As a starting point, the TIC data is enormously helpful. Not only does it provide some badly needed level of detail, the series’ focus is right in the area where everything matters. Ostensibly about Treasuries being bought and sold in foreign places, quite by accident the Treasury Department has captured an introductory measure of offshore “dollar” money.

What’s truly helpful about that fact is that there can be no debate about “what.” For the shadow money system, this has been established beyond a shadow of any doubt.

Before we get into that again, our purpose here isn’t merely some academic type review. There are very real consequences to what’s going on now; of which, carefully crafting a view of things from across the last few decades is inordinately necessary to truly understand the risks involved. These apply in economic matters as well as those pertaining to purely markets.

I may snark about the stupidity of central bankers especially as they repeat their mistakes, that’s because there is the very serious matter as to whether Reflation #3 might have already run its course.

The mainstream says no. They always answer in the most optimistic fashion, so it’s easy to dismiss the consistency. This time, however, they have some theories. What’s different in 2018 is that the Fed is for the first time aligned with any potential “tightening.” Therefore, unlike prior episodes, Economists feel somewhat more comfortable actually acknowledging this reality rather than trying their very hardest to hide or ignore it.

They’ve concocted this ridiculous story because on the surface it sounds plausible to anyone with more than a passing interest in money and economy. To the layperson, it’s all Greek. Thus, if they can convince the majority of people in the first group it will be repeated as if to the second.

Briefly, the Federal Reserve is slowly running down its balance sheet the immediate consequence of which is a reduction in the level of bank reserves. At the same time this has happened, owing in large part to December 2017 tax reform, the federal government has had to increase the amount of Treasury bills it auctions in order to pay for the greater deficit it has necessarily created by tax cuts.

Dollar tightening, mainstream version.

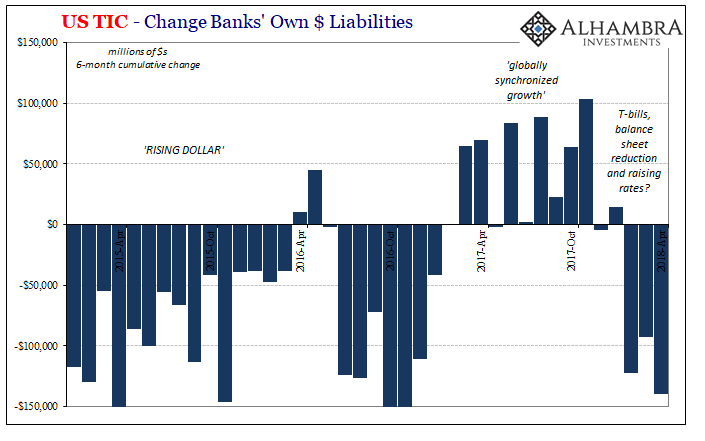

TIC figures particularly as they relate to reported foreign dollar liabilities (back and forth) do suggest that “something” has changed recently. But if we are to infer T-bills and QT into the latest possible reversal, then consistency matters. We certainly can’t use those things to explain the almost regular gyrations in bank liabilities that stretch back the entire length of what hasn’t been an economic recovery.

