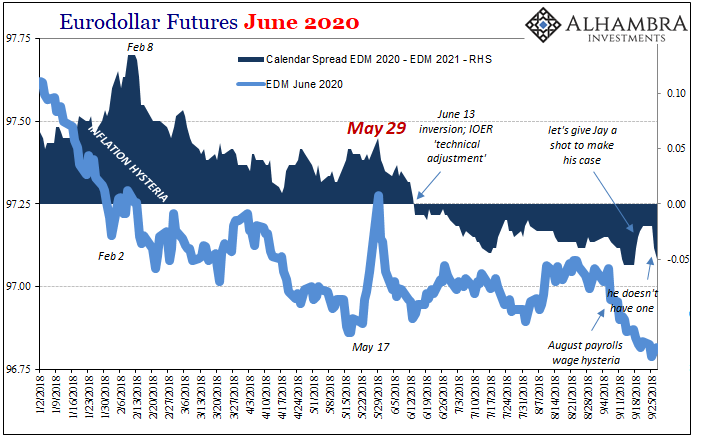

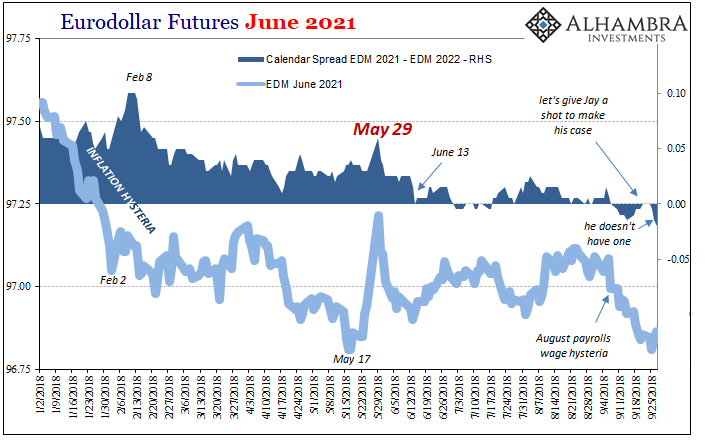

June 13 sticks out for both eurodollar futures as well as IOER. On the surface, there should be no bearing on the former from the latter. They are technically unrelated; IOER being a current rate applied as an intended money alternative. Eurodollar futures are, as the term implies, about where all those money rates might fall in the future.

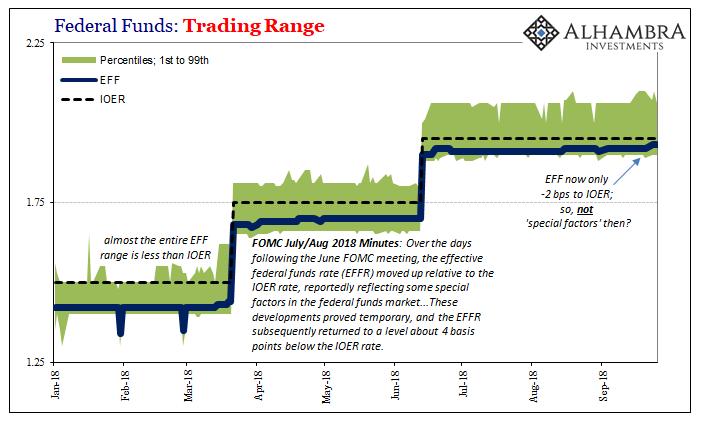

Still, the eurodollar curve inverted conspicuously starting June 13. That was the day of the prior “rate hike” before the latest one this week. It was also the first “technical adjustment” to IOER. The Fed announced that going forward (meaning June 14 onward) IOER would be set at 5 bps below the top of the federal funds range. It had previously been pegged right at the upper bound.

Effective federal funds, as noted yesterday, has been misbehaving again. Central banks can’t have money rates acting independent. IOER was intended to get it back in line.

That’s the probable relationship, if there has been one, with eurodollar futures. Another crack in the foundation showing that throughout this “rate hike” regime the FOMC really doesn’t know what it’s doing. And if it doesn’t have a good handle on EFF, the most basic of basic, then how can anyone have any confidence in the Committee over much bigger things like the economic acceleration they claim as the reason behind their policy switch?

In short, if you have to do something about EFF, and use IOER of all things, there is an even greater chance you have it all wrong.

That’s ultimately what the inverted eurodollar curve is saying. At the front, the FOMC is going to keep moving short rates up – but only for an as-now undeterminable amount of time. Over time, there is a more than trivial chance they will end up turning around in some way like the last time the curve inverted.

The eurodollar market is not unforgiving, however. For the seven or eight trading sessions (depending on your choice of calendar contract), the curve started to go back toward even in these inverted corridors. The main one has been June 2020 to June 2021, since early September the June 2021 to June 2022 has gone under, as well.

In the runup to this week’s FOMC decision, the less distorted curve was essentially saying to Jay Powell and his compatriots the market was willing to hear their case. The Fed thinks things are getting better and there isn’t any need to be overly careful. IOER and EFF bely that notion.

Wednesday came and went and the market didn’t get anything from the FOMC but the same. Inversion is right back on again – in the EDM 2021-22 space it’s now even wider than before.

And EFF is still 2 bps below IOER, even though at the prior Fed meeting at the end of July the FOMC definitively declared how this whole EFF/IOER dustup was temporary; transitory, even. It wasn’t.

They really don’t know what they are doing. The consequences of that are where eurodollar futures are trading and again trending.

Stay In Touch