There had been whispers that the FOMC would have to undertake a second “technical adjustment” this year. Is it coincidence that the eurodollar futures curve inverted on the same day, June 13, Jay Powell announced the first one? Perhaps, but given what we are talking about here there is a fair chance they are related, especially in the close aftermath of May 29.

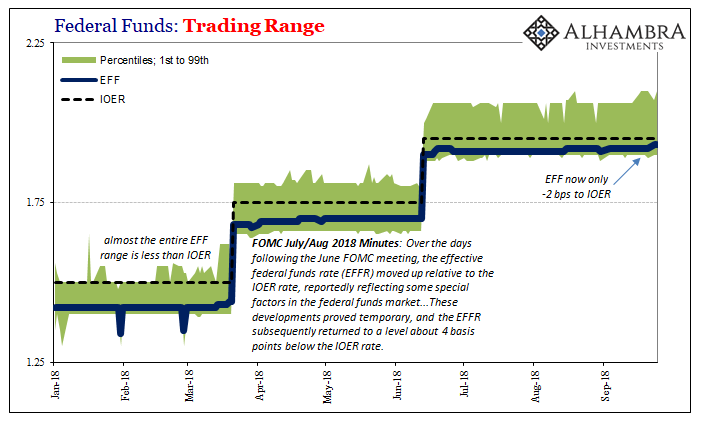

What are we talking about? The effective federal funds rate (EFF) has spent much of this year vexing US central bankers. For reasons they can’t seem to pin down the rate has moved upward inside the policy “range.” That range is defined by the reverse repo (RRP) “floor” on the bottom. On top is, or was, IOER.

As EFF began to make officials squirm on its way up toward the upper parts of the range the FOMC in June voted for this “technical adjustment” to get it back under control, or try. IOER would be set 5 bps less than the upper bound so as to pressure the effective rate lower (under the theory of money alternatives). Thus, at the last “rate hike” RRP was raised by 25 bps while IOER only 20 bps.

In the months since, EFF has squeezed a little higher still. As of last week, it was 3 bps underneath IOER. At such a close level, some were wondering if the FOMC might vote for another adjustment to IOER the same as in June. EFF apparently needs another official push, the first one didn’t really do much.

Practically daring policymakers to do something about it, EFF moved up to 1.93% on Monday. It was the same just 2 bps less than IOER yesterday, too (we don’t know what it was today, the last day before the current “rate hikes” are carried out, since FRBNY won’t publish the official calculations until tomorrow morning).

Though the Committee voted to raise the corridor today, they will move both RRP and IOER by 25 bps – no second “technical adjustment” yet despite where EFF in all likelihood sits right now.

Why not?

To be candid, I think they are scared. After all, why make the first adjustment? The answer is any rebellion in federal funds. If EFF continues to behave independent of policy levers, corridors, and all moral suasion, then that sends the same chaotic signal as chaotic money markets have been sending since the initial breakdown in August 2007. In other words, if the Fed can’t control federal funds, what can it?

Nothing.

If they adjusted IOER a second time and EFF remained 8 bps or now 7 bps below the top, that would be 2 bps or possibly 3 bps above IOER. It would instead prove IOER is useless (not that we really need any more proof). That would further show that the Fed, by sticking with something so comprehensively and consistently ineffective, is in a tough spot with few actual control levers in just money markets – forget about anything else outside of the mechanical.

At this juncture, why risk placing a spotlight on IOER and having it blow up (again) in their faces? Better to watch EFF slowly boil up to it than to give this dysfunction signal a big push toward the wrong kind of confirmation at a crucial juncture.

Chicken hawks. Better to be thought powerless and impotent than to adjust technically and remove all doubt. Central banks aren’t central, and you have to wonder if central bankers are finally starting to suspect this truth.

Stay In Touch