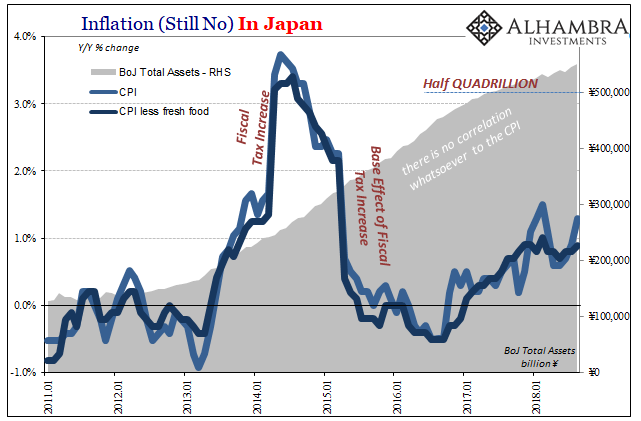

Just like Jay Powell is surely hoping for some help from Mother Nature, the central bankers at the BoJ have to be wishing for more on their side of the Pacific. The US Federal Reserve will be looking for a repeat of last year’s Harvey and Irma effects out of Florence. It looks like they’ll need them. Japanese officials have been aided now twice in 2018 already, with inflation perking up again in August.

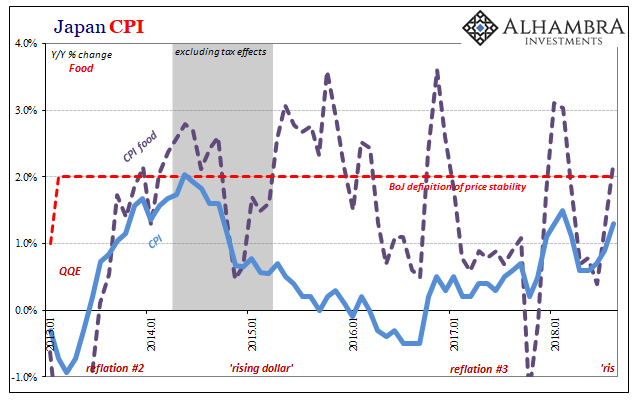

Japan’s CPI rose 1.3% year-over-year last month. It was the first time above 1% since the first three months of the year. In both cases, the acceleration was and is predicated on food. In the earlier instance, despite the massive hype it didn’t last long at all. After getting as high as 1.5% in February, making policymakers practically giddy, the inflation index dropped back to just 0.6% two months later. There was noticeably less giddiness.

Food prices, like oil prices, aren’t the inflationary basis these Economists are looking for. Though they won’t admit it publicly most times, they know it, too. Commodities can affect the CPI in the short run, of course, but they don’t do anything about keeping inflation up. In fact, food prices in particular, these spikes can be harmful to consumers since they aren’t being accompanied by broad-based income gains.

Food prices have jumped recently due to persistent bad weather. An earthquake that struck in early September could keep food prices high for another month, and the BoJ in the game as far as headline rates.

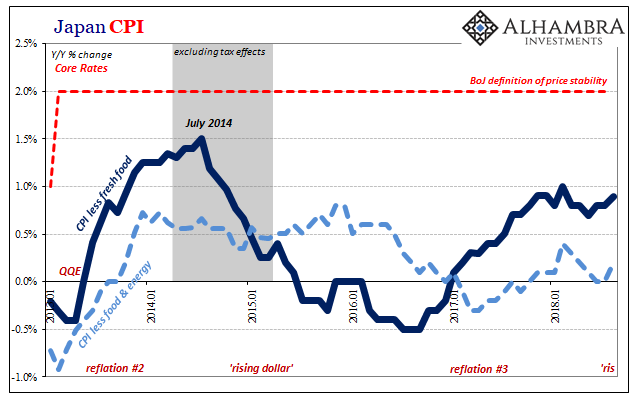

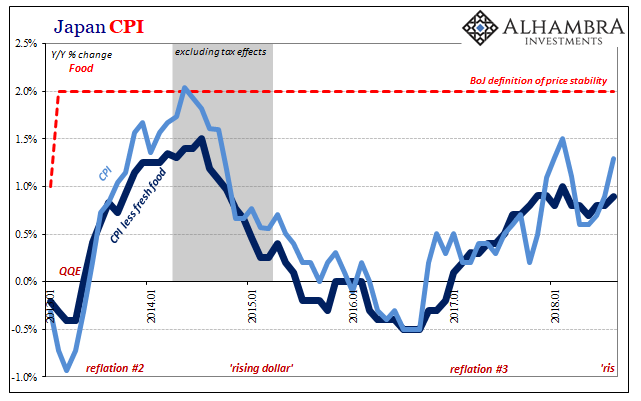

That’s pretty much all they have to show for QQE in 2018. Core rates, CPI indices excluding the volatile food and/or energy parts of the consumer basket, haven’t budged. Those are the only pieces that are moving inflation in Japan.

