Automobiles have come a long way in two decades. The import craze of this latest bout of globalization was in the car business handed an open door by a lack of quality, or perceptions about a lack of quality. The domestic auto industry in the seventies and eighties really did not shine its brightest.

By the nineties, near constant problems became a source of early internet amusement. One urban legend passed around chat rooms had Bill Gates trashing the auto industry at a computer conference, which then triggered, supposedly, a direct response from GM CEO Dick Wagoner. The story really grew out of an old joke:

There’s word in business circles that the computer industry likes to measure itself against the Big Three auto-makers. The comparison goes this way: If automotive technology had kept pace with Silicon Valley, motorists could buy a V-32 engine that goes 10,000 m.p.h. or a 30-pound car that gets 1,000 miles to the gallon — either one at a sticker price of less than $50. Detroit’s response: “OK. But who would want a car that crashes twice a day?”

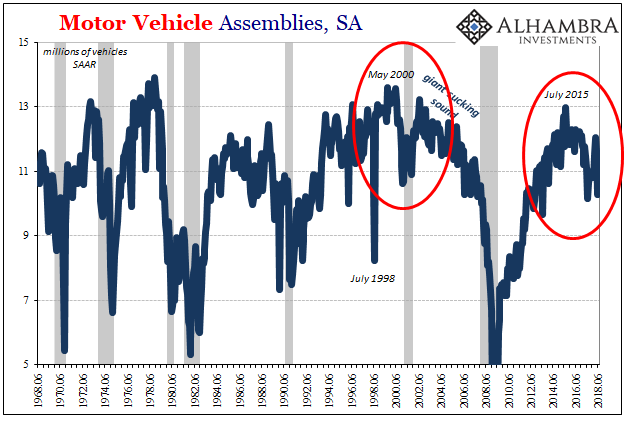

Both sides of it were simultaneously true; finicky computers then still in a stage of infancy and new cars that had a tendency toward recalls to fix unexpected issues. In July 1998, for one, General Motors was forced to recall almost 1 million vehicles over airbag sensitivities. Complaints to the National Highway Traffic Safety Administration alleged that in Pontiac Sunfires as well as Chevy’s Cavalier airbags would deploy under normal driving conditions.

The government’s investigation would ding not just GM, though. It would eventually involve Chryslers as well as “quality” imports like those from Subaru, Mazda, and Volvo. Needless to say, the model production changeover in July 1998 was particularly tricky. According to the Federal Reserve’s Industrial Production figures, domestic Motor Vehicle Assemblies (MVA) plummeted in that one month.

But that was only one month out of what was otherwise a very good decade for the domestic car business (including import brands who assembled cars in the US). All jokes aside, the nineties weren’t bad for automakers, foreign and domestic. Big problems in production are almost always instead the result of macro factors – customers being unable to buy new vehicles because many no longer have jobs, or, just as bad, customers being unwilling because they fear generally negative labor market prospects.

This is what makes the auto business of the past few years so interesting, or white knuckle if you work in it. By all accounts, production has behaved as if the US economy overall is in a mild but lengthy recession. It is comparable to the depth of the dot-com recession, but now has been extended to twice as long.

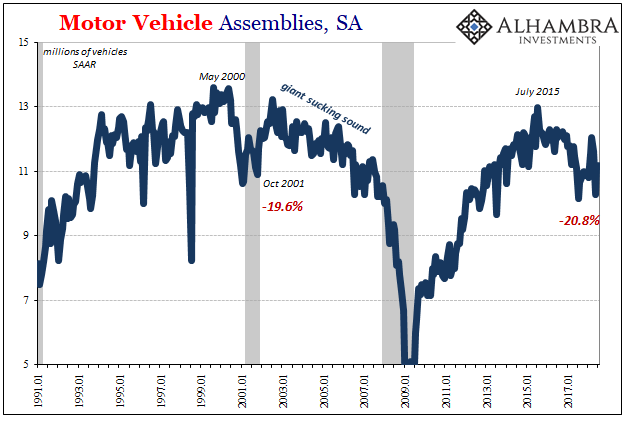

According to estimates released this week by the Federal Reserve inside its Industrial Production series, MVA’s continue to slump. At 11.18 million in July 2018, that is about the same as revised estimates for June. Compared to last July, and the last model changeover, MVA’s were up by 10% from what remains the low point so far. Is that a good sign for the business, that July this year is better than last year, or a bad one in that despite predictions as well as constant claims of a booming economy the overall slump in production reduced the need for further reductions?

