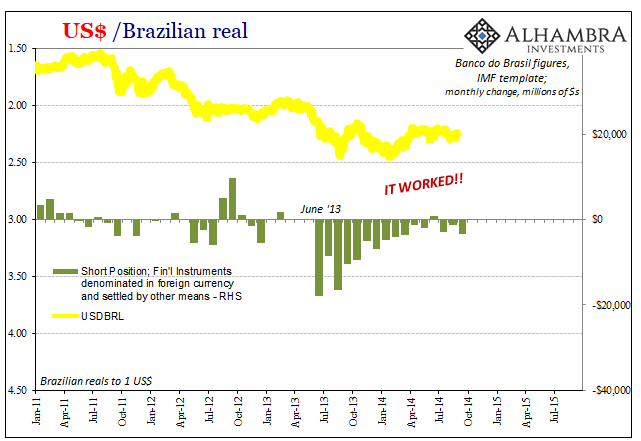

On June 10, 2013, Brazil’s central bank announced an allotment of 40,000 currency swap contracts at auction. This was the second operation carried out in short order that month, following weakness in the real, Brazil’s currency (BRL), against the dollar. In order to forestall any further declines, central bank intervention has long been a frontline tool in EM arsenals.

But why swaps? After all, Brazil as many others in the same situation had spent about two decades amassing huge stockpiles of reserves. That was the key lesson they took from the 1997-98 Asian flu debacle. In this modern world of massive global flows, central banks would have to become equally massive.

This is why I refer often the pound crisis of 1992, particularly that one New York Times article and its apt description of what was an unappreciated monumental change:

The world’s currency markets, it seems, are no longer governed by central bankers in Washington and Bonn, but by traders and investors in Tokyo, London and New York, as the chaos in the currency markets this past week has shown.

It was an interesting footnote to the UK’s struggles earlier in that decade, but after Asia was wiped out later on in the same one the world began to play catch up. That was the thing about the 2008 panic – it showed that they never really did catch up to the global system, only that they thought they had.

The EM’s quick recovery from the global Great “Recession” furthered that illusion. When the 2011 crisis struck, a second in the eurodollar system, they were just as unprepared by underestimating the severity, discounting its global reach, and more than anything failing to realize the chronic nature of the monetary reverse.

The problem with mobilizing reserves is domestic money supply. This is not a new phenomenon, and the links between dollar flows, now “dollar” flows”, and local money well-established. Using anyone’s reserves, selling UST’s, if you will, transfers the external funding shortage onto the domestic economy (just ask the Chinese).

A currency swap is a way to circumvent the full range of consequences when confronting an external pressure. At least that’s what these central bankers think. Here’s Banco Central do Brasil stating (in the form of a working paper study) in July 2013 its rationale for swaps over reserves:

A well known advantage of issuing such contingent liabilities as currency swaps is that authorities become able to intervene in the exchange market indirectly, without affecting the money supply or varying the stock of foreign exchange reserves.

You can manipulate the currency at the same time keeping forex reserves in reserve. “In other words, to some extent, the large holdings of international reserves provided an insurance, as well as the means to fight eventual adverse movements for the Central Bank.” Swaps move the currency in the direction desired while the stockpiles of mostly US$ assets sit menacingly warning any speculators who might challenge the central bank of its ultimate resolve.

But this only means something if the swaps are effective. The point of Banco’s July 2013 study, and no doubt the timing of its publication, was to assure markets and anyone else paying attention that, yes, these swaps had been quite successful even as recently as 2012.

We posited that, even though these contracts do not directly affect the supply of foreign currency in the market, they are likely to affect exchange rates as they alter the demand for foreign exchange – particularly if traders extrapolate exchange rate trends at short-term horizons

It’s not just traders who are extrapolating, though, is it? These central bankers are doing just that themselves. They deliver these swaps, and often they are not swaps as you may know them, and simply expect that they work; and that markets agree with that assessment beforehand.

The real kept falling throughout June 2013, and by the end of that one month the 40,000 allotment auctions were being fully subscribed. The situation was becoming more dangerous than they originally believed, which is why the July study came out in addition to a steady diet of more swaps over the next several months – with “selling UST’s” left still in reserve.

But there is a key difference that central bankers don’t appear able to grasp. In the Brazilian form, what Banco actually does is subsidize further dollar borrowing by banks in its own jurisdiction. In truth, that’s all any central bank does by deploying swaps. The mechanics are often dissimilar, sometimes, like Brazil, almost bizarrely so, but the general format is the same.

Central banks by refraining from offering actual money in any form, dollars or otherwise, use derivatives to artificially cheapen the price of borrowing in eurodollar markets as it becomes expensive. These offers say nothing about why it has become expensive to borrow on eurodollar markets. In truth, central bankers just don’t care.

