Too much debt. Deleveraging. The debate over the “right” size of the credit market isn’t going to be solved. Like it or not, the US and world economy has been propelled by debt for a century. The domestic credit market’s highest growth rates are found not during the housing bubble of the 2000’s but during and after the Great Inflation of the seventies/eighties.

Misconceptions abound, mostly because Economists have been off studying exclusively mathematics all this time rather than economies and the money makes them go. One of the most striking aspects of this modern system is how the line between money and credit has blurred; a lot of what might be counted strictly as debt is at the same a monetary instrument (collateral in repo, as one example).

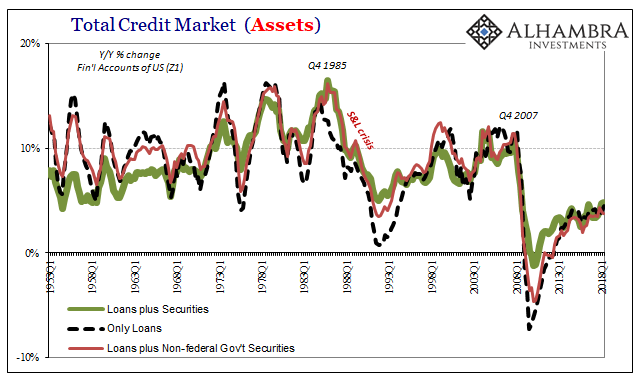

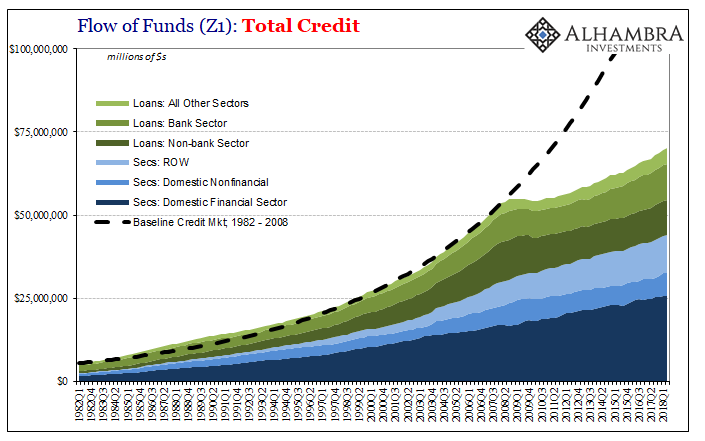

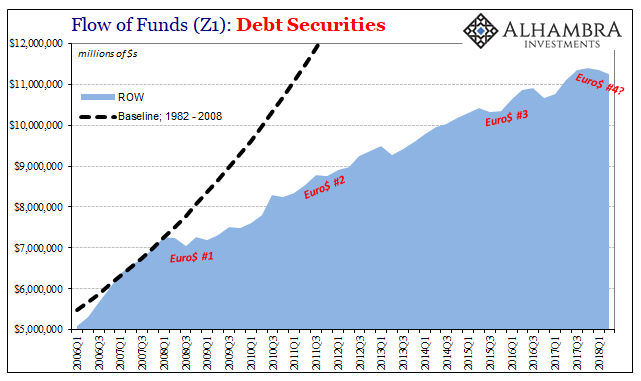

The Federal Reserve’s Financial Accounts of the United States (Z1) updated for Q2 2018 show that nothing has changed. Booming economy or not, the credit market still isn’t in it. It continues to grow, as do many important variables, but like a lot of them it isn’t the same thing as growth.

Believe it or not, the peak rate for credit growth came in Q4 1985 not the top in Q4 2007; though those two particular peaks do share a lot in common. What followed both were banking dislocations that greatly altered the way in which the system would work, or wouldn’t work.

After 1985, the S&L crisis ended up transforming the banking system from depository to wholesale, leaving the commercial bank side of things to push the eurodollar system to its fullest. That meant outside as well as inside the US.

After 2007, everything has just been shut down. Nothing has mattered which might get it restarted again.