The Bank of Japan appears to be carrying out “stealth tapering” anyway. The central bank has trimmed its purchases of certain asset classes, including some longer-dated government debt. Just today, officials bought ¥50 billion in government securities at 25 years maturity and beyond. That’s down from the ¥60 billion pace in this segment established back in July – when stealth tapering was first cryptically announced.

Many are taking this as a sign BoJ has finally succeeded with QQE, or at least the central bankers in charge of the program believe they have. This would put BoJ in the same class as the Federal Reserve; buying success without evidence for it.

In its statement for the July 31 meeting, the bank would only say that now longer-term bond yields “may move upward and downward to some extent mainly depending on developments in economic activity and prices.” The latest official release, published two days ago, reaffirmed that view.

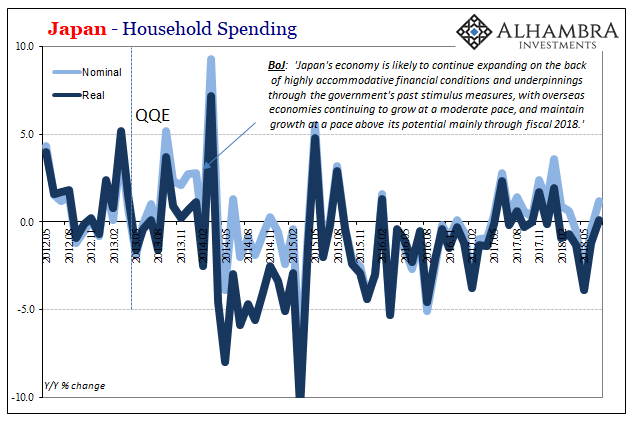

The reason is that Japanese central bankers continue to see what they call a “virtuous cycle from income to spending being maintained in both the corporate and household sectors, mainly against the background of highly accommodative financial conditions and the underpinnings through government spending.” In other words, this “stimulus” stuff has been going on long enough it has to work one of these years. Why not 2018?

In truth, they’ve been talking, speaking, and writing about the “virtuous cycle” since QQE was first introduced five years and five months ago. Half a quadrillion in assets later, there’s still no concurrent evidence it exists today. Always the future tense.

What really has happened is something very different. The Fed, by virtue of being out in front for similarly future reasons, has provided cover for other central banks to follow in its footsteps. US central bankers and Economists have redefined recovery so that the new definition simply matches current conditions.

By doing so, and acting, they allow other central bankers to point to the US recovery as a basis for expectation on all things economy and monetary policy. See, it did eventually work in the US!

No one is supposed to notice how the FOMC isn’t exactly robust in its defense of its position. They are acting, but with unusual care. The economy is strong, they say, but somehow that doesn’t merit more of a monetary policy response.

Central bankers here and there (and in Europe, at least until January when the European economy “unexpectedly” hit a wall) are just hoping that this time will be different. There is no evidence that it is. BoJ officials, like Fed officials, have their fingers crossed which is why they aren’t being openly assertive about anything.

That’s the whole point of “stealth” tapering. To try to say it worked without really challenging your own assertion that it did.

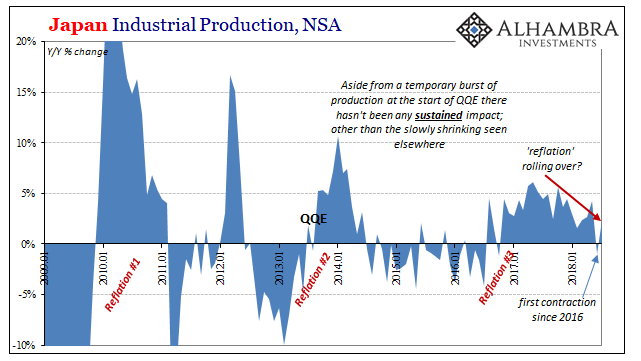

One global factor never never shy about testing central bankers, however, is starting to do so again. The Bank of Japan, as the Federal Reserve, would’ve been better off using 2017 as the unclear basis for declaring victory rather than leaving it to the real monetary system. They waited too long, globally synchronized growth once again disappearing under their noses.

Even Japan’s core CPI rates look to be peaking way short, as does Japan’s economy. This year’s getting hot, and not in terms of consumer prices. Central bankers can claim that they don’t want to crash markets on their way out after a decade of their heavy handedness. If they truly had succeeded, markets wouldn’t care that they are headed for the exits. They would, in fact, celebrate – in a sustainable fashion – actual recovery.

Stay In Touch