At one time, economics actually cared about eurodollars. Maybe it was because the thing was so new, it was a hot, sexy topic, the kind of strange and unusual deviation from the norm that can grasp someone’s attention and hold it. Perhaps it was the way in which it all began, an entire monetary system clandestinely sorted together out of almost thin air.

Paul Einzig, one of the first to notice and comment on eurodollars, would say in the early 1960’s that bankers practically begged for him not to write about it. There was some real danger to the system, no one really sure what might happen if authorities eventually stepped in. They never did, though we will never really be sure why they didn’t.

In 1970, Klaus Friedrich, then an assistant professor at Penn State, wrote for Princeton University’s Studies in International Finance, “One of the most striking aspects of the rapidly growing Euro-dollar literature is the fact that so much has been written on the basis of so few data.” We can very much appreciate that second one. There is practically no data still today.

Rapidly growing literature? In 1970, yes. Scientific curiosity in the ascent of econometrics, however, was snuffed out by mathematic irregularities. Simply put, eurodollars blow up DSGE. Therefore, Economists placing every emphasis on their regressions and statistics have for decades pretended eurodollars don’t exist as money.

The lack of data Professor Friedrich lamented obviously remains a frustrating deficiency almost a half century later. We have very little to go on apart from prices. For central bankers, therefore the public, that far-too-often means they are left confused over price movements (“transitory”) even for big things like the dollar.

We know the eurodollar is there, but of the main questions, who, what, where, when, how, we only really know “who.” We’ve always known it’s banks.

Friedrich again:

At any stage of the process of intermediation, which normally involves interbank transactions, dollar balances may be converted into other currencies and passed on in the form of balances in other curencies. If the other currency is not the domestic currency of the country in which the conversion takes place, the deposit becomes part of the broader Euro-currency market. A bank in Switzerland, for example, may convert a Euro-dollar deposit into a Euro-sterling claim on a bank in France. The terminal stage of Euro-dollar intermediation in this case is a bank rather than a nonbank borrower. [emphasis added]

This is the double-edged sword for modern Economics; as a purely bank phenomenon Economists can claim that it can’t be money since its entry into the real economy isn’t straightforward. But they do so by also ignoring how entry or not there are real economic consequences for how the system functions at every given moment.

Friedrich warned in 1970:

A related problem arises, however, in case a bank converts Eurodollar balances into its domestic currency, in order, for example, to make domestic commercial loans on the basis of funds obtained in the Euro-dollar market. While the source of credit has been the Eurodollar market, its use is obtained in the domestic currency. Once more the bank is the terminal stage of Euro-dollar intermediation and to consider only dollar positions vis-à-vis nonbanks would underestimate Euro-dollar activity.

Not just underestimate, though, grossly understate.

The eurodollar to which Professor Friedrich and a great many former economists, as opposed to these modern Economists who declined to follow them, studied was more in keeping with the original definition. A eurodollar was then a deposit liability located offshore. Even by 1970, though, that had already started to change, to proliferate as Alan Greenspan would notice throughout his long tenure at the Federal Reserve.

This modern eurodollar includes all sorts of monetary functions, all interbank, that distort the notion of a dollar deposit even offshore. These are now long chains of pure bank liabilities of every color and flavor. From derivatives and FX to repo and collateral.

So, we know the eurodollar system is out there, and we know the global economy feels its rise and fall. But, just like in 1970, we don’t have a whole lot of data to provide insight into the one or the other.

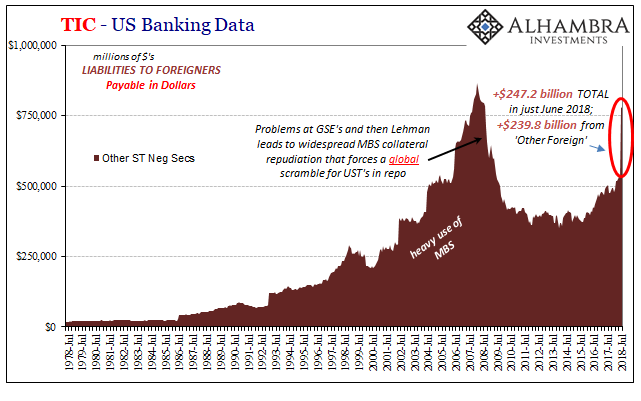

The few series we do have in 2018 have been very interesting. The TIC figures have been quite vocal about collateral. That corroborates May 29 in global prices. But if TIC didn’t specify who it was that supplied this potential quarter-trillion in collateral, FRBNY, ironically, tells us who it wasn’t.

Beyond just collateral, FRBNY collects a number of data points on the activities of primary dealers. Whether they would ever know it or not, and they don’t now, the New York branch’s mandate with regard to dealers overlaps with how things actually work in this offshore bank-driven eurodollar. If central banks aren’t central to it, and they aren’t, dealers are.

According to TIC, “other” financial institutions (not banks and not central banks; at least not central banks directly) were the source of “other” ST securities.

