If Brazilian central bankers are the standard for illicit shamelessness, their European counterparts are at least on the same spectrum. At the end of April, the European Central Bank’s President Mario Draghi took his shot at purposeful mischaracterization. Speaking to the press after the ECB’s Governing Council meeting had concluded, Draghi had been forced to concede there had been at the time, “a loss of momentum that is pretty broad based across countries and all sectors.”

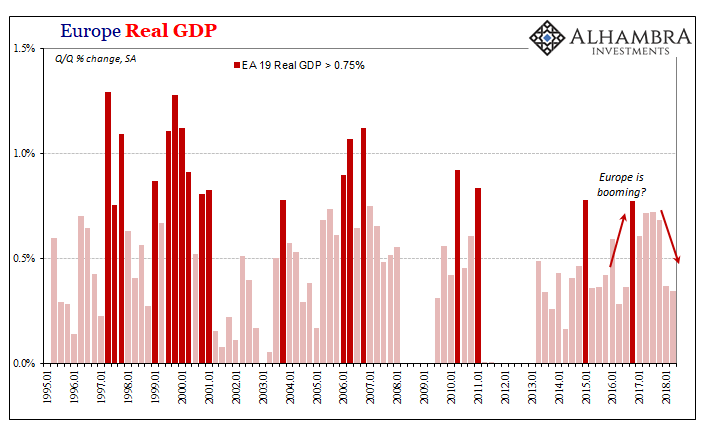

Eurostat would show that the size of the slowdown was pretty sizable. Real GDP growth in Q1 was cut in half from the prior few quarters ending 2017. That was OK, according to Draghi, because last year growth was, in his view, beyond excellent.

He would brazenly say as much three months later, even though the “moderating” economy had stubbornly persisted. Speaking to the press at the end of July following that Governing Council session, the ECB head, pardon me, spun his ass off:

Quarterly real GDP growth moderated to 0.4% in the first quarter of 2018, following growth of 0.7% in the previous three quarters. This easing reflects a pull-back from the very high levels of growth in 2017 and is related mainly to weaker impetus from previously very strong external trade, compounded by an increase in uncertainty and some temporary and supply-side factors at both the domestic and the global level. [emphasis added]

Playing to his home crowd, he knew the narrative about last year’s economic “boom” would go unquestioned. Therefore, if you think 2017 was some shade of awesome then a little slowdown in 2018 really wouldn’t be something to get worked up about.

If, on the contrary, you see how last year was at best minimal, then cutting growth in half starting from lackluster is a different animal. Eurostat reported that the slowdown had indeed carried on into Q2, with growth a touch less than even Q1.

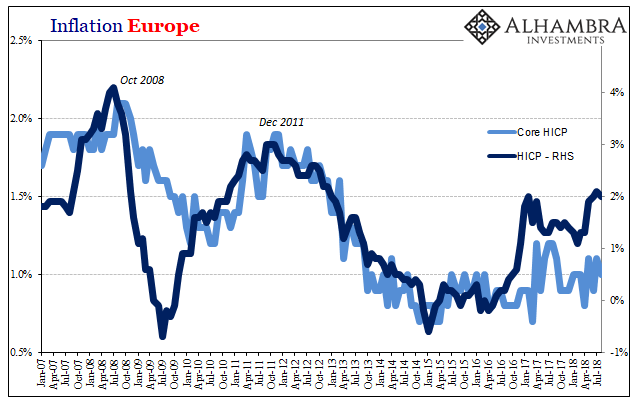

Despite this, the ECB remains undeterred with regard to its all-important inflation mandate. European consumer prices are rising at the required rate of 2%, according to Eurostat’s HICP calculations. In the latest flash update for August 2018, released today, consumer prices were up 2.0%. Though down slightly from 2.1% in July, that’s three straight months of headline obedience.

The core inflation rate, however, is another matter. It has very noticeably deviated from the headline over the last few years, leaving mostly oil but some food prices to explain the difference. Therefore, as even Mario Draghi acknowledged in July, unless the European economy actually picks up the inflation rate isn’t going to stay near 2% for very long.

