It’s funny how these things work. He didn’t actually say the word “taper”, at least not when the frenzy first started. The very idea of the “taper tantrum” was the media’s work, the easy slogan that could be used as shorthand for the conventional explanation. The economy was improving, everyone was told and easily believed, therefore what was supposed to be open-ended QE begun the prior autumn couldn’t be unending forever.

In response to a question from Congressman Kevin Brady, Chairman of the US Congress Joint Economic Committee, about when normalizing monetary policy might happen Federal Reserve Chairman Ben Bernanke responded with “step down” rather than “taper.” This was May 22, 2013.

Chairman Bernanke. If we see continued improvement and we have confidence that that is going to be sustained, then we could in the next few meetings, take a step down in our pace of purchases.

It’s more than a little fuzzy in how we go from “continued improvement” to a major global currency crisis in the summer and then the hell that broke loose in 2014. It doesn’t really make much sense, though it does sound eerily familiar to our 2018 ears. Taper was, supposedly, tightening and that was why the world suddenly fell apart in 2013 only to suffer a worse fate starting 2014? We really were supposed to believe things were going to be so good they were bad.

Not quite.

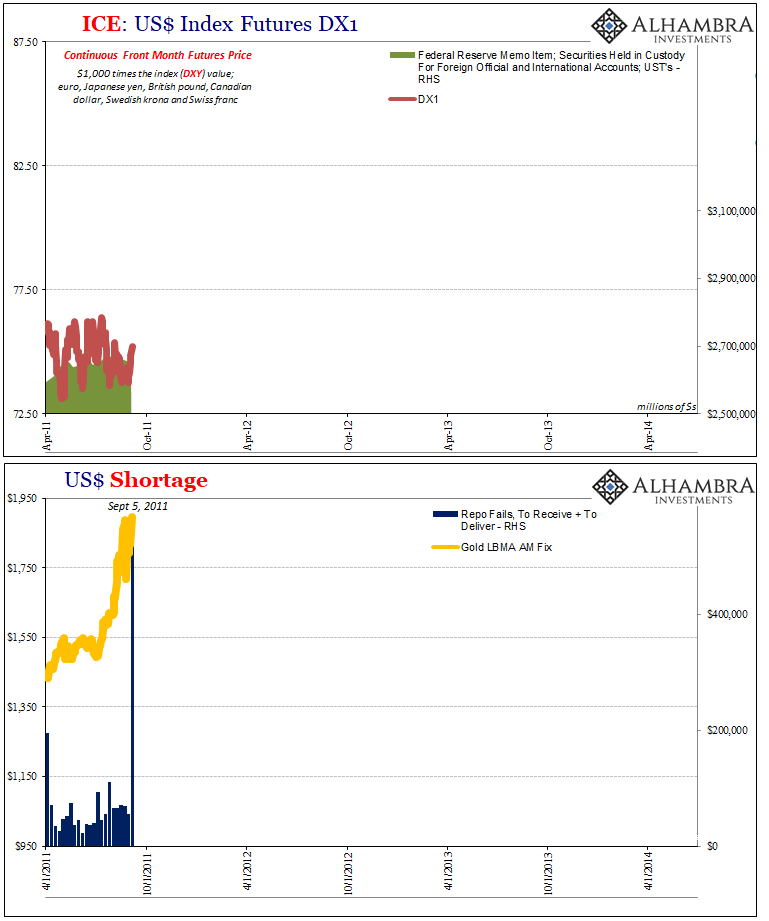

Before understanding the “rising dollar” we first have to back up and explore the deflationary wave that swept up into it. That means rewinding our review all the way back to the recovery’s shallow and unsatisfying peak in 2011.

It was a crisis practically no one expected and certainly not to the severe proportions presented to the global monetary system in short order. Especially not with $1.6 trillion in bank reserves, money supposedly having been printed by not one but two QE’s to that point.

Regardless of conventional views, in late July 2011 there was major trouble. It grew worse until September when things started to break everywhere, especially in Europe.

