Payroll Friday continues to be among the more absurd rituals of the finance industry. That’s saying something because in this business there are many that in any other context would be laughed out of the discipline. Never mind the impropriety of attempting to use a single monthly yardstick for economic progress, over the last four years the payroll report has made itself irrelevant.

I made this point fairly regularly in 2015 and 2016. The payroll reports were still awesome by the standards of this “recovery” and yet it didn’t matter as the US economy grew weaker and weaker despite what everyone thought of them. People kept clinging to the Establishment Survey as if it was some magic shield against the “manufacturing recession.”

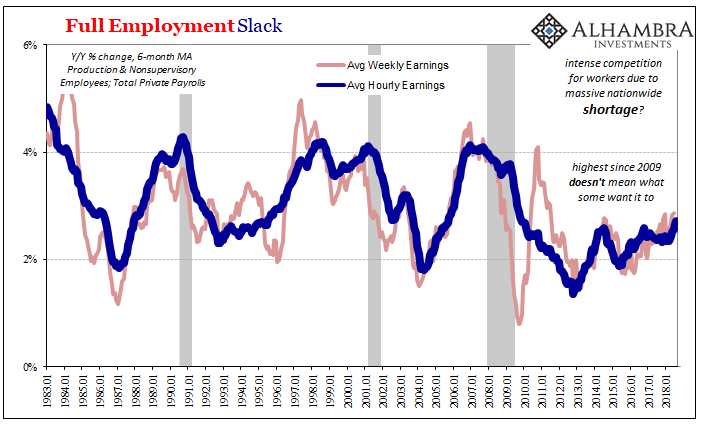

And those were the good ol’ days for the BLS. Today, it’s just the unemployment rate all by itself. At 4% and less for the fifth straight month in August 2018, it just has to add up to a booming economy; except the math doesn’t work. As noted yesterday for the nth time, there is just no evidence in wage and income growth that the labor market is even close to tight. The major media outlets are all yelling about some massive labor shortage but employers sure aren’t paying up for workers.

That’s why the comedy of this particularly irrelevant Payroll Friday. The average hourly wage rose in August by the most since 2009! That’s all it took, a headline out of context. The hourly rate increased by 2.9%, which was the highest, but barely more than in July or really any other time of the last set of years inclusive of payroll irrationality.

Given the headline and the knee-jerk market reaction to the “highest since 2009”, it’s really underwhelming, isn’t it? It reminds me of 2014-15 and the constant reminders of the “best jobs market in decades.” This is just wishful thinking, the desperate grasping for the unemployment rate to become real because that’s the only way this recovery can possibly be anything other than the same illusion.

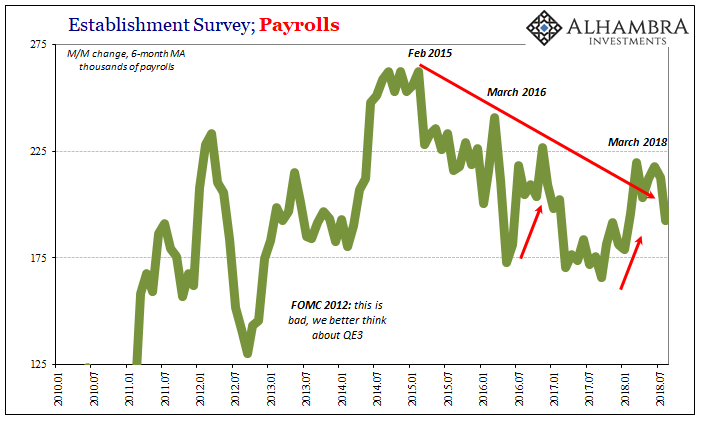

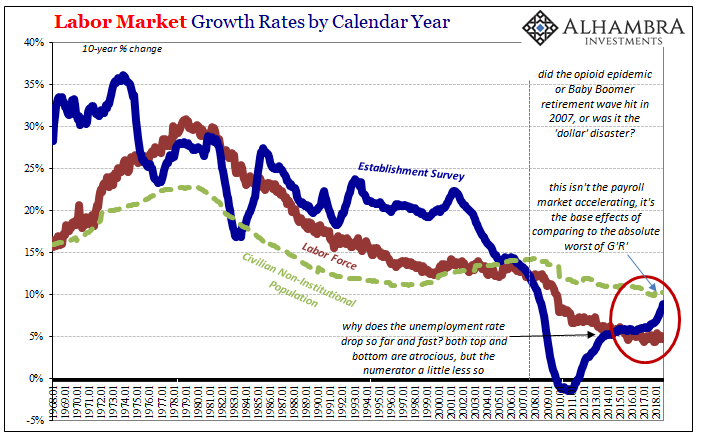

That’s the irony here, because outside of that one small uptick in the average wage, the rest of the payroll report was closer to awful. To begin with, +201k for the month of August is less than two-thirds of good. Not only that, the BLS revised payroll gains in the two prior months (June and July) by a combined -90k. The 6-month average for the Establishment Survey is below 200k again, suggesting the labor market may have cooled since the aftermath of last year’s storms.