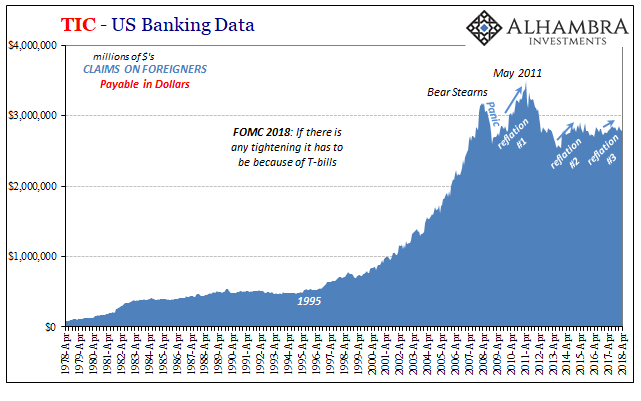

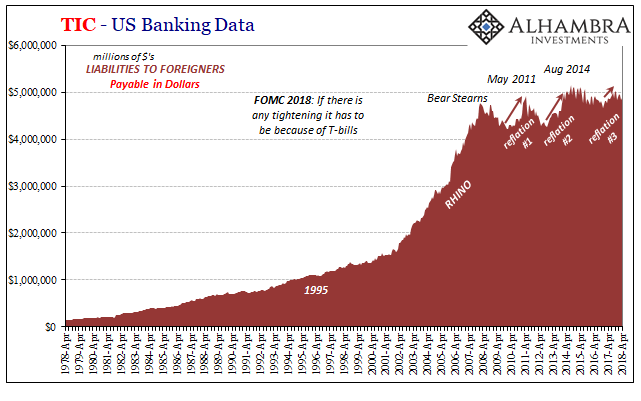

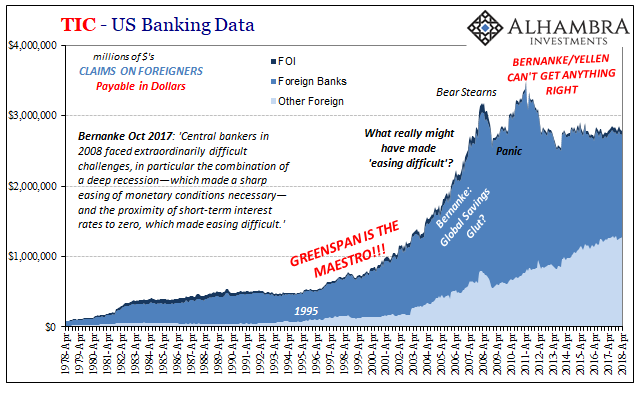

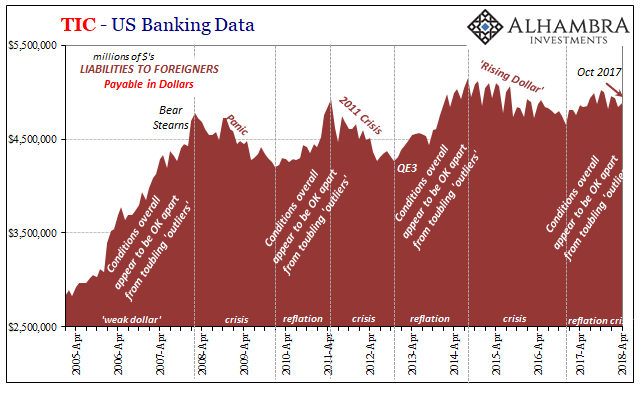

The issue is further crystallized when we take the same data and view it by levels rather than by changes in levels.

All of a sudden, those fits and starts pale in comparison to the larger problem at hand. The offshore money system grew until Bear Stearns failed, and then it stopped. No amount of QE or bank reserves has been able to restart the global program. Instead, these mini-cycles since 2007 appear to be consequences of the overall failure; how banks are attempting to deal with the breakdown, which differs depending upon immediate circumstances.

This is the part about which there can be no debate. The matter is simple in terms of “what” as you can see below:

It appears consistently on both sides of the offshore divide. Non-bank participants are largely undisturbed by any but the biggest crises. These are everything from money market funds to EM mutual funds to foreign trust concerns operating as various sorts of shelters.

The systemic retreat is an exclusive feature of the bank channel.

That’s an odd development given the narrative about QE, and thus applicable in evaluating the significances any possible QT. Central banks have created trillions in bank reserves with several purposes (inflation expectations and portfolio effects) but by and large their focus has been exclusively banking. Monetary policy itself is all about banks.

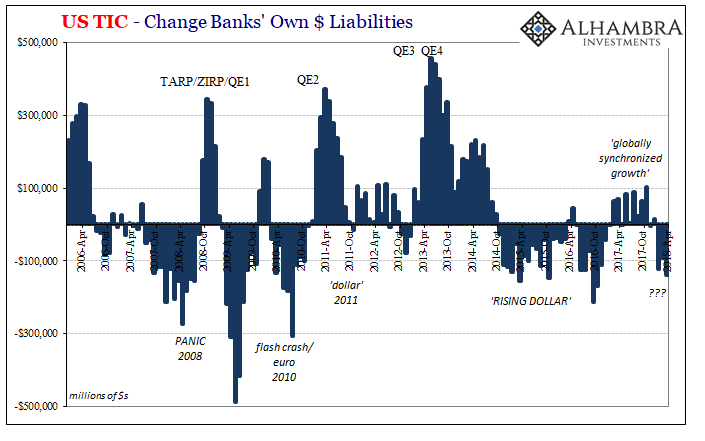

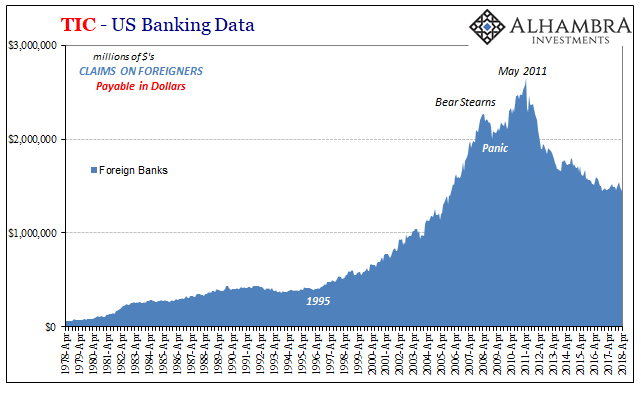

The chart above for the outbound monetary side (US banks lending dollars to foreign institutions) is incredibly compelling for dismissing the common narrative about QE. Money market fragmentation that appeared in August 2007 turned fatal in March 2008 with Bear Stearns. That showed both that there were very serious consequences to global dollar liquidity risk (LIBOR vs. federal funds, or OIS if you like) and more so that the Fed wasn’t fixing it (or even putting a dent in it).