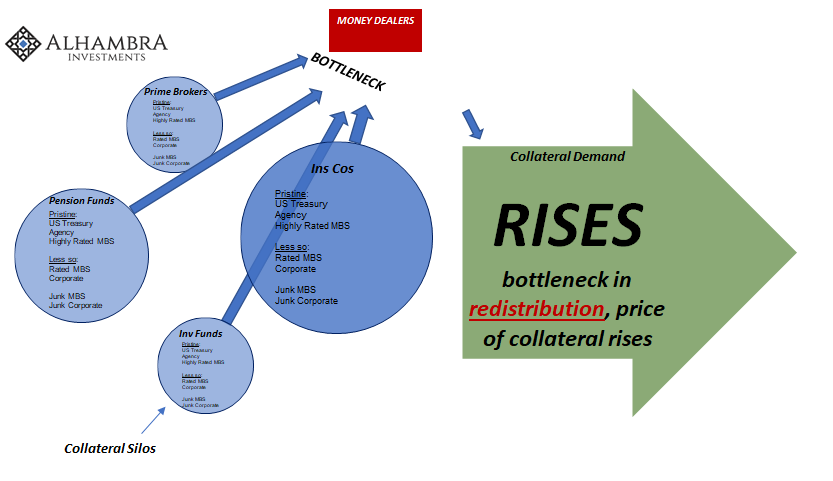

Any kind of collateral bottleneck should have been handled by those firms who are in the business of handling collateral. That’s what dealers are for. As noted here, they perform a redistribution function, managing and attempting to equalize the global supply of collateral for repo and FX against demand for it.

Those who supply a great deal of the collateral necessary to keep things running smoothly are not those who use it (insurance companies, for one, are funded by contract premiums not repo or dollar swaps; they use those premiums to buy portfolios of otherwise idle securities that then dealers can “borrow” to relend across the global system, everyone pocketing an economical spread for their trouble). Without someone in the middle, things can get out of hand.

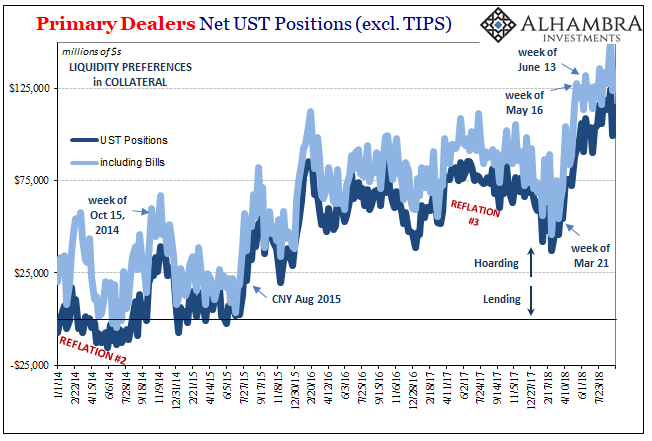

Dealers aren’t purely risk-free running matched books, though. What I mean by that is dealers while also performing redistribution functions also have their own funding needs. Given that situation, you can easily guess who might get first crack at collateral if things get rough.

Where were the dealers on May 29? Hoarding. Hoarding their asses off.

Between mid-March and mid-May, the very period when all the global fireworks erupted, FRBNY reports that primary dealers were hoarding an astounding amount of UST securities – both coupons as well as bills (so much for T-bills being the culprit). By August 2018, and that last little blip in the dollar, it had grown to a record level.

We also know it hasn’t been the domestic repo market where collateral is so obviously tough to obtain. That leaves us, as the dollar’s rise, suspicious again of overseas eurodollar markets.

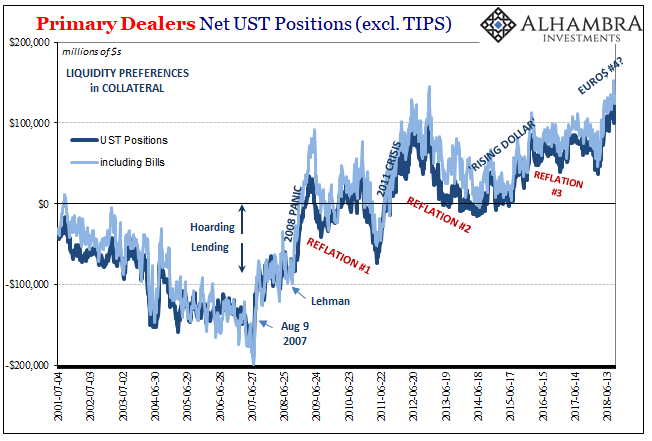

Throughout the intermittent eurodollar squeezes since August 9, 2007, like TIC the dealer data has been consistent in showing us the procyclical, therefore unfortunate, response of the dealer system. The FRBNY data may be only one part, the domestic subset of the global interbank network, but it’s a big part and it has been reliable in the past.

Whether after Lehman, the 2011 crisis, the big “rising dollar” in 2014-15, or now in 2018, dealers become uniformly risk averse during these periods when money hierarchy breaks down. Pure liquidity risk, and no small wonder why. Central bankers can’t congratulate themselves enough for especially engineering what they call “resilience” in the financial system.

The interbank participants, on the contrary, can’t help but wonder if these central bankers actually believe it or if they are just spouting off positively to the public. In either case, global eurodollar banks know that they are on their own and can count on very little help from officials; absolutely nothing from major central banks.

Faced with rising risk, who wouldn’t hoard? It’s the only prudent option. If dealers hoard for themselves, what’s left for everyone else besides a bottleneck. And in economics, supply disruptions mean huge price spikes. May 29.

Unfortunately for the world, it is also, again, procyclical; reinforcing all the negative monetary habits that have over the last eleven years pushed the economy off of the recovery track and into persistent stagnation if not depression. Why isn’t global growth synchronized any longer? Why might it be synchronized again soon enough, but the wrong way?

One last note. Dealers as of mid-September are still hoarding an eye-popping amount of collateral. Not only does that confirm May 29 and TIC, it also suggests it might not take much to repeat, given persisting strain indicated by one of the few data points in effective eurodollar money. In short, this latest in a string of eurodollar problems is still a problem.

Stay In Touch