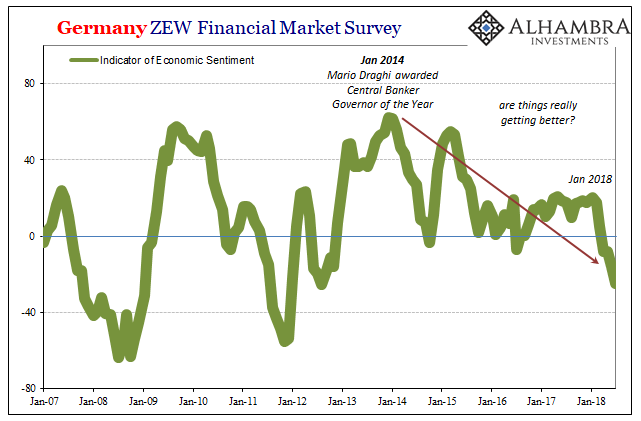

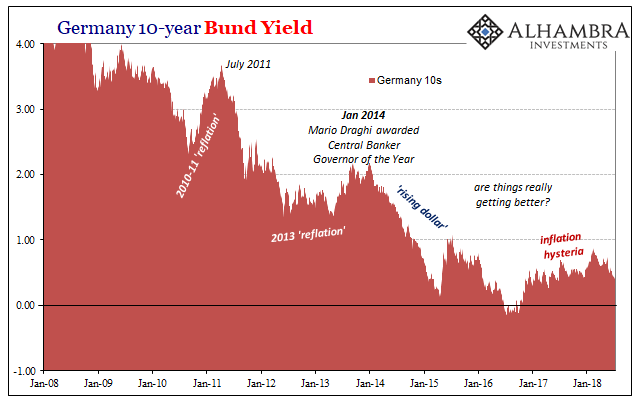

Sometimes it pays to wait. Better to be sure than premature. In January 2014, the journal Central Banking handed out its inaugural awards. Among the recipients was Paul Volcker who was bestowed a lifetime achievement prize. The initial Governor of the Year honorific, something like a central banker MVP, went to Mario Draghi of the ECB. He graciously accepted in the glow of universal acclaim for the “unflappable conviction” of his July 2012 promise and the broad, cautious optimism it had provoked.

On behalf of the Governing Council, executive board and staff of the ECB, I’m honoured to be named governor of the year by Central Banking. Thanks to both the ECB’s actions and hard work by governments in implementing fiscal consolidation and structural reforms, conditions in financial markets have gradually eased since July 2012.

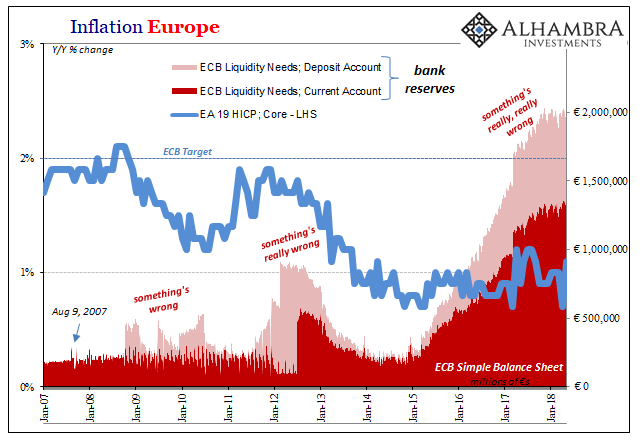

Just five months later the ECB was doing NIRP and a little less than a year beyond that the start of a QE program. This has as already expanded once, and as of the middle of 2018 it is still going.