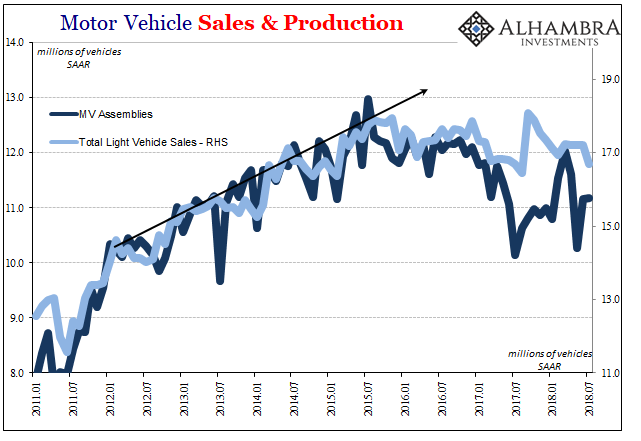

It’s easy to see why automakers are in production recession. Sales continue to be soft. They are classified otherwise in the mainstream, of course, where various media outlets will be quick to note how sales of ~17 million are good when compared to prior years. The charts, however, show something else – a clear and so far sustained inflection.

This is now three years of something. It is that background which draws our focus so far away from this presumed economic boom. The auto industry isn’t as important as it used to be, no question, but it is an economic bellwether nonetheless given the close relationship between slumps in production and those of the overall economy.

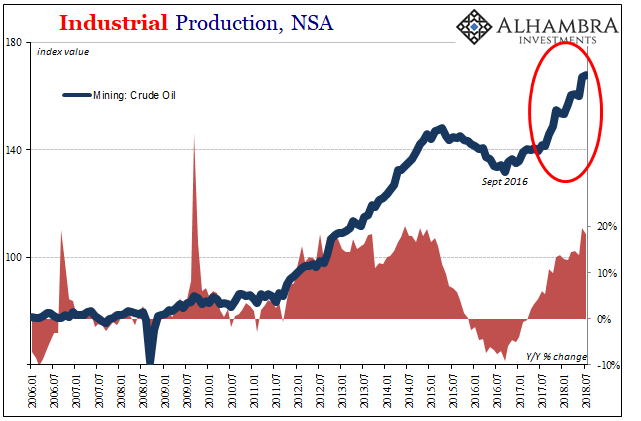

It leads us to the same limbo that has reduced US economic function, all global economic function, to little more than unusually small upturns interrupted by increasingly lengthy downturns. It never gets anywhere because when given the chance (eurodollar reflation) it can never really get going. This time around, since the last downturn in 2015-16, the auto business is a huge drag more than offsetting what is another record run in crude oil production.

As a political issue (energy independence) the shale boom is a huge win. As an economic factor, it isn’t nearly as compelling as light trucks and especially car sales. That might be an even bigger difference if the price of oil follows along with the dollar, which has already renewed its 2014 pattern. The mining sector didn’t fare well at all in 2015 and 2016 while autos hung in at least for a while.

That’s not a cheery thought as the dollar goes up again. While Economists will surely claim that King Dollar is a good sign, and that perhaps another oil price decline a consumer boost, it didn’t work out that way for the auto industry nor the global economy the last time around. This time, if there is a this time, autos would already be starting from a mild production recession. Thus, in what condition might the economy overall be starting from?

The letter “L” comes to mind.

Stay In Touch