The system partially rebuilt in the aftermath of the 2008 panic on the premise that maybe LSAP’s and QE’s were the difference. The 2011 crisis established, unambiguously, they weren’t. The result has been quite the opposite of easing through the US bank channel into offshore spaces.

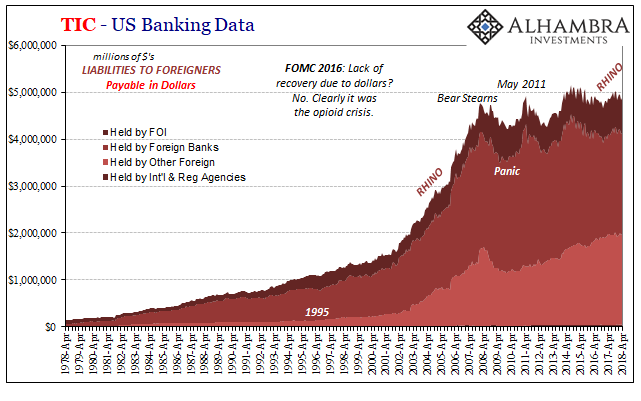

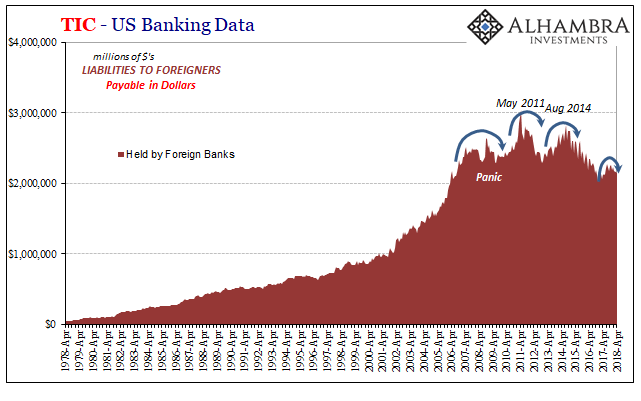

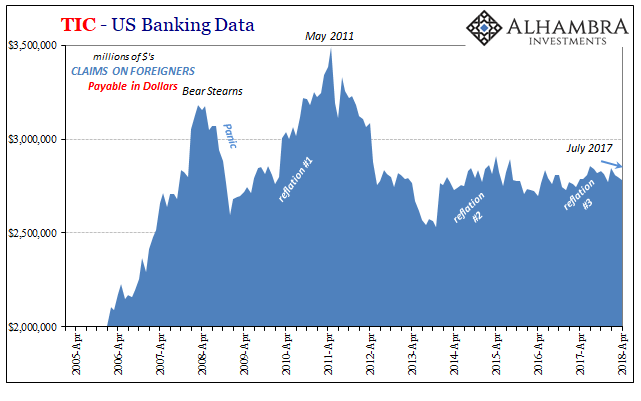

We find the same thing if to a lesser degree on the inbound side. US banks ostensibly borrowing dollars from the offshore markets suggests something about the availability of overall monetary funding in those places. The last three crises that have so far appeared are perfectly silhouetted, especially the “rising dollar” which grew serious later in 2014.

The repetition of that template thus possibly applies for 2018 (as marked above). In other words, it isn’t just about the last few months, rather what’s really indicated is potentially how this period might fit into what is a clear oscillation of funding/monetary conditions.

This year is far from unique, which it would have to be for the T-bill/QT theory to be valid. Dating back to October 2017, there is to this point (through April 2018, the latest figures) every indication of not just a systemic reversal but another systemic reversal along the same lines as before. QT, properly understood, would be a paradigm shift. What’s proposed in all this data is the same paradigm that has unfortunately existed since August 2007.

The more recent shift isn’t as clear for the reverse side (outbound), but that’s to be expected given the post-2011 behavior of the banking system in this direction.

To sum up, we know what the deficiency is and has been for a very long time – banks. That’s a big problem for the idea of QT since it very clearly shows there was no QE; or, more specifically, QE didn’t end up doing any E. The level of bank reserves has been entirely irrelevant for reasons I’ve briefly sketched out before. That would leave the T-bill angle in isolation, which only makes it all the more ridiculous than it already was.

Instead, the more serious implications are for the increasingly developed outlines of restarted “dollar” reverse. What is being proposed by the TIC figures is an end to Reflation #3 in any meaningful monetary fashion however it may have kept on in the last bond market selloff later last year (still the curve collapsed, which is the more consistent element to the trading during that time).

We have all the indications of tightening, but not as the mainstream would have it because this would be renewed tightening of a variety we’ve seen before. You may not have heard about it in any FOMC member speech nor read about in a mainstream article, but that’s perfectly in keeping with everything you see above. So far as they are both concerned, all that’s changed is that the Fed has finally aligned its intent with repeated(ing) monetary reality. Correlation is not causation.

The cause is what ultimately matters, and TIC is especially helpful in clarifying it.

Stay In Touch