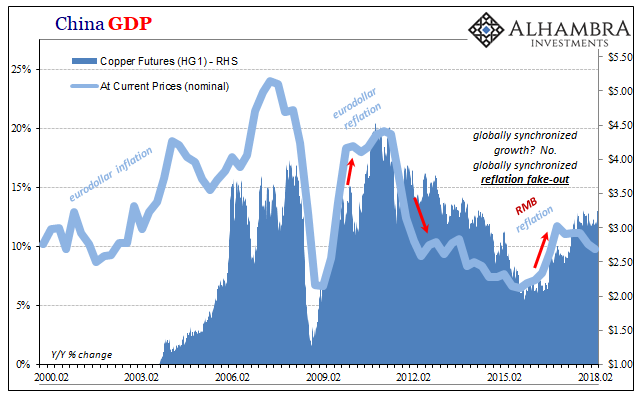

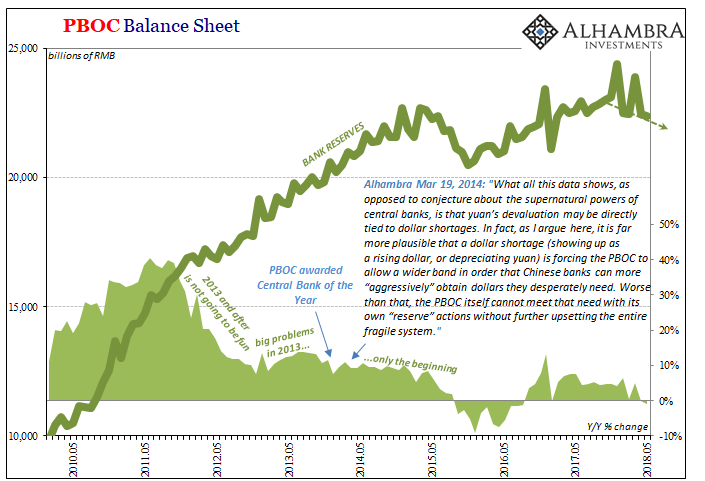

The big honor handed out was to the People’s Bank of China (PBOC) as Central Bank of the Year. If Draghi was league MVP, the PBOC was its champion apparently. In a very narrow sense, it might have seemed fitting given the struggles Chinese money markets went through in 2013. That summer was as eventful in SHIBOR as US tba MBS, if not more so.

Chairman of the Awards Panel, Christopher Jeffery, noted, “The PBoC demonstrated strong leadership in its efforts to curb excesses in the financial system, while at the same time pushing ahead with interest rate and capital account reform at a time of major political change.” The country had achieved economic expansion “faster than any other major nation in 2013” despite major challenges in politics beyond money.

As with Draghi, it may have been too soon for such recognition. Four years is an eternity in money. That’s especially true if you are a central banker who isn’t quite on top of banking and money on a global scale. Joseph Yam, a former executive at the HKMA in Hong Kong and an advisor to the PBOC, put 2013’s problems this way:

The liquidity squeeze was a reflection of an unsophisticated market panicking under guidance or encouragement from the PBoC to manage their money market books, in particular their funding for loans, properly.

Yeah, no. It may have seemed that way superficially in January 2014 because for one CNY was just then getting started on its “unexpected” reverse. The world hadn’t yet learned CNY DOWN = BAD because at the time there wasn’t any expectation for such a monumental change. At least not according to mainstream interpretation.

As noted many times before, however, there were warnings on top of warnings on top of warnings they (the PBOC, Mario Draghi, as well as all of Paul Volcker’s policy descendants and disciples at the Fed) all just ignored in favor of the useless dollar bank reserves of QE. Because they were useless, in China there weren’t even those.

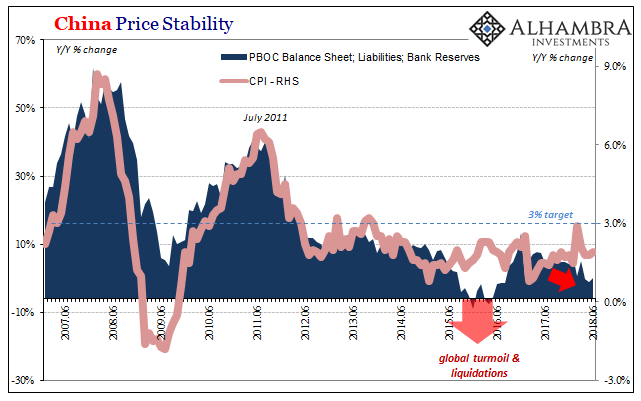

What happened in 2013 especially with regard to China was a big enough warning that things were getting serious, as they have in the half decade since.

The deflationary impulse that swept through the global economy in 2012 was real and massive, not something that QE3 and QE4 in the US could ever have handled (it didn’t). Mario Draghi’s “promise” that same year was a similar sideshow. All they accomplished was creating false expectations, the distance between economic reality and increasingly forlorn hope in commodities first before everything else following in 2014 and 2015.

The chart above shows pretty clearly just what everyone was actually facing at the time as a global whole rather than individually among separate constituent pieces. And though it may seem something like a tautology (commodity prices are an input into nominal GDP), the relationship above is confirmation of market to economy, all starting in the shadows of offshore money where no central bank, or central banker, can penetrate.

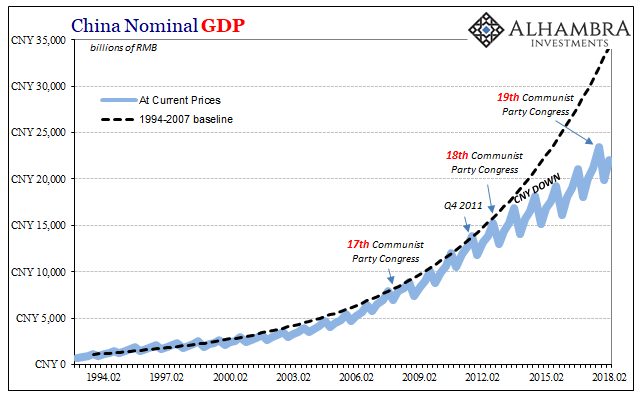

In other words, the PBOC hadn’t handled 2012 well at all, a fact confirmed by all the stuff in 2013 that foretold of the “rising dollar.” China hasn’t yet recovered from it, and given the way things are going now, more evidence provided by the latest data for Q2 2018, it’s not likely to in the foreseeable future, either.

This is where globally synchronized growth comes to us from, the same people who thought Mario Draghi and the PBOC both were on their way to great success in January 2014 – just as it all fell apart. History repeats because central bankers still have no clue there’s no money in their monetary policies. They do have awards, though.

Stay In Touch