If we are in the red on global eurodollar money, it makes sense to ask the question where we are in terms of global economy. What I mean by that is in the context of these repeating cycles.

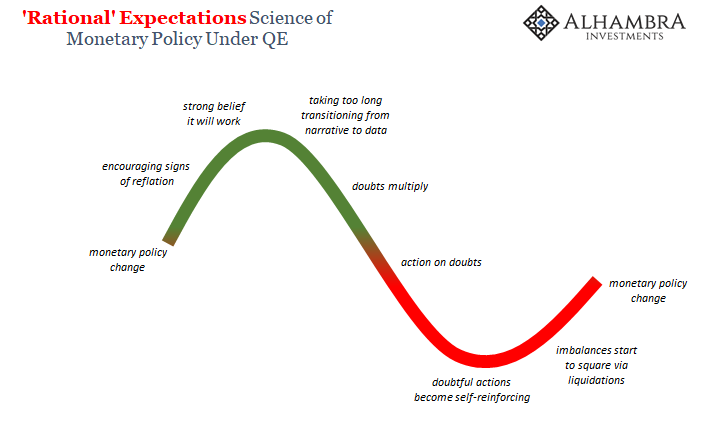

The world starts out enthralled by central bank or government actions when these usually come only after the ultimate depths of the monetary mayhem. Reflation takes hold in sentiment buoyed by the return of positive numbers that after only a short while this molehill becomes a gigantic mountain of recovery rhetoric. This is the upslope green.

The downslope is I think where we are now on the economy, but still in the green. Doubts are starting to creep up as economic acceleration has so far failed to materialize. This is one way in which inflation hysteria will work decidedly against those who practiced it so thoroughly. If you create expectations for something big and it doesn’t pay off, the “doubts multiply” section of the green can turn to red “action on doubts” in a hurry.

Small disappointments people get over quickly; big ones require emotions like fear, the heaviest transition catalyst. This is, I think, EM currencies, curves, and even some important commodities.

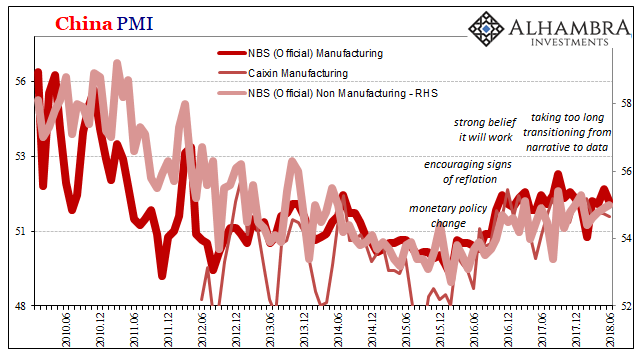

There are a few key economic indications that have in the past proved to be fruitful guides in marking progress along this cycle. Since China is at the center of the global economy both in terms of the supply chain (manufacturing and export) as well as supplying marginal growth underneath (occasionally filling in external weakness with internal “stimulus” that spills over), we focus on Chinese statistics anyway.

