The US is going it alone. The rest of the world isn’t so synchronized like it was, purportedly, in 2017. No matter, at least for Americans. Even Europe, last year’s poster boy for what this upswing was going to accomplish, has thoroughly disappointed. The United States is just going to have to leave everyone else behind with no regrets.

The Eurozone, Japan and select emerging markets all seem to be struggling economically with low inflation levels, poor policy responses, and low demand. Meanwhile, the U.S. keeps posting surprisingly strong economic numbers.

Consumer confidence, manufacturing momentum and services strength have converged into an economic growth rate well above 3 percent for the past six months, defying the gravity that seemingly grounds everyone else.

The above wasn’t written recently, however, though it could easily pass for current commentary. It speaks to us from out of time, penned in December of 2014. The theme of US “decoupling” was very strong then, too. Even the manic upward slope of the dollar was, for a while, readily embraced as a good thing.

The team of economists at Cornerstone Macro, led by veteran Nancy Lazar, notes that the U.S. consumer is actively benefiting from the turmoil happening in Asia and Europe.

While for some, especially Economists, they never learn, mostly it’s just the tantalizing idea that this time will be different. OK, 2015 sure didn’t turn out the way anyone wanted and decoupling was an incorrect explanation for differences in timing, but 2018 isn’t 2015. They may share the same direction for the dollar, but tax cuts baby!

The funny thing about them is that in early 2015, during the last decoupling hysteria, the oil crash was being talked about in the same way. In May of that year, Janet Yellen explained to Rhode Islanders the good parts of that rising dollar:

In addition, the drop in oil prices amounts to a sizable boost in household purchasing power. The annual savings in gasoline costs has been estimated at about $700 per household, on average, and savings on heating costs–especially here in the Northeast, where it was so cold this winter–are also large.

Like 2008, in a matter of months her careful optimism was far surpassed by all the things that weren’t supposed to be possible. Rather than starting to “raise rates” in June 2015 and go forward at a regular pace from there, as decoupling would have demanded, the FOMC instead would wait until December 2015 and then undertake only the one all the way through November 2016.

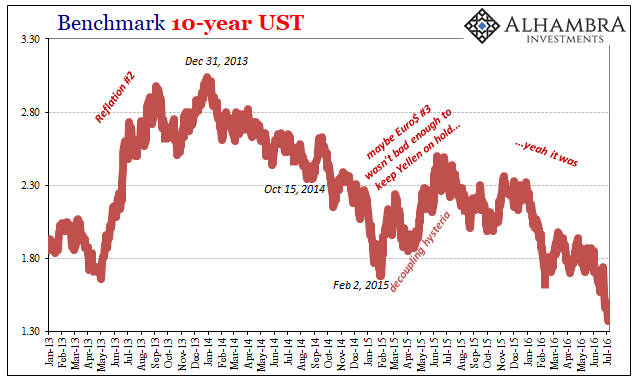

With the latest BOND ROUT!!! back in the front pages for the first time since mid-May, US economic strength in the face of renewed “overseas turmoil” is rhetorically a safe bet again. But that only raises further questions, the same ones that were brought up in early 2015 after what was then far more evidence for economic strength than there is today. It didn’t matter four years ago, why does it now?

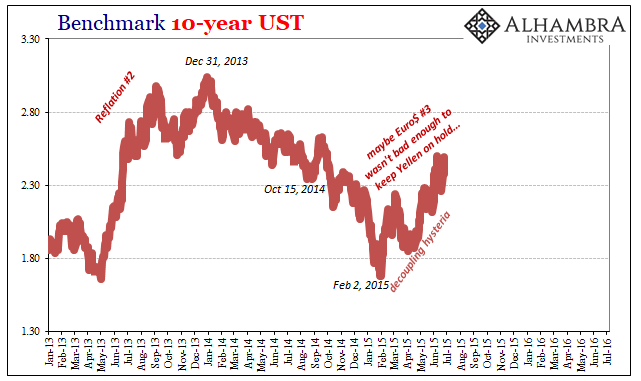

Nominal yields in the UST market had fallen all throughout 2014 since peaking in late 2013. These “unexpected” declines were more pronounced in October 2014 as well as that December – just as US growth seemed to be reaching its fevered pitch. GDP was thought to be 5% for two quarters in a row while the labor reports reported the “best jobs market in decades.”

From February to June 2015, yields retraced the vast majority of their prior decline. If the decline of long interest rates was concern about “overseas turmoil”, then the BOND ROUT!!! of 2015 seemed consistent with decoupling.