Just as the Kansas City Fed noticed in March that housing never recovered from the last bust, the financial system didn’t, either. The two things are very much related, not that any central bankers would identify this latter half of the problem. Even though Z1 is a Federal Reserve series, it isn’t apparent that officials actually use it.

Ben Bernanke, of all people, actually said it best in 2009.

If there is one message that I’d like to leave you with, if we’re going to have a strong recovery, it has got to be on the back of a stabilization of the financial system.

You might then ask, what had he, and his successors, been doing all this time? The combination of Quantitative Easing and ZIRP was aimed in part at consumers and businesses in the form of inflation expectations. But mostly QE was supposed to spur banking and bring about the full recovery of the financial system.

Not only was it a massive increase in bank reserves, one lethargic form of risk-free asset, these kinds of LSAP’s were intended to create portfolio effects. The central bank bought securities from banks with the idea that the banks would then have to lend or at least buy additional securities.

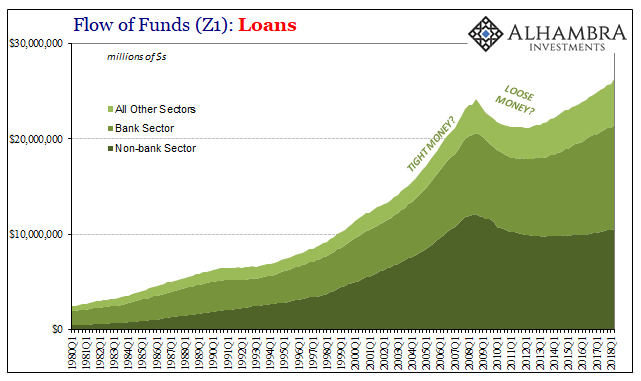

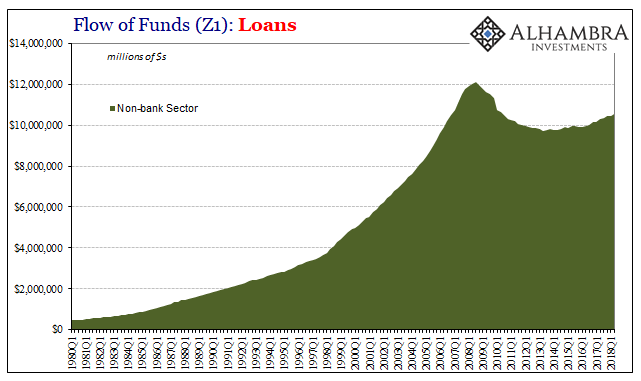

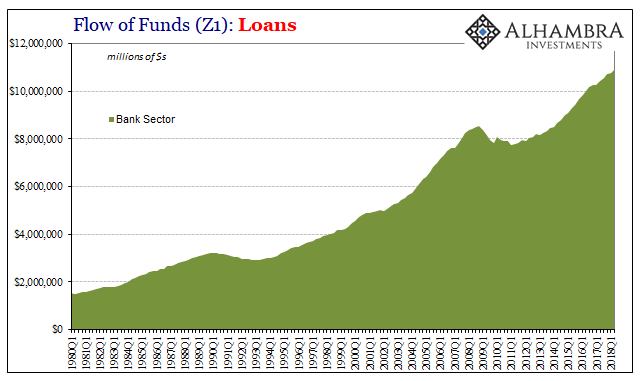

It didn’t really happen, not in the way it was meant to. Nonbanks have been more of a challenge than the banking system. But even banks have been openly reluctant to engage in the same levels of lending and leverage as before. For the first time since the Great Depression, the financial system just won’t grow.

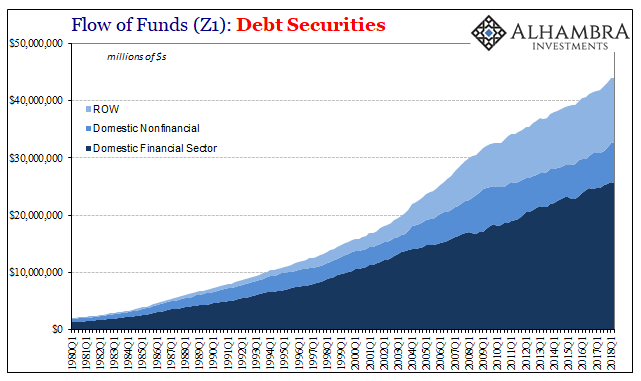

The recovery in it is actually worse than it may already appear. If lending is the bank side, securities are the savings side. It is this latter category which you might otherwise suspect would be untouched by the same negative factors plaguing the banking system. But, again, money and credit have been blurred, meaning that the eurodollar’s constant negative presence places even the securities side in liquidity risk.