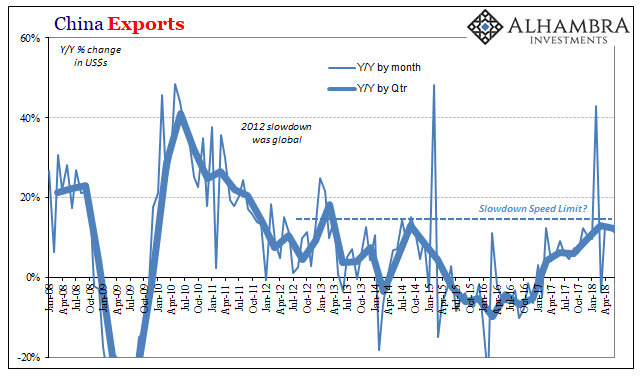

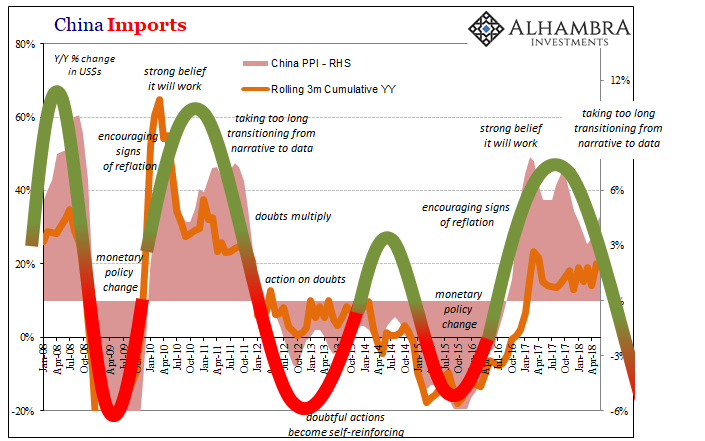

The trade data, however, has been consistent in mapping out what has proven to be the marginal direction of the global economy. The latest statistics for June 2018 released today were every bit the same as they have been since early 2017. Though the numbers sound impressive in isolation, they are actually a very clear representation of that downslope green – taking too long transitioning from narrative to data.

Chinese exports were up 11.3% year-over-year in June, almost perfectly in line with growth rates in April and May. For Q2 as a whole, exports increased 12.2%, down slightly from 13.0% in Q1. For China these are already low levels and there isn’t the slightest hint they are about to shift upward.

Even when compared to 2017, the increasing rate is very modest and not the sort of trend that would suggest what everyone keeps talking about. Instead, it is very much consistent with the post-2012 environment that contrarily suggests the same depressed state; a dangerously low ceiling on each and every cycle upswing.

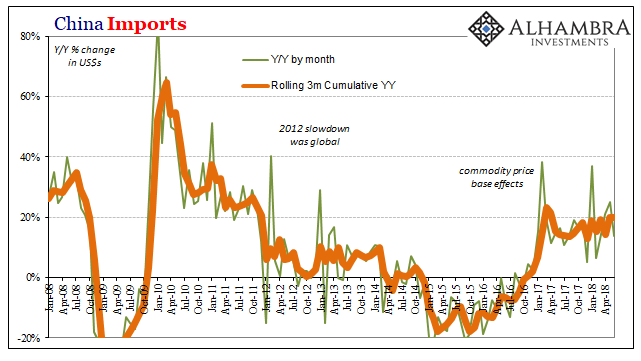

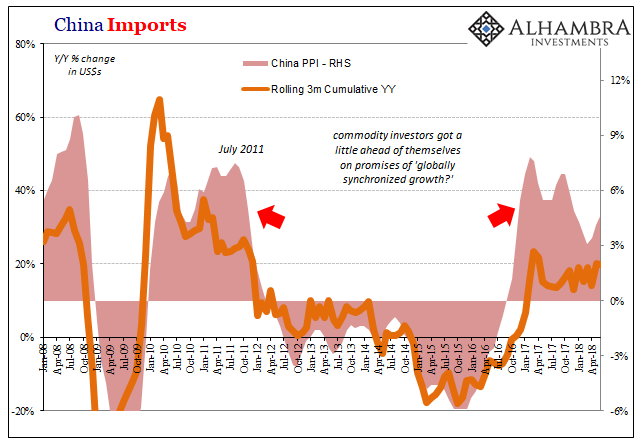

While we are left with that negative impression of the end demand component of the global economy (including the US and its 4% unemployment rate), China’s import side is even more directly crucial to economic development. Imports in June disappointed with just 14% year-over-year growth.

For the quarter, Chinese imports were up just about 20% from Q2 2017. Again, it’s an impressive sounding number that in reality is about half of what it “should” be.

Like exports, imports have been stuck for quite a long while without the necessary quickening that would confirm the idea of what globally synchronized growth is supposed to mean. Time is now working against it, this apparent low-level ceiling that doesn’t even match 2011 let alone pre-crisis or recovery features.

In rough translation, it seems to propose being somewhere on the downslope but still in the green. The economy isn’t yet falling off into the red where the eurodollar may already be, but we would expect a lag maybe even a significant one at times. This is about the only constant throughout the data, including those of and about China.

Last year was supposed to be an improvement upon 2016, and it was. That was expected to be only the first step toward this something bigger, the idea that all the world’s independent economies finally posting positive numbers at the same time would create energy and momentum. Real economic flight would follow.

There are no independent economies, however.

Each can maintain its own factors and characteristics, but they are inextricably linked by the one common element from which they can’t ever escape – not while it remains the only global monetary option.

This is why 2017 has proved so disappointing. Rather than being the first step it looks more like the only step this version of “reflation” was able to take; which makes Reflation #3 no different at all from its prior iterations. That’s a big problem which can only be confirmed by time.

As such, we have a pretty good idea of the general overview about what comes next. It’s not a boom, local or global.

Stay In Touch