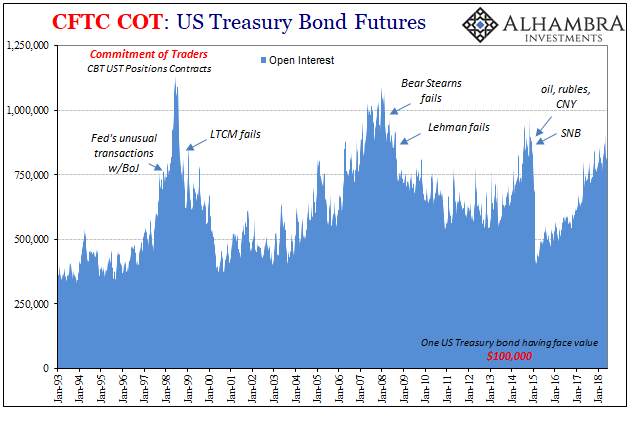

I doubt there will be an official report created and published surrounding the events of May 29. Unlike those on October 15, 2014, which did trigger a Treasury Department alphabet-soup-of-partners response, it wasn’t crashy enough this time around. The UST market experienced a true panic more than three and a half years ago, though one of buying rather than selling. Still, in a matter of minutes, yields collapsed. People tend to notice roller coasters.

Six weeks ago, by contrast, the collapse in yields was nearly as impressive in absolute terms but far more orderly stacked throughout the whole trading day rather than condensed into the alarm of a short span. Just not sexy enough for mainstream consumption and therefore government bother.

Not that it would make much difference either way. The official voluminous yet somehow empty report that came out was true farce in every sense. Computer trading was left for the blame in it rather than the obvious collateral (and junk bond) issues by then plaguing credit and money markets for months beforehand. It couldn’t be a monetary or dollar problem, so said the keepers of the money and the dollar. October 15, 2014, was not just a collateral call, it was the announcement that the “rising dollar” wasn’t to be just some annoying fad.

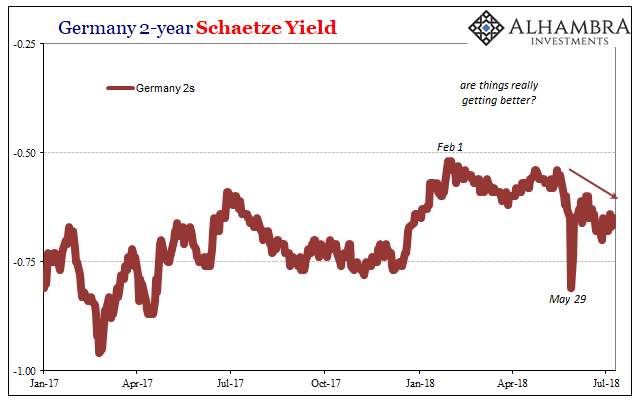

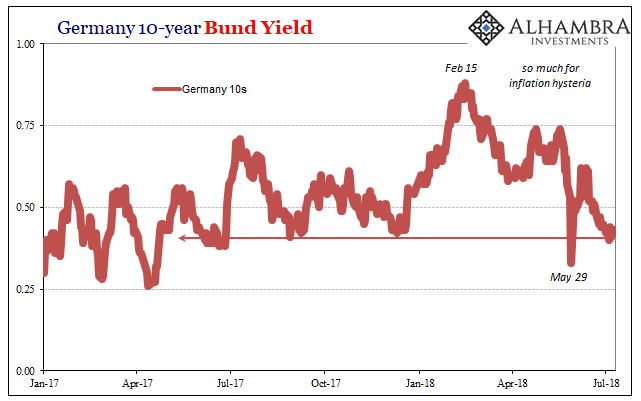

May 29 may prove to be a similar beacon. It has been just as much misunderstood, often purposefully. Italy rather than high speed trading was given immediately as the cause, though that might only be true in the very narrowest sense of initiating the global cascade. The bund market in Germany felt it more than the UST market here, a European epicenter fitting for the last few years of Europe’s rejoined “dollar” dealing.

