The global economy was in very rough shape in 1980. Caught in the spiral of the Great Inflation, there was practically nowhere to hide from ripping upheaval – beyond just the economic problems. Despite trying seemingly everything for an entire decade, nothing Economists came up with would rebalance the system.

They kept saying they only needed time for their schemes to work. By the summer of ’80 no one outside the ideology was left to believe them. Even Congress in rare bipartisan fashion denounced “demand side” Economics for leading the country into chaos.

The US economy finally broke. After sustained waves of inflation combined with higher and higher unemployment (just Milton Friedman has predicted more than a decade before), in January 1980 the nation fell into official recession. It was only the beginning. Though that particular contraction was short, lasting only seven months “officially”, according to the NBER, it was severe on its own and merely the first of two in close succession.

In August 1980, the month of recovery, which only meant the bottom of that recession, interest rates were obscene. The 10-year US Treasury had ended 1979 yielding around 10%. By February 1980, it was nearly 13%. Now that was a BOND ROUT!!!!

Mortgage rates, of course, followed. In December 1979, the average 30-year fixed loan cost a little less than 13% interest. In April 1980, it was as high as 16.5%.

Mortgage rates would fall during that spring and summer, but those who were intent on buying and building houses for the month of August had booked their loans at or near these peaks. According to the US Census Bureau, in that first month of initial recovery homebuilders had managed to sell 61,000 (not seasonally adjusted) new single-family dwellings across the United States.

That was down sharply from August 1979, when sales of new homes had reached 68,000. The peak for that particular housing cycle was two years earlier in August 1977. During that month, the government estimates 74,000 new homes had been built and sold.

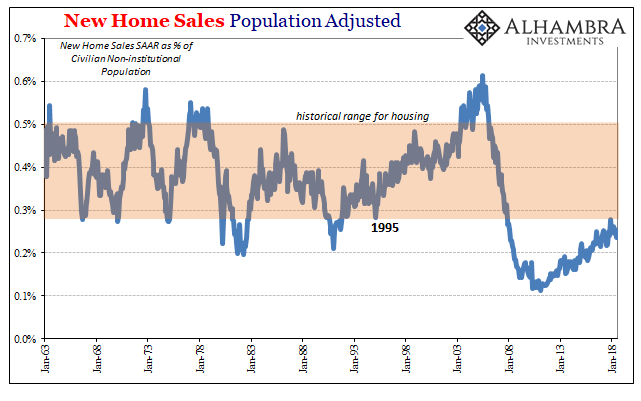

In figures released today, the Census Bureau reports that in the month of August 2018 50,000 (not seasonally adjusted) new homes were sold. 50k. That’s one-third fewer than in the same month in 1977, more than four decades ago. It’s 18% less than in August 1980 at the bottom of one very sharp recession when interest rates were out of control and the unemployment rate had jumped from around 6% to nearly 8%.

In August 1980, amidst universally accepted economic disorder, the Civilian Non-Institutional Population was a shade more than 168.1 million prospective American workers. The Employment-Population ratio was 58.8% and declining.

In August 2018, the Civilian Non-Institutional Population is 258.1 million, or 53% more than it was in the same month 38 years ago. The Employment-Population ratio is 60.3% in the latest estimate, and the average 30-year mortgage rate has “climbed” to around 4.6% from about 4% last year. The unemployment rate is less than 4%, as everyone keeps reminding you. It has even been below mortgage rates for all of 2018.

These statistics on the housing market are not consistent in any way with a healthy economy. They don’t even compare favorably to one of the worst economic periods in our history.

They say that the US economy is booming. It’s not. Some parts of it are doing OK, even quite well. A huge part, too big a part, clearly is not.

That’s always the challenge even in the best of times. A true economic boom leaves some people out of it; that’s just the nature of free markets and capitalism, the messy, unpredictable invisible hand. But during a true economic boom, the proportion who unfortunately reside in this undesirable position is exceedingly small.

If that segment is unusually perhaps historically large, then the economy isn’t booming it has done something else entirely. Housing is a key indicator along these lines and it is only one of many.

For 2018, we know what the problem is and it is actually two problems. The economy shrunk ten years ago and no one will admit it. The housing data and others like it (a lot of other data) all point toward these sorts of historical comparisons that just don’t make sense for such an awesome economic boom.

That’s because Economists and officials, egged on by politicians on both sides eager to put all this economic dissatisfaction behind them, have changed the rules. A recovery used to be a recovery, no updated definitions needed. Nowadays, a recovery is whatever’s going on right now.