That didn’t mean, though, that bond investors (banks) agreed with the thesis. As yield curves compressed and collapsed then as now, what it suggested was that after that first phase of what would become eurodollar event #3, it hadn’t yet become bad enough in the US. Unless it would, Janet Yellen could go forward with her plans for “rate hikes”, one key risk to bond holders.

It would have to become far more serious than it already had been to put the Fed on hold. Which, of course, is exactly what happened, stunned as Yellen was to this more universal downward pull.

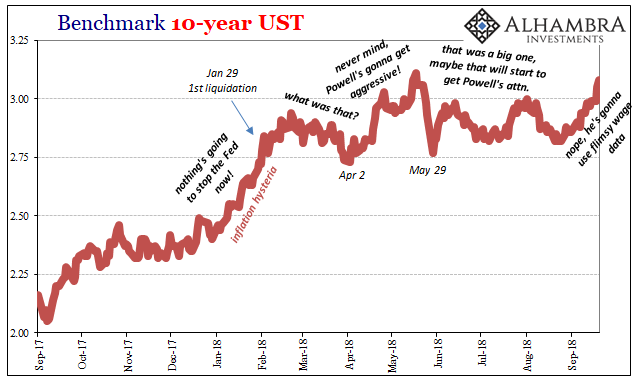

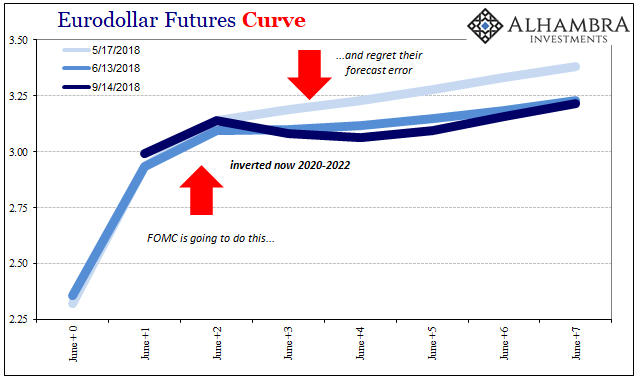

You can see the very same processes playing out in the bond market all across 2018 so far. This back and forth between Powell’s Fed being able to go as he likes, and these other times when his view is challenged – by “something.”

More than that, like 2014-15, it is those points of inflection that draw our close attention. Inflation hysteria was in full glide – until February 2. Global liquidations. Nominal yields stopped rising, started moving slightly lower and kept at it for several months after. What was in late 2017 clear sailing suddenly became “what just happened?”

By April, even though the EM crisis had by then been triggered, the BOND ROUT!!! got going again anyway – until May 17. Following the big dislocation (collateral) up to May 29, nominal yields shifted lower for several months after.

The only reason nominal yields haven’t fallen further following these monetary disruptions is the upward pressure from short-term yields – the same conundrum as 2004-06 – that was lacking in 2014-16.

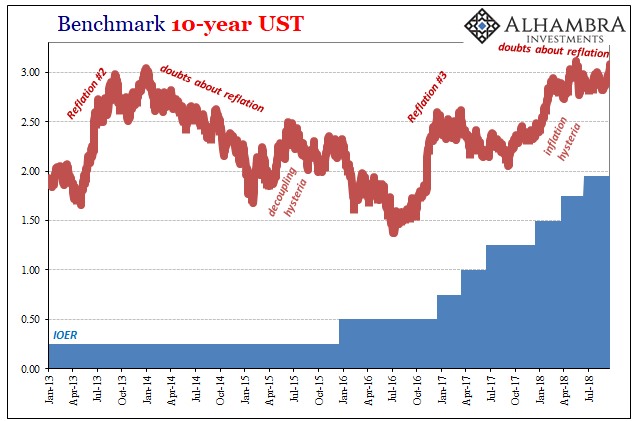

Thus, 2018 decoupling really hasn’t been any different than 2015’s. The key is timing, in that eurodollar event #3 impacted overseas locations many months and even a year before spreading inward to produce a near-recession in the US. The bond market vacillated between whether or not Fed officials could get away with ignoring it – the relative calm of early 2015 the last time in that particular mini-cycle bonds would trade this way.

It’s difficult to judge just how far it will have to go before irrational bureaucrats have their minds changed for them. For that, these minor selloffs that are shouted out as BOND ROUTS!!!

In the end, it didn’t matter because there is no decoupling. If the global economic system is rolling over, which is the whole point behind decoupling, eventually it will come for everyone. That’s the yield curve’s lack of slope, or the eurodollar curve’s very interesting shape.

Stay In Touch