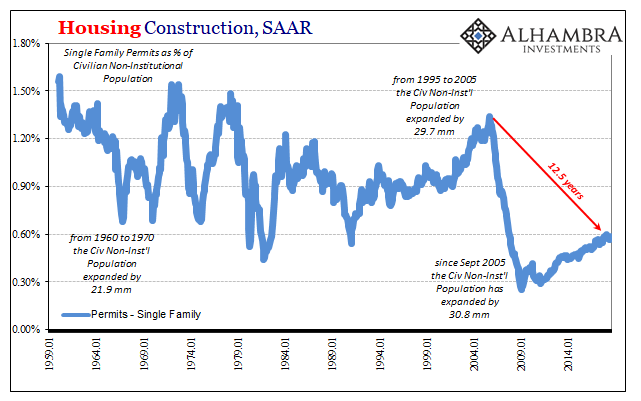

Back in March, the Kansas City branch of the Federal Reserve stated the obvious. US home construction was stuck near the lowest level in the 60 years of records being kept. Despite a decade having passed since the prior bust turned to boom, and with the economy booming, it was apparently worth mentioning.

Obviously, it wasn’t obvious to everyone since the published report was picked up across the US media incredulous to its findings. The Wall Street Journal went so far as to call it this country’s next housing crisis.

America is facing a new housing crisis. A decade after an epic construction binge, fewer homes are being built per household than at almost any time in U.S. history.

That’s the thing about economic depression. In recession, it passes and barely anyone notices once it’s gone. The dot-com instance was so mild, for example, most still associate it with September 11 though it began months beforehand.

Experiencing a prolonged macro event tends to change peoples’ behaviors for them. The generation that made the twenties roar is the same one that became so fiscally frugal to the point of extremes after the thirties. With very good reason. Some people are forced to appreciate these extremes.

Among the most prominent of those is liquidity risk. This works both ways. For businesses, they become reluctant to take on new liabilities (this labor shortage companies don’t seem too willing to do much about). For consumers, they aren’t so cavalier about life altering decisions as they once were.

In terms of housing, these are pretty simple. Where flipping homes fifteen years ago had become a fun game of who can oversize the most, over the last ten years people now prize financial stability. That starts with their view of the labor market, which may, in fact, be very different from how it is described every day in the Wall Street Journal (and its near constant anecdotes in lieu of actual data about this labor shortage).

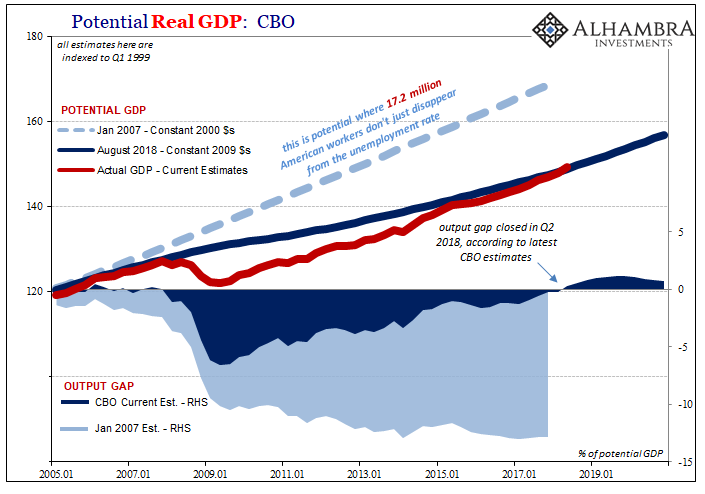

A very few Economists get it:

“Americans are essentially staying put in their homes for the foreseeable future, either by choice, or by necessity or some combination,” said Bankrate.com senior economic analyst Mark Hamrick in a press release.

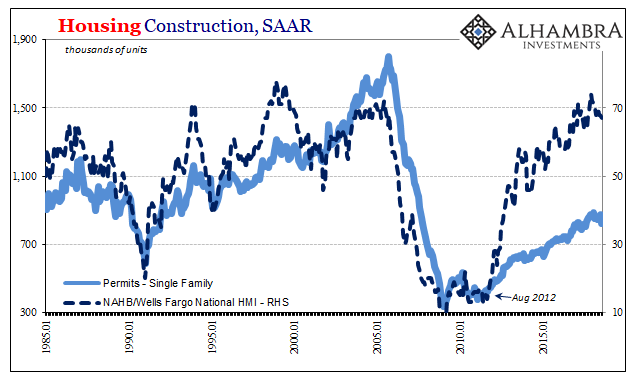

This restrictive supply of available homes should be causing an enormous boom in construction – if the Wall Street Journal is right about this housing “crisis.” It’s not, as the paper conceded in March. Builders are sky high in sentiment but clearly reluctant in action.