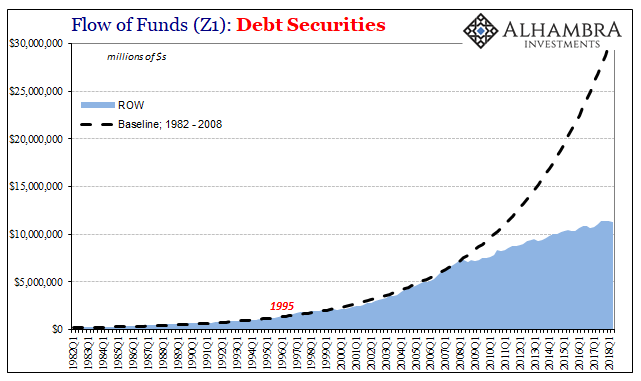

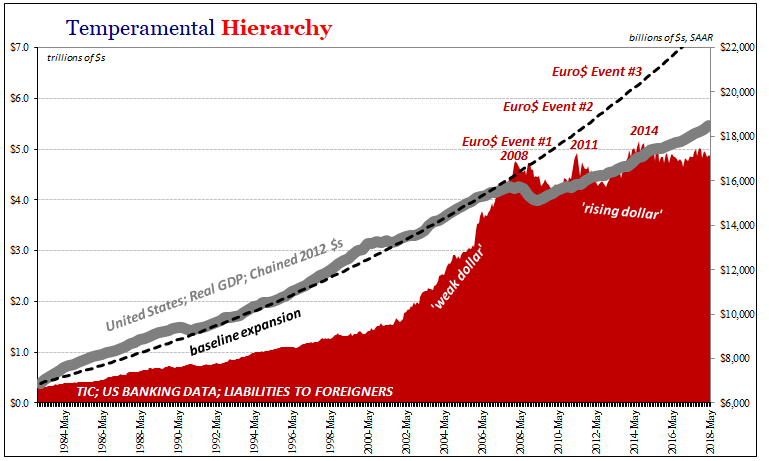

That’s especially true of the ROW sector, foreign institutions of all kinds which before 2008 couldn’t get enough US securities (particularly MBS). But having become synthetically “short” by funding in dollars, they are extremely reluctant to hold them so long as dollar funding represents a huge, intermittent risk.

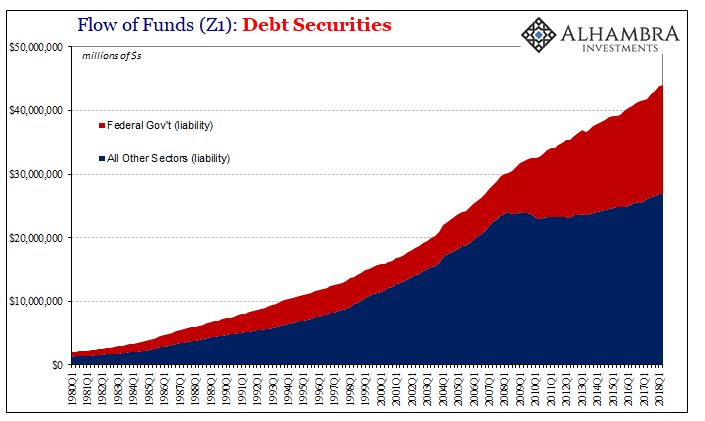

Not only that, which class of securities are being prioritized in this new post-2007 paradigm? Those with the highest perceived liquidity characteristics, those like UST’s. Almost exclusively UST’s.