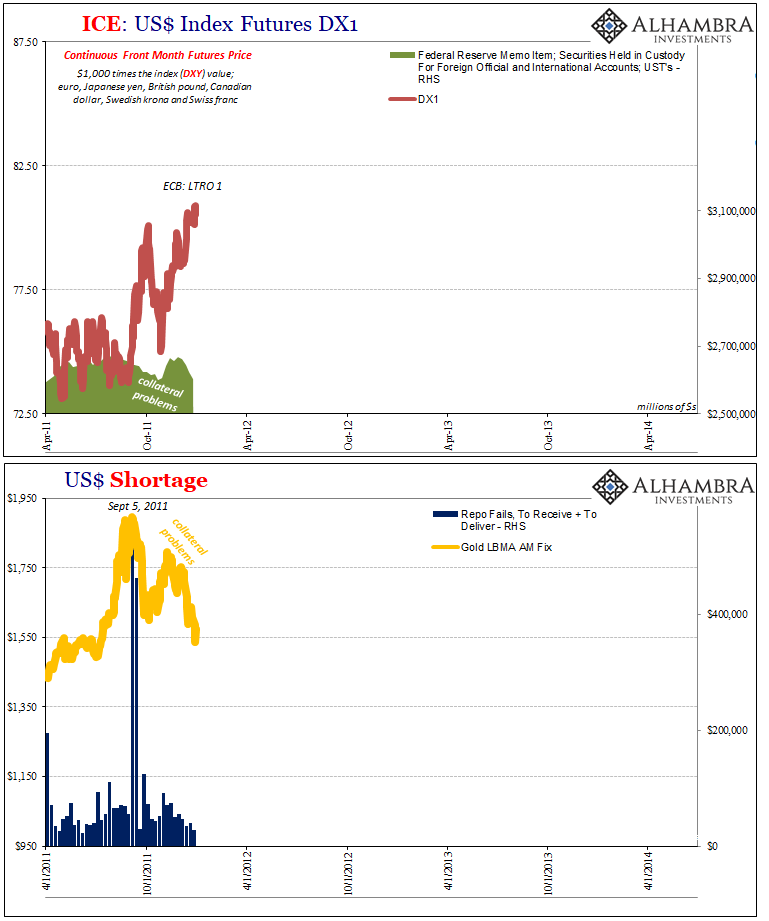

Eventually and belatedly (as always) central banks would begin to respond only after shaking off their total disbelief. It was the ECB that went biggest in December 2011 offering two massive (they said) LTRO allotments, the first scheduled for settlement on December 22. The ECB wasn’t alone in its actions, as several of the major central banks announced coordinated efforts that included dollar swaps with the Fed.

These didn’t work, though in every single news story published about the LTRO’s the word “liquidity” appeared in each; as in the ECB is providing ample liquidity via its current and deposit accounts (bank reserves).