Just as workers have altered their home selling behavior, builders have, too, faced substantial changes to their habits. Among them, construction finance once at the top of any local bank’s list of lending projects is no longer.

And builders themselves, many who barely survived, cognizant of the surprisingly large number who didn’t, aren’t so willing to take on funding risks no matter what the unemployment rate says about prospective demand. The NAHB sported 240,000 members at the peak in 2007, a membership that had collapsed to 140,000 by 2012. Many were good businesses that just couldn’t manage the reverse of monetary leverage. They aren’t building for it until they actually see it this time.

Homebuilder sentiment is therefore something altogether different on this side of the bust, during this ongoing depression. They are happy not about their upside but as far as they can tell, being careful about leverage and funding risk, there isn’t an imminent risk of downside. They learned some very hard lessons and appear to be sticking to them – so long as the economy and the financial system remain as they are.

That last point is really the major one, though it gets buried in the noise of everything else. Things are generally positive, but generally positive isn’t a recovery. The real estate market is growing, but it isn’t really growing. That’s all the Kansas City Fed’s “study” found. Given that the report was written by central bankers belonging to a bureaucracy whose job it was to ensure a recovery, it isn’t surprising that they are surprised to find housing never recovered.

More recent housing data isn’t encouraging, either. The lower the unemployment rate goes, the main emphasis of this “boom”, the worse the housing market becomes; not because one follows inversely the other, rather because the unemployment doesn’t reflect on-the-ground reality of the full economy.

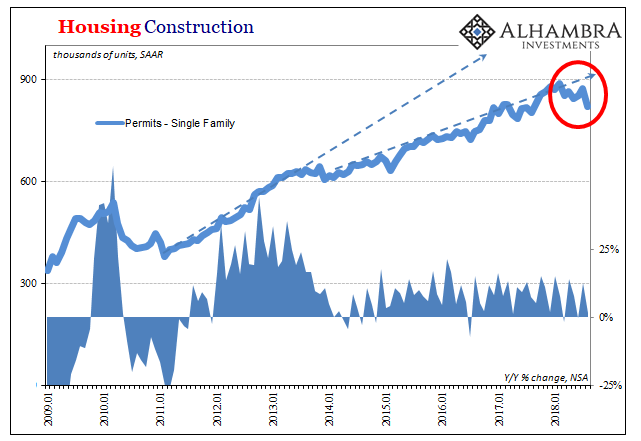

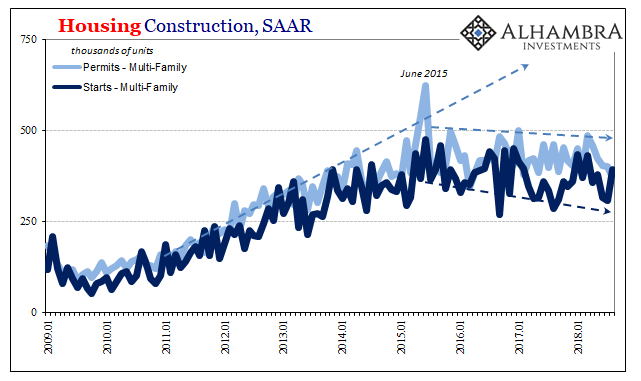

Apartment construction has been stagnant at best for one month more than three years now. At the same time, single family construction has hardly been robust – so much so that the Wall Street Journal characterizes it as a crisis of undersupply.

Now in 2018, there are signs of weakening in that segment. Since January, permits have fallen substantially. Month to month, the housing construction figures tend to be very volatile. This is a seven-month string, a multi-month slump emerging that raises the significance.

It puts central bankers in the US in a terrific bind. Nothing about housing makes sense in the context of full recovery, this economy currently booming for it. Take away that view, there aren’t any mysteries. Nor is it new(s). Changing the definition for recovery doesn’t actually turn the Great “Recession” back into recession.

Stay In Touch