On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows…Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

It is now August 2018 and the expected inflation acceleration (meaning, broad-based gains beyond commodities) is still being talked about in the future tense. He said the exact same thing last year. It leaves European officials stranded at a familiar crossroads. Hello 2011. It’s still coming, they say, but those nagging “transitory” slowdown deflation features are creeping back into the mix.

They have already crawled back in, requiring Draghi’s ridiculous July dance to try and downplay them. Central bankers keep promising what they cannot deliver; economic circumstances change for reasons that have nothing to do with central banks or any of their policies.

There is simply no monetary or economic basis for these more optimistic projections. It’s just not there. It was a long shot to end last year based on really uninspiring growth at that time. Draghi and parroting Economists tried to say that 2017 was just the first step, but more than halfway through 2018 with the euro heavily playing the flipside of dollar deflation they don’t even have that anymore.

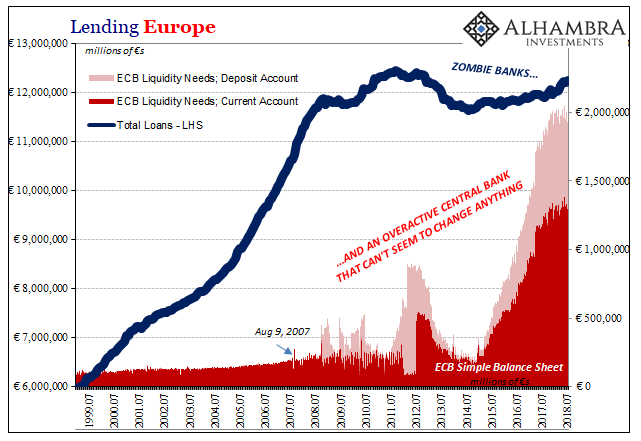

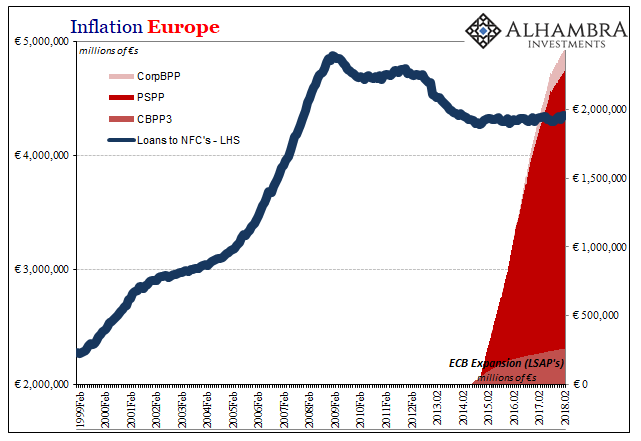

Instead, the ECB is forecasting based on things that “should be” but aren’t yet. Among those, as always, is loan growth. But lending has perpetually lagged no matter what the central bank does, and it has done a lot, meaning, again, there is no current basis to expect any pickup in economy, inflation, or really anything.

Lending is up nominally since 2014, with total loans outstanding rising by a total of €614.7 billion, a pitiful 5.3% (overall, not per year), in four years. Over those same four years the ECB has purchased, and still holds, €2.48 trillion in various securities. It’s not working.

In the four years between December 2004 and November 2008, inclusive, lending in Europe surged 42.3%, an increase of €3.5 trillion. The difference is obvious, and so are the reasons for that difference.

No big central bank operations were required during that earlier period. Central banks don’t print money, banks do by balance sheet expansion. When central banks are active, it is because banks are not. Everyone is taught that it’s the other way around, that monetary policies “stimulate” banking. Nope. Therefore, monetary policies of the QE or NIRP variety don’t actually help other than to signal to everyone that central bankers now realize something they don’t understand is wrong.

The history of the last decade is conclusive on the matter, having been established well enough in Europe alone but for good measure the lack of results has been replicated all over the world

On this basis we are supposed to believe everything magically goes back to normal? It really doesn’t take much to explain these flat and low yield curves almost everywhere. Long-dated bonds don’t need any absurd spin for their skepticism. They may be mispriced according to central bankers living still in the future tense, but here on Planet Earth in the present they present a remarkably accurate picture of reality.

Stay In Touch