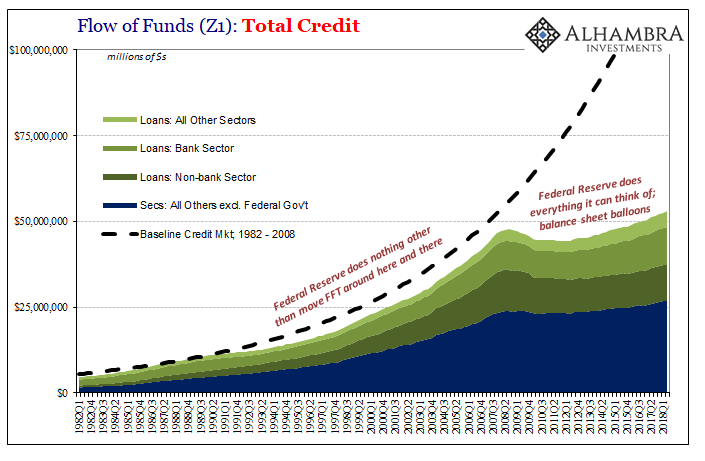

When we put the two halves together, loans and securities, what we find is a credit market that just doesn’t operate the way it used to. Subtracting the federal government’s obvious binge, the difference is greater still.

We can’t help but notice that when the Fed was doing next to nothing (in truth, it was doing nothing) the credit system grew unabated. As it began to do more and more, the credit market further and further deviated from prior history. However you want to account for the difference, that’s not successful monetary policy by any rational standard.

What it really says is that the Fed is and has been a bystander. They do more things when things are very wrong. They don’t solve the issue, they merely signal that there is one.

So long as the system functioned they could do next to nothing and take credit for any positive results. Once it no longer functioned, there wasn’t anything the central bank could do about it. There still isn’t.

Outside the US government, the US economy remains stuck in the throes of a debt crisis. It isn’t one like a credit-fueled bubble that you often hear about; rather, the problem is there isn’t enough. We can regret that all we want, but the modern economy is highly financialized.

But it’s not really debt that is missing. Whether in the form of lending or securities issued, the problem is eurodollars and liquidity risk. As the money system goes, the financial system and therefore economy follows. Bernanke got that part of the theory right. It’s the money part he repeatedly botched.

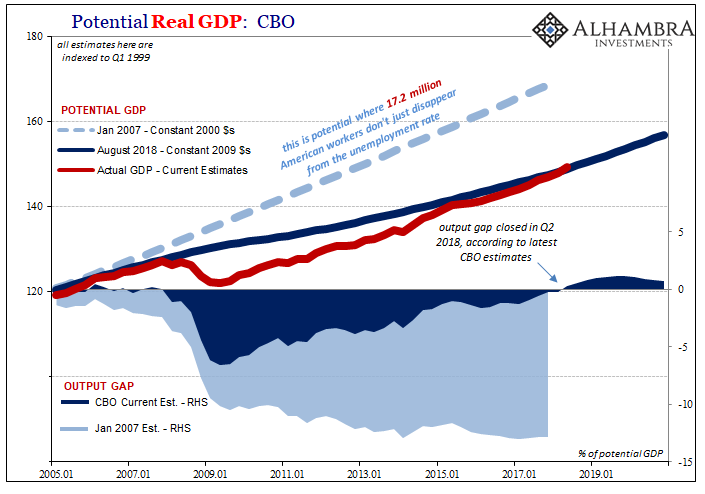

Isn’t this just deleveraging, the very thing many people claim is necessary? If it is, why hasn’t the economy started to grow again? Or even banks, for that matter. A simple balance sheet recession wouldn’t take ten years and cost trillions to the economy in lost output. Nor would it be an ongoing global problem creating so much currency instability.

Furthermore, it would not be accompanied by constant deflationary signals. If deleveraging has been taking place, the economy would be running at, rather than way below, its potential. There wouldn’t be repeated monetary events scaring away global intermediaries from carrying out prudent credit market activities. At some point, they would have been buying something other than UST’s.

If ten years isn’t enough, then it never will be.