They simply believe that by doing something the problem will resolve of its own. They never conceive how by subsidizing an expensive task they would have made that task even more expensive if the problem isn’t solved. If you have a $100 funding requirement at, say, 3% (these numbers are for illustrative purposes, not the exact way in which things actually work; it’s much, much more complicated) that suddenly becomes 5%, Banco offering to cut that rate back to 3.50% only helps if at the end of the subsidy the market funding rate goes back to 3%.

It can become even more oppressive if banks are lured further in, as they often are by swaps. What I mean is, Banco subsidized the funding rate all the way to 2.5% or 2%. In that case, extrapolating central bank success, you might borrow $150 rather than $100 (offering the surplus $50 to others, at mid-spread, as is intended by the policy).

Except, now when the subsidy matures you owe $150. If the eurodollar market goes back to 3% normal, no big deal. What if it doesn’t? What if non-subsidized funding costs are now 6%, or worse? Everyone runs for the exits all at once and central bankers stare in dazed confusion over what the hell just happened.

For Banco, it got away with it for nearly seven months thinking everything had stabilized. In early February 2014, the real was back toward the August 2013 lows again, but then steady for the spring and summer (or, in South America, fall and winter). By June 2014, they were paring back their eurodollar subsidies (swaps) believing of nothing but complete success.

While they were doing this, Brazil’s economy had already suffered the first effects of 2013’s monetary wrath. Not only that, China’s currency, CNY, had begun to destabilize in the same way as Brazil’s had only months earlier. The symptoms were very nearly the same. There were other warning signs that eurodollar funding was not going back to 3%, as in our stylized example, but was in those particular months skyrocketing.

In the Economics textbook, those things don’t matter because central bankers are presumed hold total dominion over their local systems. Any economic fallout was expected to be transitory, easily managed as the real stabilized through the rest of 2014.

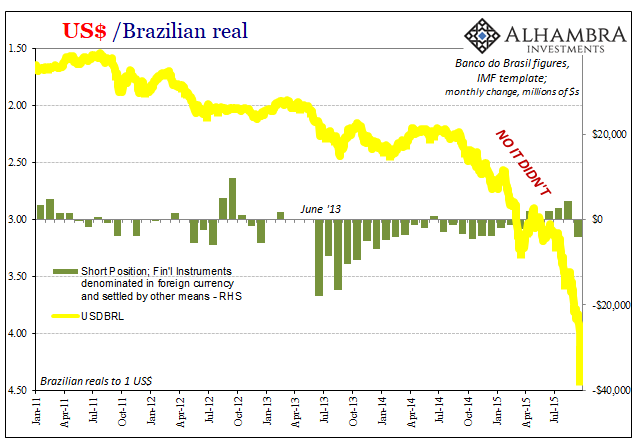

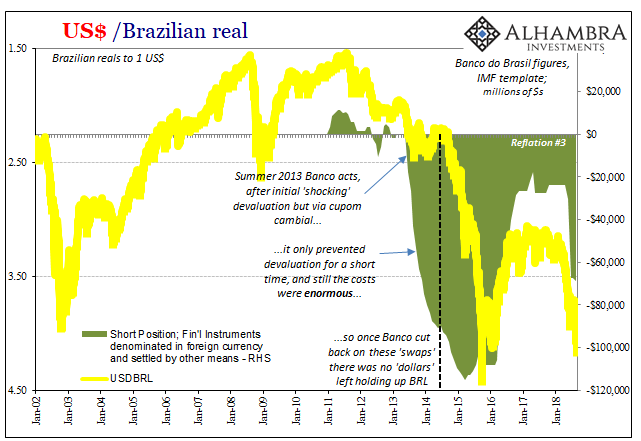

By that September, Banco had extrapolated itself to the precipice of complete catastrophe.

This was the farce of early June 2018. Faced with the exact same eurodollar situation, Banco put on a ridiculous circus. They would easily manage BRL with swaps and reserves, they said, as if the July 2013 study wasn’t somehow superseded by a mountain of global evidence in every possible form.

The interesting thing about markets, however, is they don’t often extrapolate in the way Economic theories expect. The “don’t fight the Fed” mentality that all central banks depend upon in one shape or another is persistently eroded by these eurodollar episodes.