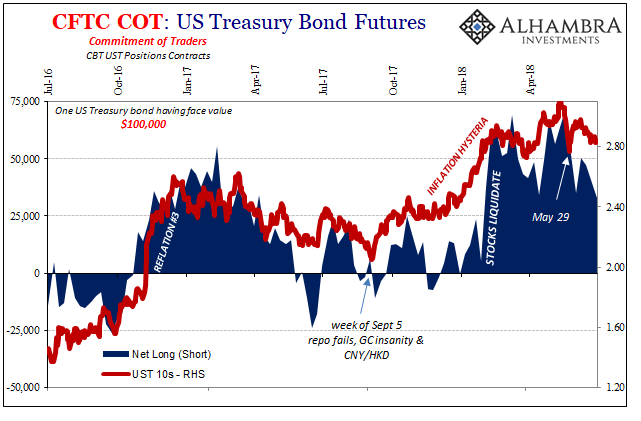

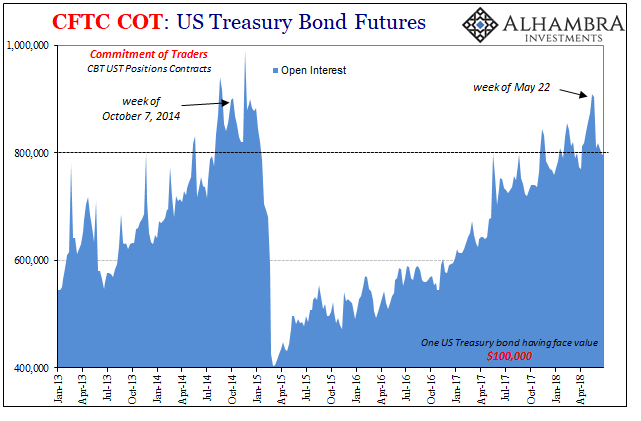

Up until the week of May 22, the week just prior, UST futures positions were decidedly negative for these securities if not for the whole global bond position in general. That is to say, futures were net long (thus short specs) as in reflation episodes past and present. Yields should have been rising, which they did as the 10-year rate surpassed its 2014 peak. But only to 3.11%.

Imagine that you are one of those betting on Economists to be right about economy for once. Like everyone else, you bought into the inflation hysteria because why not? It’s been eleven years and time is on their side, or it could be anyway. After all, they really seem to mean it this time.

Then, seemingly out of nowhere, the global bond market gets hit with a high magnitude quake like what registered on May 29. What do you do?

Such an extreme move could only trigger itself likewise extreme reverberations. Being caught the wrong way would almost certainly have led to sharp short covering. Indeed, the COT reports for the week of May 29 do show a collapse in the net long (spec short).

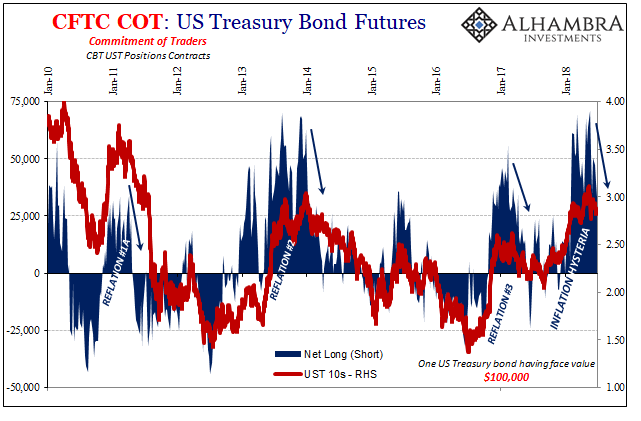

Maybe that’s to be expected, but it hasn’t stopped. The aggregate position has receded in the latest week (July 3) to the lowest since the big move in January. Now, the futures market is starting to look like the familiar disappointed repercussions that come after reflation inevitably fails. We’ve seen this, too, before. Three times (four if you count Reflation #1 and Reflation #1a separately).

It does make you wonder what futures traders might be thinking now into July. They first have to be asking themselves, “what was that?” It sure wasn’t Italy because here we are and nobody is talking much about that specific country yet oddly enough the same symptoms are getting worse. As I’ve noted in this place over the past week or so, a lot of other markets are moving as if a global shift is underway. There is much too much deflation (Dr. Copper, eurodollar futures) detectible of late than what might linger on of reflation or inflation.

It may be that the UST futures market gets right back on Jerome Powell’s side, or at least bets that Jerome Powell will be able to stick with his current forecast as he plans. The doubts, however, are starting to pile up, that maybe there is “something” far bigger going on out there in the offshore shadows.

Again.

Stay In Touch