As anticipated, the FOMC voted on both proposals in front of it. There should only be the one, but even routine monetary policy no longer is. Alan Greenspan’s Fed charged ahead with seventeen consecutive moves (the last few completed under Ben Bernanke) with little discussion about uncertainty in the economy (though there was, conundrums and all) let alone in the very place the central bank is supposed to operate with impunity.

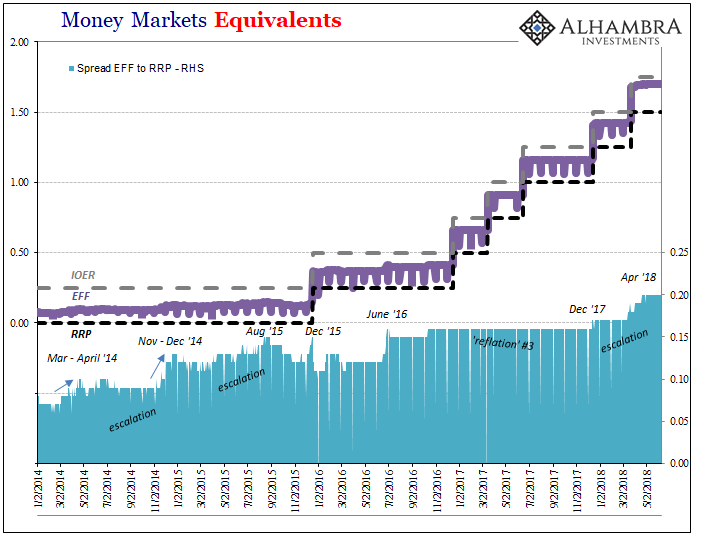

The result of today’s action is the first of what is almost certainly going to be asymmetry moving forward. Dating back all the way to December 2008 when policymakers mercifully scrapped the singular federal funds target, the FOMC object had been to maintain a 25bps band or corridor in which they would accept actual trading. As of now, that band has been reduced to 20bps; RRP was increased +25bps; IOER only +20bps.

It immediately brings to mind not just IOER’s failure, as noted before, but also the ECB’s. The European central bank had tried narrowing its corridor starting in May 2013, though with everything reversed. It is a topic that deserves greater devotion at a future date (was it Bernanke’s uttering the word “taper” that ignited the big storm that spring and summer or was it the ECB’s narrowed corridor announced the same day?), so for now I’ll just summarize their experience as the same as it was for the Fed in 2007 forward – losing control.

Beyond the unwelcome distraction in federal funds, the bond market is also not fooled. Jay Powell has displayed a little more showmanship than Janet Yellen, which isn’t a flattering comparison. There is a certain arrogance in his demeanor that is much too reminiscent of Bernanke. Yellen, at least, you always got the feeling she was a bit unsure which would have been much closer to the truth than Bernanke’s unshakable confidence (pictured below).

The yield curve continues to collapse because unlike the media which refused to offer any hard questions at these staged photo opportunities, the bond market understands the dramatic shift from even just a few years ago. There are big implications in these clear misses.

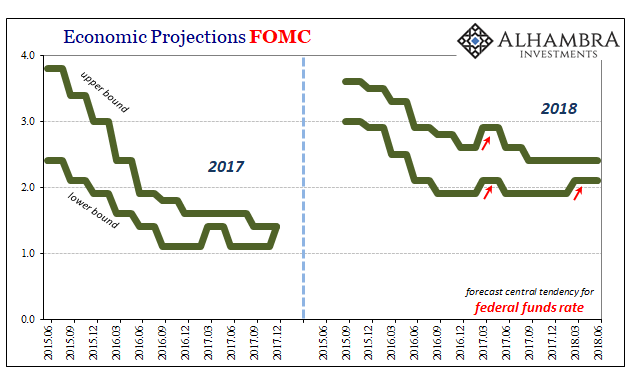

When the FOMC first began this meandering odyssey toward what it hopes ultimately amounts to something like normalcy, it did so in December 2015 amidst everything going wrong. Not only was the economy in the middle of a serious downturn, and the global monetary system a dangerous mess, the effects of that deviation have all but wrecked those prior expectations.

What I mean by that is incredibly simple. In 2015, the FOMC’s modeled projections for how their exit would unfold have been entirely erased. Jerome Powell’s task in 2018 is to try to explain how the economy could be so good at less than half of 2015’s numbers.

The statistical models under those prior assumptions forecast a federal funds band between 2.4% and nearly 4% on the high side for 2017; the Fed finished last year way short of either. It was expected that by the end of 2018, this year, federal funds would be no less than 3%. Nowadays, there is widespread uncertainty as to whether the FOMC ever gets that far (at least in the foreseeable future).

Even as late as the middle of last year, as a consequence of Reflation #3 the FOMC’s projections for this year’s federal funds were moved up to 2.9% on the high side. Today? That’s absurd, and it was only a year ago.

The mainstream focus on the dots is misplaced. What matters is not this meeting’s dots in comparison to last meeting’s, rather it’s how the economy didn’t come close to behaving as was expected just a few years ago when this exit strategy was mapped out. That’s not nothing.

It is treated as water under the bridge by the media and mainstream commentary, sadly, a fact of economic life to further ignore like all the rest dating back to 2007. It’s laughable that any of them, Powell included, can suggest with a straight face that the economy is anywhere close to overheating or above-trend growth. It isn’t even living up to what were already diminished expectations when all this began.

What’s keeping the Fed from acting more confidently is that underneath it all they aren’t confident in anything – including IOER and federal funds. Powell today characterized it as uncertainty when in one respect it is perfect certainty; they really don’t know what they are doing.

A comment written in the Wall Street Journal this afternoon pretty well sums up the situation:

Mr. Powell said the important thing is to make sure the fed-funds rate remains in its groove. The Fed may not need to make additional technical changes to make that happen, but that’s not certain at this point. The Fed will watch and try to learn more about what’s going on, but for now the goal is simply to keep rates on target. [emphasis added]

The whole enterprise has been staked to federal funds since the middle eighties. The whole thing. If in 2018 they have to “try to learn more about what’s going on”, then what are we really talking about?

They’ve had one job to do…

Stay In Touch