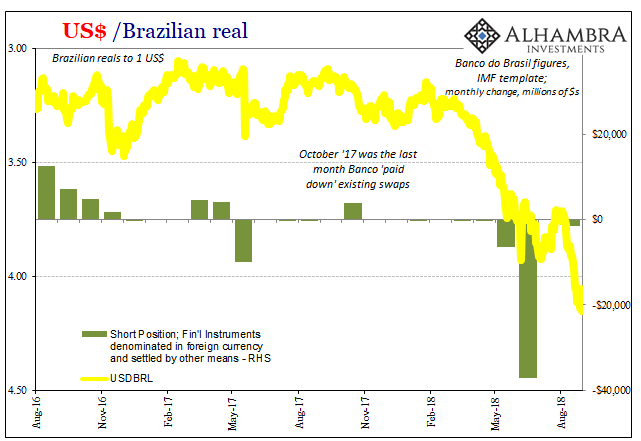

In Brazil 2018, Banco again made its display of force in the form of swaps. In June, they did more in that one month than in any two months during the 2013-15 episode. Unlike 2013, the real declined sharply in the aftermath, especially during August. According to Banco’s latest update, the central bank offered just $1.5 billion in swaps during that month compared to the $37 billion allotted during June. No steady diet this time, it appears.

Have the central bankers caught on to how markets have caught on?

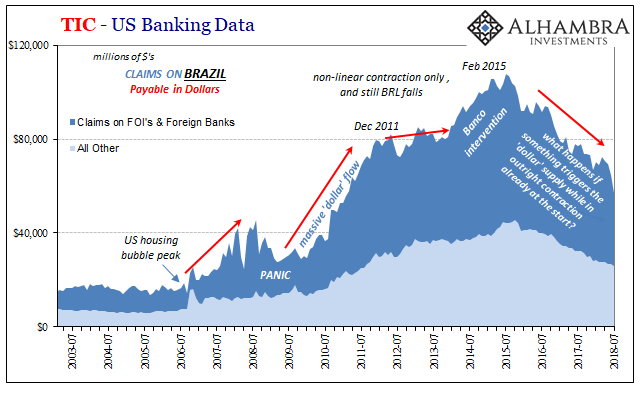

The TIC estimates for July 2018 suggest a rather large drop in cross border bank claims (in dollars). This, too, is unlike 2013. In other words, Banco was subsidizing eurodollar funding in June but in the following month it doesn’t appear to have been close to enough of a cost subvention.

That would leave Banco with two increasingly unappealing options. The first is, as they have in July and August, to largely do nothing; to hope that the FOMC is right about T-bills and the painful indigestion merely passes on its own. This isn’t all that different from using swaps, both are aimed at the same temporal goal of just buying time until the external imbalance clears up by itself.

Before August 2007, this wasn’t an unreasonable inference outside of 1997-98. EM central banks had been intervening for years. Small interventions for small problems. It’s these big interventions for big problems that the theory breaks down so disastrously; not that either is big but that they don’t understand the difference in what turns small problems into big ones, therefore small interventions into impossible tasks.

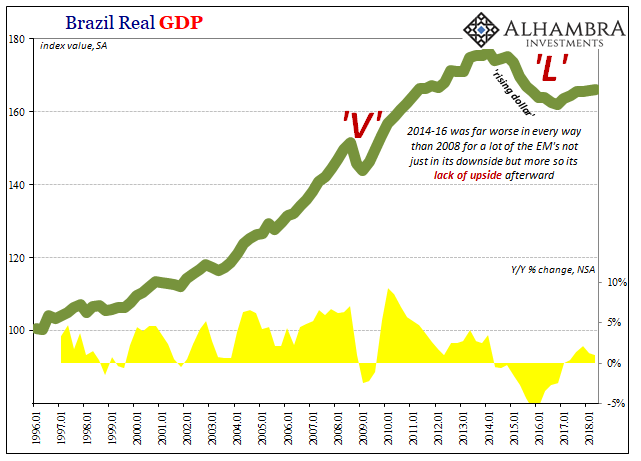

The second option is to use their “insurance.” Brazil hasn’t yet over the last five years despite what has been 19th century-style depression. Others, however, have, including the Chinese who had collected the largest stockpile of reserves any human could have ever conceived. It didn’t matter that they had them, and it further didn’t matter that they used them (nor the staggering extent to which they had). CNY dropped anyway, China’s economy absorbing the damage (its own “L”).

This doesn’t mean that Banco won’t take that next step. In reality, the one BRL points toward, they don’t really have a choice. Whatever happens now, it’s out of the central bank’s hands though they might be the last to figure that out. The TIC data suggests banks may have. That 1992 New York Times article was right about 1992 as well as 2013 and 2018.

Instead of spending decades building worthless stockpiles of reserves, central bankers would’ve been better off having used all that time rewriting the Economics textbook’s monetary chapters. They still can. But, as 2013-15 showed, they probably aren’t going to no matter what.

Stay In Touch