Mario Draghi doesn’t have a whole lot going for him, but he is at least consistent – at times (yes, inconsistent consistency). Bloomberg helpfully reported yesterday how the ECB’s staff committee that produces the econometric projections has recommended the central bank’s Governing Council change the official outlook. Since last year, risks have been “balanced” in their collective opinion.

Given what’s happened this year, especially how different it’s been from what it was supposed to have been, the suggestion was for “downside” rather than “balanced” risks. This would be more like reality.

The Governing Council today for one of the few times rejected the advice. At its latest policy meeting, the ECB officially keeps its assessment as “balanced” economic risks. Good for them, it’s quite an emotional toll to surrender.

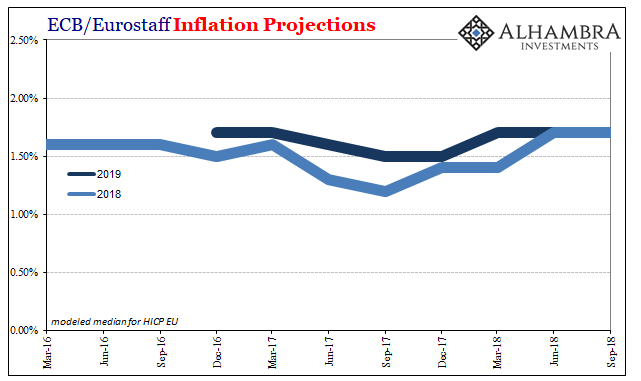

At the same time, however, their projections are beginning to roll over anyway. In terms of inflation (HICP), they no longer are projecting inflation to accelerate further. Since last September’s forecasts, the models had been riding the rise in oil prices to a situation closer to the central bank target. As of the current modeled runs, European inflation still won’t reach 2% anytime soon.

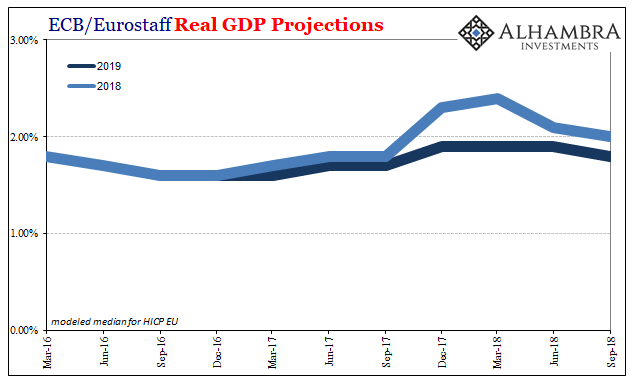

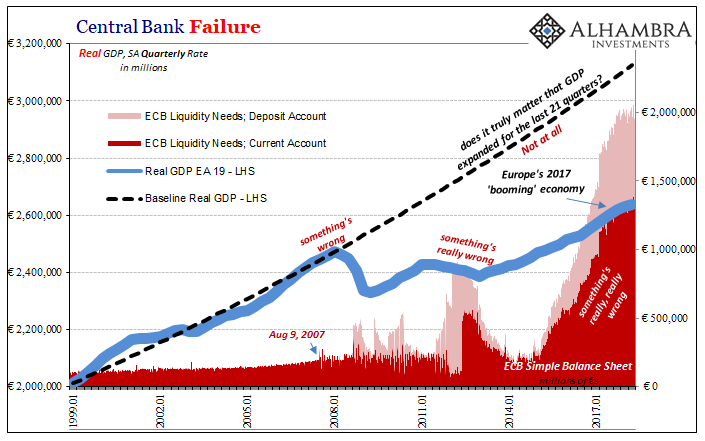

For economic growth (real GDP), the numbers are already starting to come down. For the second time in a row, the macro figures for 2018 have been reduced. Back in March, the ECB staff were seeing 2.4% in growth for this year, picking up on last year’s supposedly strong finish. They always extrapolate in straight lines, clearly unable to determine what it is that moves the global economy one way or another.

