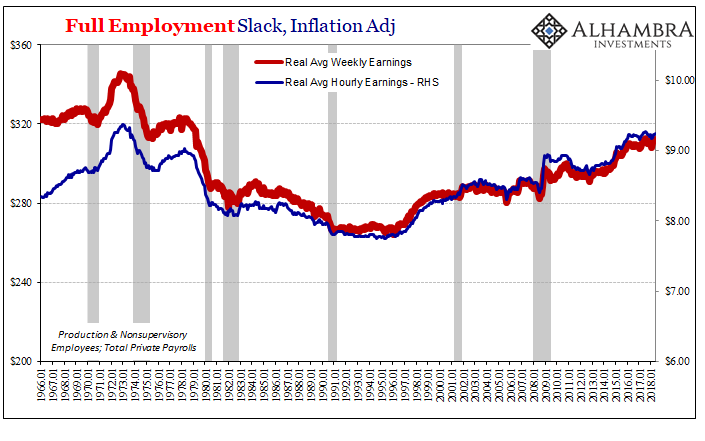

It was much simpler during the Great Inflation. Rapidly rising consumer prices rapidly rose more than rapidly rising wages. The effect was huge nominal increases in pay that didn’t keep up with the cost of living. The BLS figures that real average weekly earnings were between $315 and $320 in 1965 at the outset of the episode (in constant 1982-84 dollars). By the time of the double dip recession in 1982, real average weekly earnings had fallen by about 12%.

That’s unreal in any timeframe, but for a prolonged period extending seventeen years it was catastrophic. There is a reason the seventies are, overall, not remembered with much fondness.

It’s why in July 1979, President Carter delivered his so-called Crisis of Confidence Speech.

Confidence has defined our course and has served as a link between generations. We’ve always believed in something called progress. We’ve always had a faith that the days of our children would be better than our own…For the first time in the history of our country a majority of our people believe that the next five years will be worse than the past five years. Two-thirds of our people do not even vote. The productivity of American workers is actually dropping, and the willingness of Americans to save for the future has fallen below that of all other people in the Western world.

…

We remember when the phrase “sound as a dollar” was an expression of absolute dependability, until ten years of inflation began to shrink our dollar and our savings.

It sounds awfully familiar, doesn’t it? Other than inflation which is now more deflationary (beyond consumer prices) especially in the labor market, there is this renewed tendency to blame us for systemic issues that have little to do with us. Americans didn’t pull out of the gold standard, that was Economists who were totally unaware of the massive evolving circumstances of the global monetary arrangement. Carter was pleading with Americans to stop bitching about inflation and wages because he believed that bitching was the problem (confidence!)

He outright laid down that very accusation, recounting on national TV what a recent visitor had warned him:

We’ve got to stop crying and start sweating, stop talking and start walking, stop cursing and start praying. The strength we need will not come from the White House, but from every house in America.

Now, Economists are trying to claim it is workers again who are to blame. They are too lazy to go back to school, they say, when the local factory closes down and ships its jobs to Vietnam or Indonesia (not so much China anymore). The benefits of globalization would accrue to a much larger proportion if only we would stop bitching about what’s wrong and embrace what’s right, according to this view. Heroin is the new crisis of confidence.

And it was all crap. Carter was not just wrong, he was dead wrong. The problem in the 1970’s wasn’t OPEC or Gerald Ford and his utterly idiotic buttons (above), it was Economists. Even the US Congress finally came around in actual bipartisan fashion to seeing this truth:

The 1980 annual report signals the start of a new era of economic thinking. The past has been dominated by economists who focused almost exclusively on the demand side of the economy and who, as a result, were trapped into believing that there is an inevitable trade-off between unemployment and inflation.

This realization more than anything is what ended the Great Inflation, not Volcker. It was the widespread acceptance and then condemnation (which didn’t go nearly far enough) of what was truly gross scientific malpractice. There were then, and there are now, huge consequences to Economics and its doctrine of committed ignorance (econometrics, or Positive Economics).

The real difference between 2018 and 1980 is that the malady is much harder to see, the effects more obscured. It isn’t really that difficult, still within the monetary realm, it’s just not as obvious as double-digit inflation and interest rates. But therein lies the answer. The basic nature of our problems are the same, just pointed now in the other direction.

As Milton Friedman said in 1967 before the Great Inflation really got going:

As an empirical matter, low interest rates are a sign that monetary policy has been tight-in the sense that the quantity of money has grown slowly; high interest rates are a sign that monetary policy has been easy-in the sense that the quantity of money has grown rapidly. The broadest facts of experience run in precisely the opposite direction from that which the financial community and academic economists have all generally taken for granted.

He was right about what was to come in the seventies as that’s just what happened. And his simple observation holds in the 2010’s, even now as the UST curve collapses at just 3% on the long end. In both cases, Economists have had it backwards. They are what’s wrong.

But they are still held in high esteem today, and people the world over actually believe the Fed is “raising rates” when it’s not, and that its policy board members are doing so for the right reasons when they have no idea. Again.

Stay In Touch