I don’t know if I should make this a regular feature or not, but IOER is the one monetary policy factor that maybe is easiest enough to understand and therefore the quickest route for the public to get to they really don’t know what they are doing. Federal funds aren’t some obscure way off policy goal, it’s the very lever the Federal Reserve has claimed all along it has been using for decades to great positive effect.

It’s a logical fallacy to merely assume that if you get one thing wrong the whole thing is. In this case, however, that one thing was supposedly all that mattered for everything. Therefore, if you don’t know much or anything about that one thing…

No one was paying attention in 2008, so hopefully repeated attention will do the trick.

Let’s recap IOER again in 2008 using the guy who in 2018 edging ever closer to retirement has decided to change his tune a bit on the subject of federal funds. Beginning with October 7, 2008, right at the start of the experiment:

MR. DUDLEY. That’s why getting interest-on-reserves authority was very, very important. As Brian has said in earlier briefings, interest on reserves is going to start on Thursday, and that’s going to place a floor on the federal funds rate.

Just three weeks later:

MR. DUDLEY. …some banks have also been selling federal funds below the interest-on-reserves rate…As a result, there has been a significant amount of federal funds rate trading below the interest-on-reserves rate.

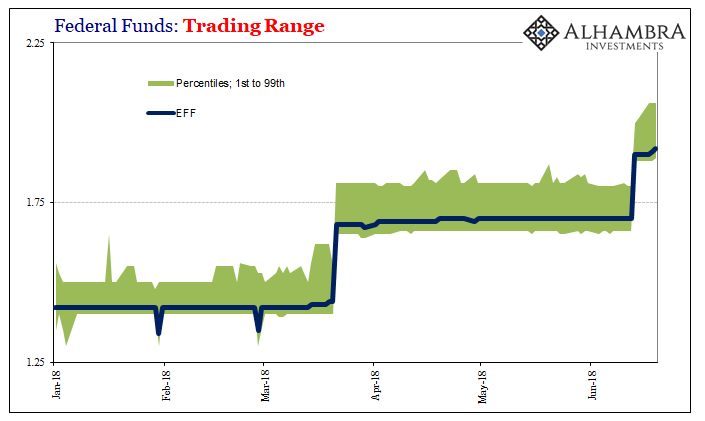

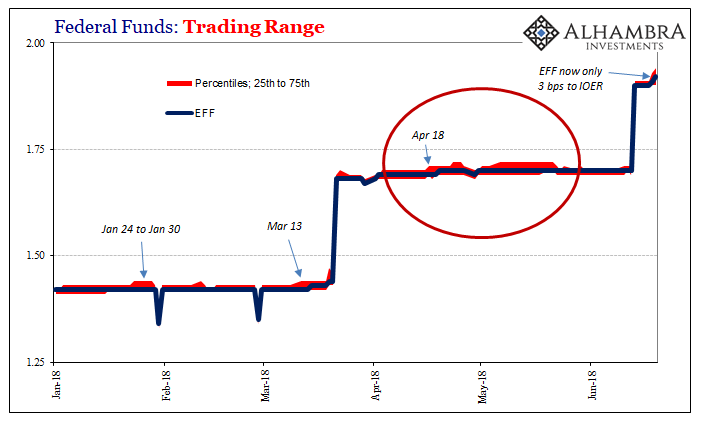

IOER was again used last week, adjusted downward from the upper bound so as to “ensure” the effective rate for federal funds (EFF) doesn’t get too close. Results only five days later are trending more like IOER’s effectiveness in 2008. Shocking.

Tuesday, EFF broke to -4 bps under IOER. Yesterday, – 3 bps. 75th percentile up to 1.94%, meaning about 25% of actual transactions took place right near, at or above IOER (as high as 2.06%). Tick, tick, tick.

Stay In Touch