The September estimates have been pared back to 2.0%, and for the first time the 2019 estimates were lowered a touch. What happened in between March and September?

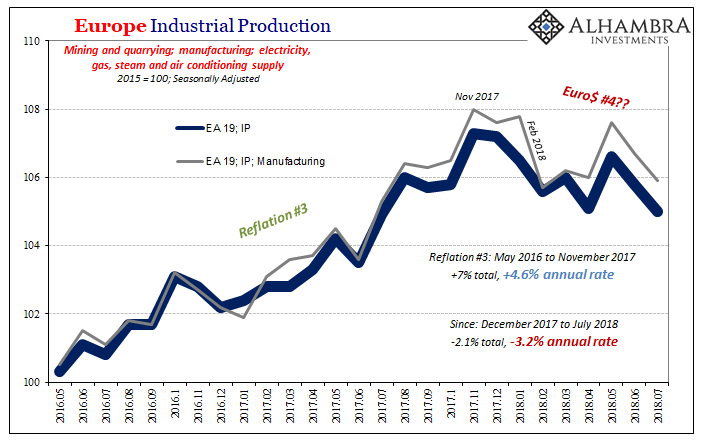

Nothing much, at least according to Mario Draghi. He’s clinging steadfast to the idea 2017 reflation somehow lives on. He didn’t say “transitory” but that’s just what he meant.

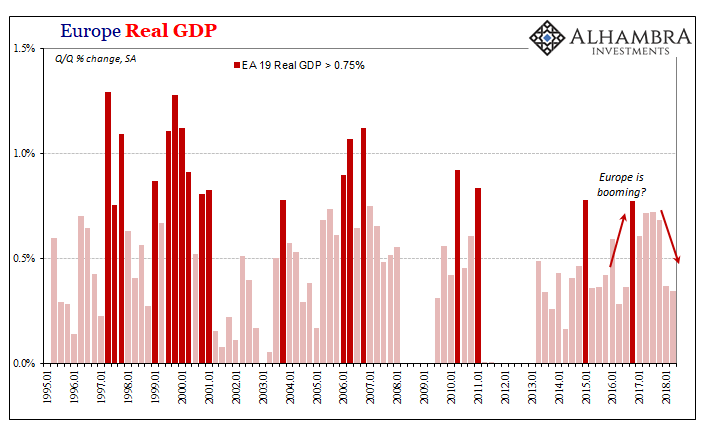

The underlying strength of the economy continues to support our confidence that the sustained convergence of inflation to our aim will proceed and will be maintained even after a gradual winding-down of our net asset purchases… Euro area real GDP increased by 0.4 per cent, quarter on quarter, in the second quarter of 2018, following growth at the same rate in the previous quarter. Despite some moderation following the strong growth performance in 2017, the latest economic indicators and survey results overall confirm ongoing broad-based growth of the euro area economy.

“Some moderation.”

But Draghi had to say something more about that past “moderation.” Quite consistently, he downplayed these downside risks that are somehow still balanced despite their clear indications in a broadening number of economic accounts and variables.

At the same time, uncertainties relating to rising protectionism, vulnerabilities in emerging markets and financial market volatility have gained more prominence recently.

“Gained more prominence.” Draghi is nothing if not entertaining. They all bought into globally synchronized growth because, if little else, they have to be exhausted after eleven years of one failure after another.

In Europe more than most other places, an actual recovery would have meant something. It would have validated, in part, QE and “non-standard” monetary policies; the very technocratic nature of the activist central bank. They really, really want this one.

As such, these Economists aren’t going to give it up so easily. They claim data dependence often, but that’s never been the case. Recall the ECB was “raising rates” in both 2008 and 2011, forecasting each time a lot more growth and inflation than they do now. In both instances, it was severe eurodollar crisis underneath the whole time.

But that was Jean-Claude Trichet’s ECB. Mario Draghi was supposed to be different. Instead, he’s proving pretty consistent.

Stay In Touch