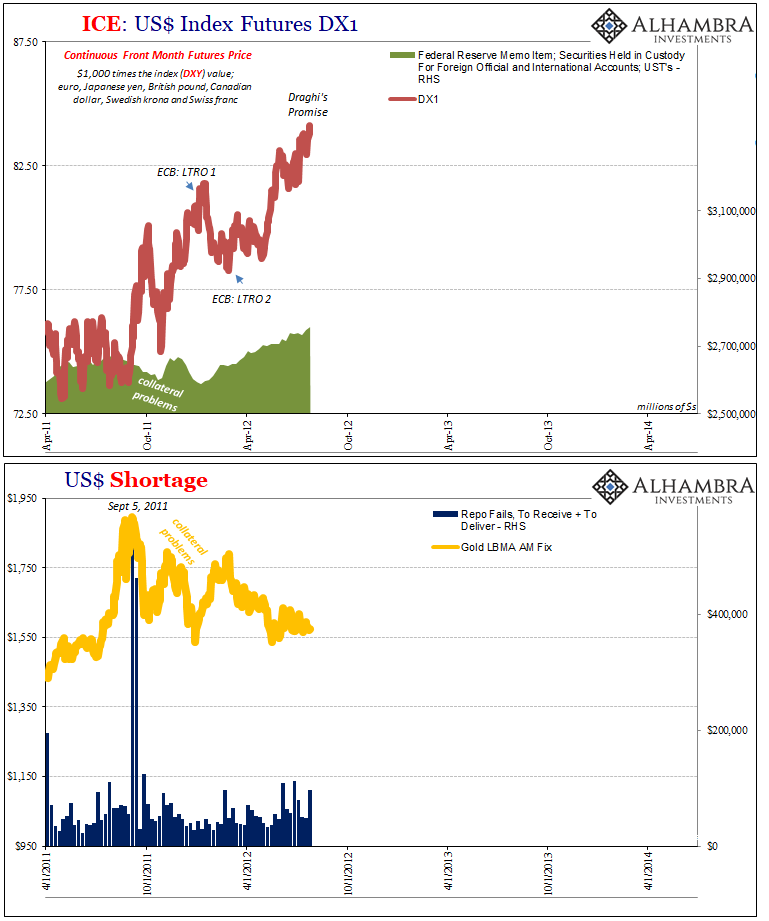

It wasn’t until July 26, 2012, when Mario Draghi was forced into issuing his “promise” to do whatever it took to save the euro. Thus began the next stage of larger central bank responses that included among them first a third then a fourth QE in the US. It is within this period that the conventional interpretations about economy and “liquidity” were arranged.

From this perspective, the “taper tantrum” still doesn’t really make sense, though, certainly not in the dimensions it took for the global system. But because central banks are treated as central, a narrative was created around Bernanke’s step-down intentions to try to bridge the huge intellectual gap. Taper was, they said, tightening.

Only it wasn’t.

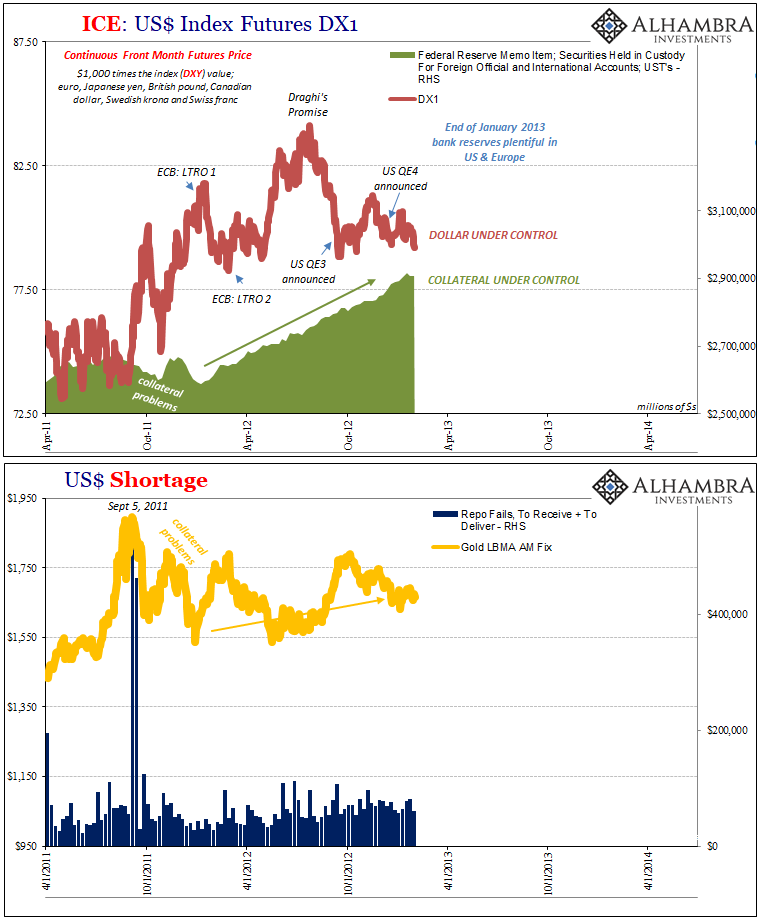

Anyone who has closely followed gold knows all-too-well that there were major problems long before Bernanke’s second Congressional appearance that year. The renewed “dollar” flareup especially in collateral terms hit months before, all the way back at the start of February 2013.

Looking at it this way we see that the interim period after Draghi’s promise containing the last two Fed QE’s wasn’t the beginning of the answer it was instead just another pause in the oscillating deflationary impulse still sweeping across the global “dollar” system. Nothing goes in a straight line; it was simply written that because of these pauses they must have been attributable to something some central bank had done only ignoring how none of the prior central bank actions had ever accomplished what they said they would.

If you have to keep doing things, these things aren’t working.

There were any number of reasons why this might have occurred months before taper. Europe had fallen into re-recession and was struggling to escape despite Draghi’s promised efforts; the US improved from the near-recession in late 2012, but this, too, was a bit on the sluggish side at least outside of the employment numbers.

Maybe more than both, the invulnerability of the EM economies especially the Chinese was increasingly under suspicion. China’s economy had suffered in 2012, too, and it brought down with it prospects for “global growth” that up until early 2013 were supposed to have been ironclad.

