That didn’t take long. The Fed’s IOER scheme lasted all of three trading session. That it was broken yesterday of all recent days isn’t surprising, at least when you realize the full range of things going on yesterday.

First, a review:

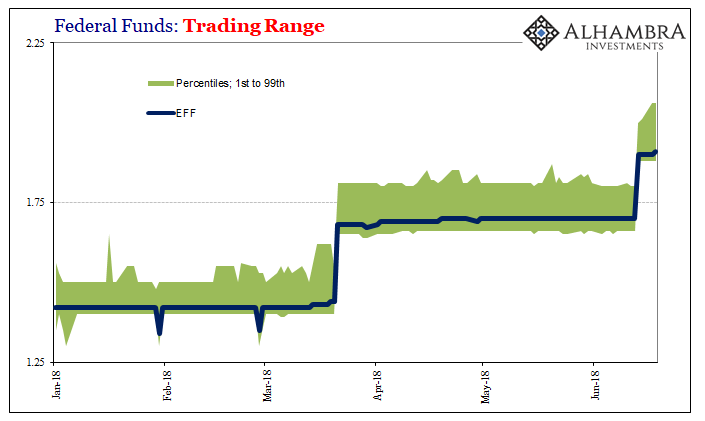

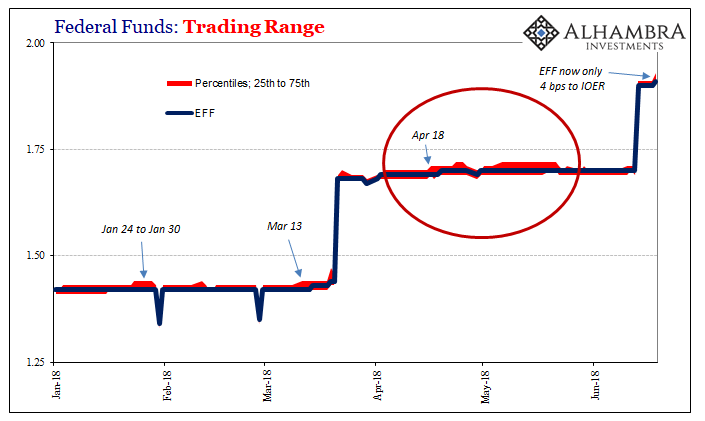

The issue this week, perhaps, is again EFF only this time the effective rate is pushing a little too high for the FOMC’s comfort. It is still less than IOER, but since mid-March that distance has shrunk to just 5 bps.

The bigger issue is, as always, they really have no idea why EFF is exploring the upper ends of its range.

At the last “rate hike”, the FOMC decided (hoped) that by reducing the distance between EFF and IOER it would add positive pressure on EFF so as to keep it from rising too much further. The acceptable policy range as of last week was shifted to 1.75% to 2.00%. Before this last change, IOER had been set equal to the upper boundary.

To hopefully push EFF away from possibly violating that limit, IOER this last time was recalibrated to 5 bps below the upper end (1.95% rather than 2.00%). Since EFF had been running at a spread of 5 bps less than IOER, for the first three days of the new regime that spread held. That might have proposed with EFF holding steady at 1.90% IOER had initially proved effective (or perceptions of IOER) at keeping EFF at 10 bps below the top rather than the 5 bps when IOER equaled the upper bound.

Yesterday, however, EFF moved up to 1.91% narrowing the spread to just 4 bps to IOER and now 9 bps to the upper end. Again, that’s consistent with happened yesterday. This doesn’t mean that any tightness in federal funds was responsible for selloffs (particular around Asia), rather it’s very likely the other way around. Whatever negative “dollar” pressures may have developed (CNY DOWN among the many), they were sharp enough to have registered in federal funds by this seemingly minor violation.

The top end of the transaction range has been responsible for pulling up on the average. EFF is not a singular rate, rather it is an average of actual transactions that take place across a range which FRBNY helpfully publishes. The 99th percentile jumped up to 2.06% from 2.01% on Monday, suggesting negative pressures may have emerged while Chinese markets were closed.

On Tuesday, the 75th percentile hopped up 2 bps to 1.93%. So far this year, whenever the 75th percentile moves it aligns closely with recent events – including the obvious change on April 18 right at the start of the EM currency drama.

Did anyone check the T-bill auction schedule yesterday?

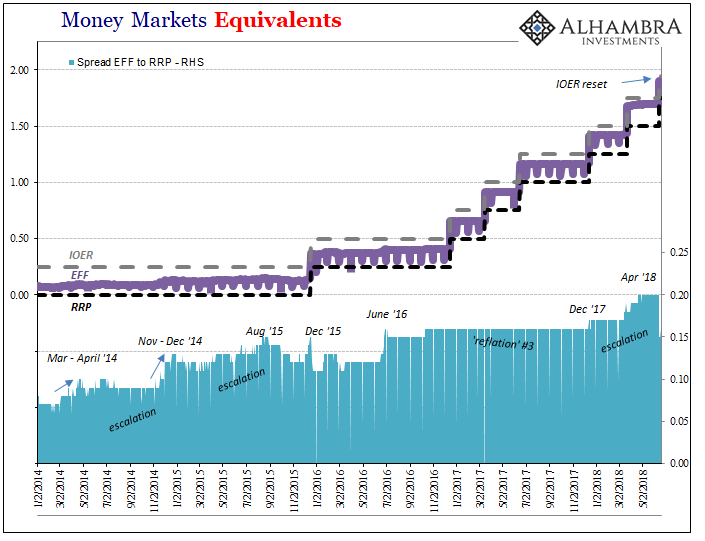

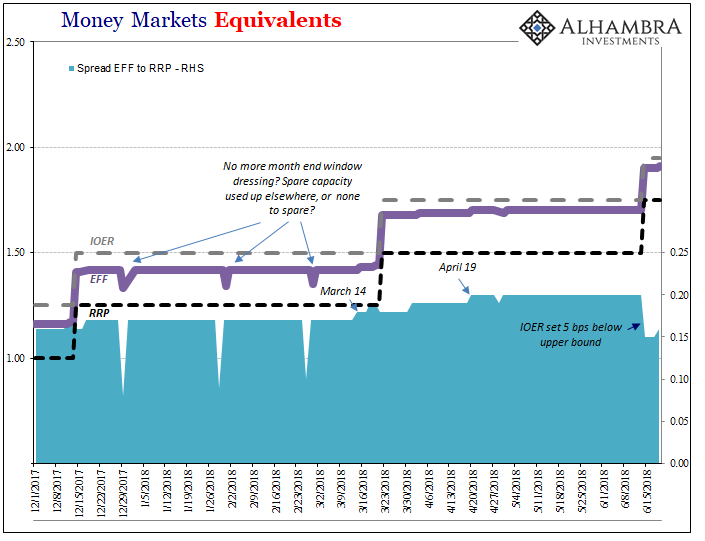

That’s not the only change. Notice how EFF no longer exhibits a month-end drop. Banks apparently aren’t dumping excess capacity into federal funds at the conclusion of each calendar month and haven’t done so since the end of February – right when the EM matter began to take off. Where did the spare funding capacity disappear to? We know it wasn’t QT because there isn’t QT.

Stay In Touch