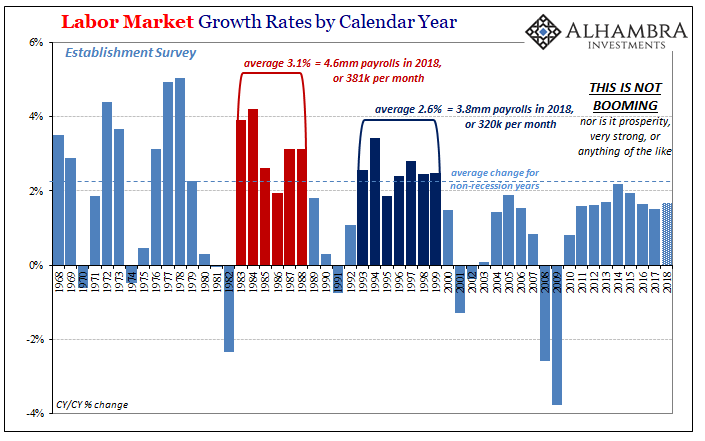

Employment growth in 2018 overall has been just barely more than in 2017. Last year, contrary to the rhetoric, was one of the worst in the labor market outside of recession. To be only slightly more than that should be alarming, especially eight months in with total payroll growth about the same as 2016 or 2012 (when the Fed panicked into QE3 and QE4).

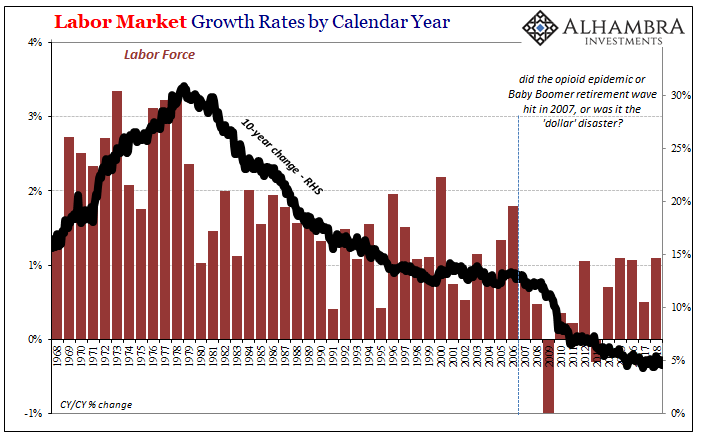

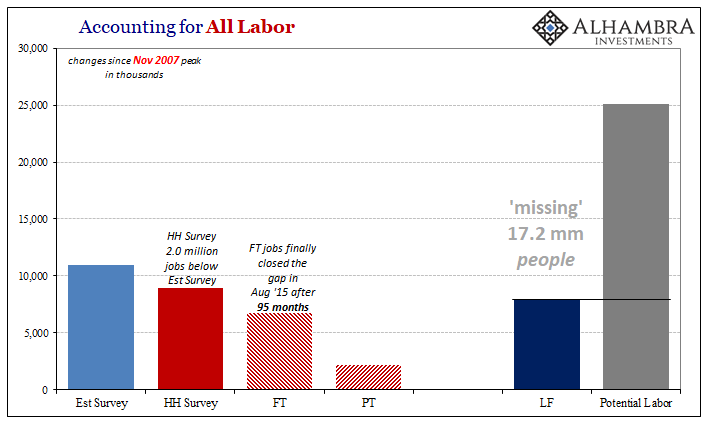

Even more concerning, the labor force is stagnating again. Month-to-month changes in it are noisy, but with a sharp decline in August the overall labor force was smaller last month than it was in February. Six months without an expansion leans toward significance, especially given the narrative about a labor shortage.

But that is the shortage, they will say. The labor force can’t grow to accommodate supposedly booming business demand for workers because all that’s left are drug addicts, the lazy unskilled, and aging Baby Boomers perfectly happy in their Florida condos.

This is why the wage rate is so important, because even at the highest since 2009 it still tells us that businesses are reluctant to pay up for workers. That can only mean Economists and the media have it all backward; the labor force isn’t stagnant because of opioids and the unwillingness to go back to school, rather the drug epidemic rages and Americans realize the futility of spending more for “education” because unlike Payroll Friday headlines they have to live with this very real absence of opportunity.

Without economic opportunity, it feeds those particular self-destructive tendencies as well as quite a few others.

This is why wages won’t accelerate. No matter what happens on the demand side, there is an almost endless supply of labor that can match employer needs. Companies aren’t paying up for new hires because they don’t have to (which in one sense is a good thing because they don’t want to, and in reality they actually can’t).

What happened over the last four years is the boom narrative switched partners. In 2014 and 2015, everyone was all over the Establishment Survey. The “best jobs market in decades” might have been technically true, but still nothing meaningful in proper context. Then the downturn happened anyway and the headlines began to show the damage from it.

So, everyone just ditched that for the unemployment rate. Neither of them have ever been confirmed by anything else, so Payroll Friday is further degraded to this sick custom. People and markets will be mesmerized by them in the short run, at least until all that dollar stuff makes them refocus to what actually does matter. Some months it doesn’t take very long.

Stay In Touch