In short, the post-2011 world was looking more and more like Bank of America’s balance sheet. People still today don’t appreciate the paradigm shift of 2011. If the eurodollar broke in August 2007, it was broken for good in the middle of 2011. No QE or policy promise was going to fix that; none has.

What happened in 2013 was a warning, a big one, about what was coming. It sure wasn’t recovery and happy days. Markets in the US did manage Reflation #2, but it was conspicuously brief and never made it past the last weeks of 2013. By early 2014, while Bernanke was handing off to Janet Yellen what he thought was the right baseline monetary tendencies for ultimate economic success, he had only been fooling himself yet again (for a man as intelligent as Bernanke, he clearly stopped learning at MIT in 1979 with his PhD).

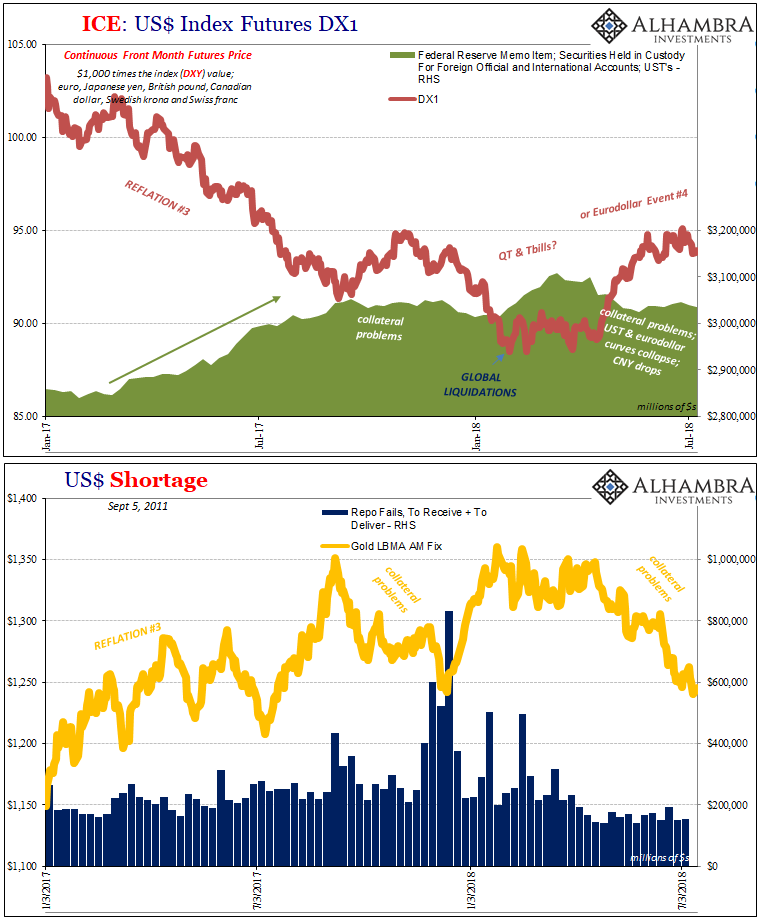

There was enough going on in the first half of 2014 that was too much like 2013. Gold never recovered despite “reflation”; the dollar didn’t much, either; the curves started to collapse as did CNY right at the outset of that year. By the time DXY flew upward, there really wasn’t much to be surprised about – unless you believed it was a taper tantrum.

The world was fooled into thinking that everything was fine and that all this other stuff that wasn’t fine in 2013 was just a rough patch to be easily smoothed over by the successful completion of a global recovery. As noted yesterday, they even handed out awards to Mario Draghi and the PBOC in January 2014 thinking that was the only possible end for so many bank reserves and “money printing.”

That’s what believing in the taper tantrum did to the world, leaving it blind, and wholly unprepared, for what was about to happen. Though the US economy was largely sheltered experiencing only a manufacturing recession and downturn in 2015-16, that was still a world away from what was supposed to have happened. For many parts of the world outside the US, in particular the EM’s, it has been a catastrophe from which most have yet to escape all these years later.

The renewed EM crisis in 2018 with all the same collateral components is as it was in 2013. It wasn’t Bernanke’s step-down then, and it isn’t QT or T-bills now. Both of those would have us believe of small, manageable problems we shouldn’t be overly concerned about because everything is about to get so good.

This is eurodollar stuff. Still. The results are never close to good.

Stay In Touch