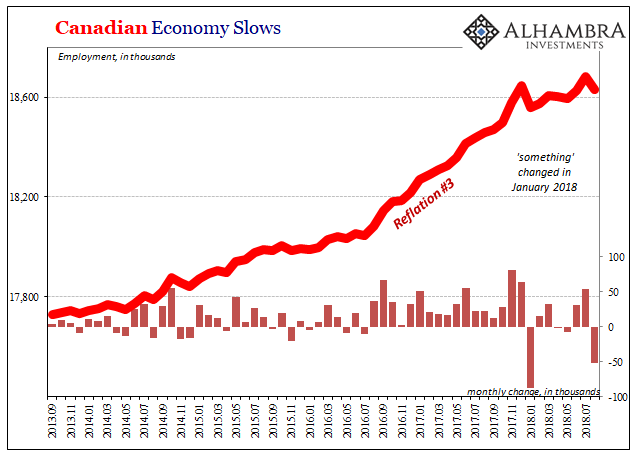

The ritual of Payroll Friday is not strictly a sorry American phenomenon. It is one shared by our neighbors to the north. The Canadian version, thanks to M. Simmons filling in the gaps of my limited experience with it, doesn’t typically sink into the depths of silliness to which its US cousin explores. At least not in as many months. This one, for August 2018, seems an exception.

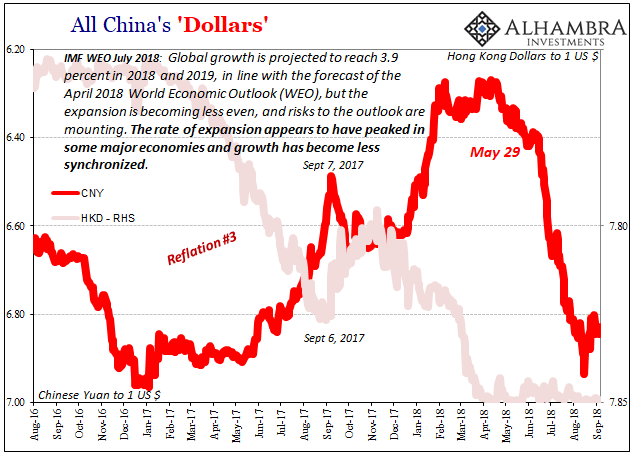

The main idea is simple enough – globally synchronized growth. In 2017, the argument was about the size of the positive numbers and whether having all major economies on the same side of the divide was meaningful. This year, especially heading into the back half of 2018, is turning out different. As in not so synchronized.

The data released Friday by Statistics Canada in Ottawa reversed strong employment gains made earlier this summer, including sharp increases in Ontario. But the overall picture is one of a labour market gearing down markedly from last year and an economy not at risk of overheating. That reinforces expectations the Bank of Canada will take a cautious approach to increasing borrowing costs.

Total payrolls fell rather sharply last month, according to today’s figures from StatCan. It’s not the first time this year, as job growth reversed even more intensely back in January. It was, however, the third month out of the last five to be shedding jobs. One month you can tolerate as noise. Half of the eight months so far posted?

One wonders why it took this particular report to make such a difference in terms of the “boom.” Below is the very same media outlet, Canada’s Financial Post, reporting on what was widely perceived as being the country’s economic situation. This earlier article reckoned the biggest risk facing Canada wasn’t trade wars or currency but overheating. It was an uncontroversial perspective.

The evidence of tightening is everywhere: the unemployment rate is sitting at four-decade lows; pay raises are picking up; and companies are reporting increasing number of job vacancies. Job listings show businesses giving thousands of dollars in signing bonuses to hairstylists and mechanics.

Here’s the punchline; the piece was published on August 29, a mere nine days ago. It sounds more than vaguely familiar, too, which is the point. Canada’s economy wasn’t any more robust or strong than the US version of this boom. The rhetoric about the global economy last year was way, way overdone, and some of it spilled over this far into 2018. And it will keep up this way until it can’t.

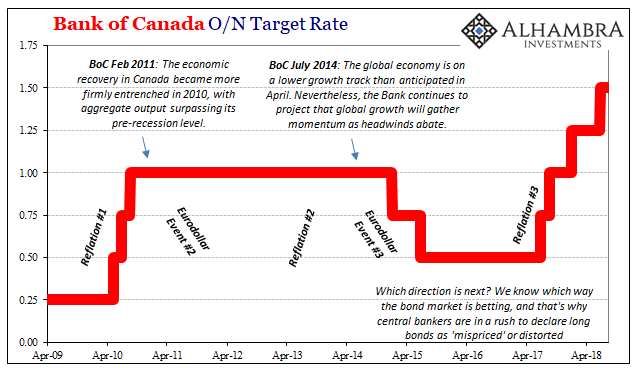

It was enough, obviously, for central bankers to sell their recovery. That was easier in 2017. It’s a much harder pitch in 2018 (just ask eurodollar futures). But that’s not really the extent of downside risks, though they will begin in that way.

In 2018 the dollar isn’t being so kind as it was last year. There is no Reflation #3 to provide some modest push to keep things at least nominally positive, not anymore. One by one, globally synchronized growth is coming apart, which only means it will be synchronized again in the not-distant-enough future; only with the return of minuses.

In truth, like Canada’s job market, there are always minuses even during the best of times. They become bigger and more frequent during these “unexpected” downturns. Unfortunately, the contours of renewed downswings are starting to appear in more places.

Economic growth in Canada is easy – just get the dollar, the Canadian dollar, to keep going up. Figuring out how to keep the eurodollar from doing the same thing, well, that’s the real trick. You keep getting the sense they really have no idea what they are doing, anywhere. They raise rates but have no idea why.

Stay In Touch