Thus, if the proportion of Americans still stuck outside the “boom” continues to be large, as the housing data proves conclusively, then they just don’t count anymore. It’s like an automaker who was running four assembly lines in 2007 but was forced to shut one down in 2008. Ten years later, the company is still running just the three but now claims it’s at full capacity as if the fourth line, which is still there and theoretically available if work ever actually picks up, never existed.

That’s how you run into these absolutely mind-boggling comparisons. We are all just supposed to pretend this didn’t happen; that home builders managed to sell 61,000 new homes in August 1980 under plain awful economic conditions, but only 50,000 in August 2018 despite enormous population growth and an aggressively awesome economy?

It’s a recipe for social and political upheaval. That’s what we’ve seen already, and that was when things were shrunk but at least mostly positive. There are growing signs we might not even have that moving forward.

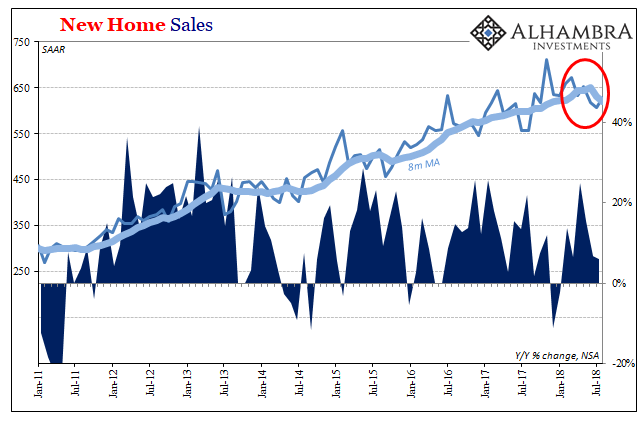

New home sales are recording the same real estate slump as other housing data. On a seasonally-adjusted basis, at an annual rate, the number of new homes sold was 629k in August 2018. That was up from 608k (revised lower) in July, but remaining on a clear downward trend. The Census Bureau advises that when looking at monthly changes you use an 8-month average because of the natural volatility in the data.

The 8-month average is now down for the second month in a row. That’s the first time that’s happened since October and November 2015 – the depths of the “rising dollar” and the economic downturn cycle following from it.

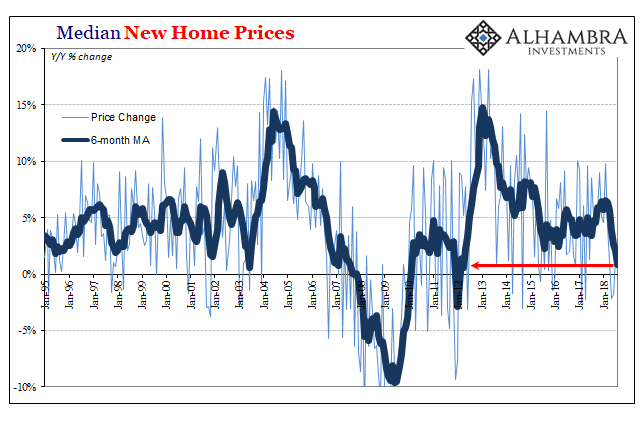

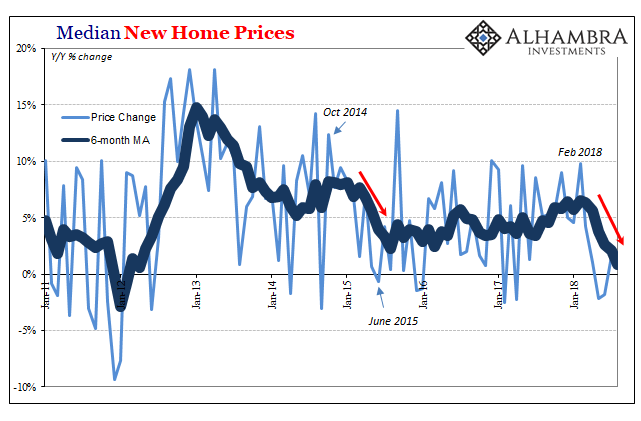

It’s not just average sales that has suggested another rolling over. The median sales price of new homes has also decelerated, indicating builders are worried about inventory and demand even at these historically low levels. While prices rose year-over-year in July and August 2018, after declining in May and June, the average gain is now practically zero for the first time since early 2012. The deceleration over these months looks exactly like 2015 in the throes of that downswing cycle.

The housing data suggests neither the condition nor the direction for a booming economy. The FOMC will today “raise rates” anyway. This is all, in a nutshell, the flat yield curve at ~3%.

Stay In Touch