The financial system is instead broken. We don’t know what the “right” size of the credit market might be. There are any number of signals that tell us this isn’t it. Even in 2018, a whole decade after the big one, amidst what central bankers say is a strong and booming economy, the credit market continues at its historically low pace.

Discounting federal debt, total credit grew by just 3.8% year-over-year in Q2. That’s down from 3.9% in Q1 and 4.3% in Q4 2017. It’s not really materially different than in any quarter since 2013. Something keeps holding the financial system back.

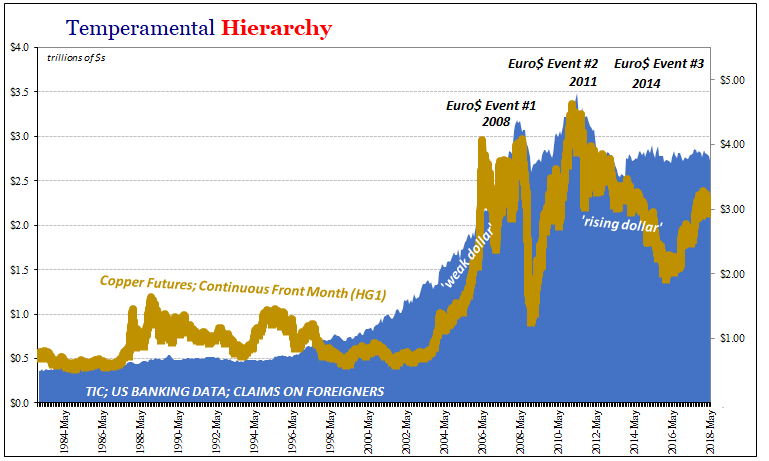

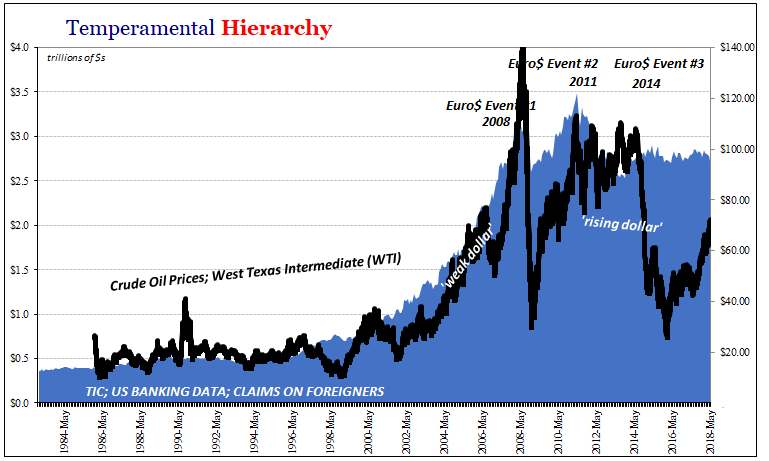

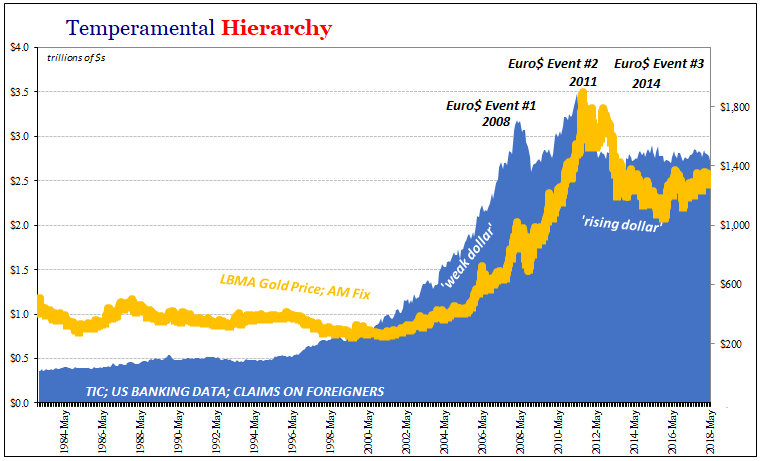

The big reason for the slowdown in 2018? ROW. Monetary risk of eurodollars. Again.

Stay In Touch