On March 9, 2007, Rhode Island Representative Patrick Kennedy introduced HR 1424. At the time it was to be known as the Paul Wellstone Mental Health and Addiction Equity Act of 2007. The bill contained five small sections intending to ensure equal coverage and treatment for mental health issues under insurance claims.

It passed the House but then gained an enormous Senate amendment. Since Congress was attempting to mess with health insurance mandates, several Senators wanted to expand the messing to include the prohibition of genetic discrimination. No person, the bill reasoned, should be charged more for coverage once the results of any genetic testing became known.

HR 1424 was stripped of this amendment in early 2008, with this other bill becoming a standalone HR 493. The latter eventually became law and is known today as the Genetic Information Nondiscrimination Act of 2008.

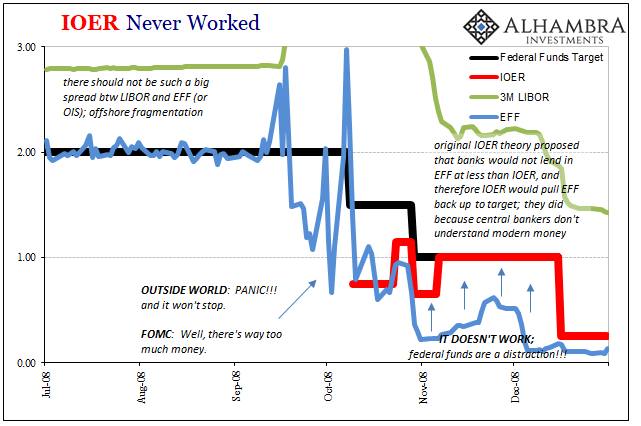

This left 1424 sitting around. In late September, Congress would be rushed into an emergency bailout of the financial system. After hearing over and over from all the “experts” that everything was safe, suddenly those same experts were as panicked as markets.

On July 15, 2008, everything turned – again. There had been a modest rebound before, a slight sigh of relief after the world seemed to have processed the near failure of Bear Stearns. A small breeze of reflation even blew, to which officials began their track of cautious optimism.

They had no cause for it, though, only a biased and emotional appeal to how, again, the worst just wasn’t possible. Not with Bernanke, the man who wrote the book on the Great Depression, in charge.

Congress was in session on July 15, with Ben Bernanke testifying as did Treasury Secretary Henry Paulson. Senator Chris Dodd would open the sham by shamming big time:

CHAIRMAN DODD. In considering the state of our economy and, in particular, the turmoil in recent days, it is important to distinguish between fear and facts. In our markets today, far too many actions are being driven by fear and ignoring crucial facts. One such fact is that Fannie Mae and Freddie Mac have core strengths that are helping them weather the stormy seas of today’s financial markets. They are adequately capitalized. They are able to access the debt markets. They have solid portfolios with relatively few risky subprime mortgages.

I wrote a few months back on the occasion of the tenth anniversary of this shameful sequence:

The only thing true in that statement was the very last bit; the GSE’s did have solid portfolios with very few subprime mortgages contained within them.

As it turned out, just six days later Secretary Paulson would be meeting in New York with hedge fund managers and Wall Street bankers. According to a Bloomberg investigation conducted and published years later in November 2011, Paulson discussed with them “a possible scenario for placing Fannie [Mae] and Freddie [Mac] into ‘conservatorship’.”

Subprime was just that powerful, apparently.

They would indeed fall into conservatorship in the second week of September 2008, news that was pushed off the front pages by what followed in the third week with the wondrous calamities of Wachovia, AIG, and Lehman Brothers.

The old House bill was resurrected and given a new amendment, this time called the Emergency Economic Stabilization Act of 2008. It was signed by President Bush on October 3, 2008, exactly ten years ago today. HR 1424 which had begun its legal life as a minor health insurance tweak ended up as one of the biggest government projects in our nation’s history: TARP.

The Troubled Assets Relief Program, the $700 billion plus “bailout” scheme, is Title 1 of the Act. Section II clearly defines its broad purposes (meaning, they aren’t clearly defined at all):

(1) to immediately provide authority and facilities that the Secretary of the Treasury can use to restore liquidity and stability to the financial system of the United States; and

(2) to ensure that such authority and such facilities are used in a manner that—

(A)protects home values, college funds, retirement accounts, and life savings;

(B)preserves homeownership and promotes jobs and economic growth;

(C)maximizes overall returns to the taxpayers of the United States; and

(D)provides public accountability for the exercise of such authority.

Lots about homeowners and housing, very little about liquidity and stability. The two, however, were intricately linked just not via subprime mortgages.

The bill’s mistakes are the same mistakes everyone keeps making. The very first provision under TARP, establishing the authority of the Treasury Secretary to do anything, is his ability to purchase or make commitments to purchase “troubled assets.”

To figure out what a “troubled asset” was, Paulson was authorized to discuss with all the relevant experts the government had available – you know, those at the Federal Reserve, OCC, Office of Thrift Supervision, etc., all the people who had no idea where all this trouble for assets came from.

Which is why, less than two weeks into its life, the Troubled Asset Relief Program was changed so that it would no longer focus as much on troubled assets. On October 13, 2008, amidst a full-scale Wall Street stock market crash, Secretary Paulson announced $250 billion would be used to “invest” (read: bolster capital ratios) in the banking system. One hundred twenty-five billion would be funneled to nine big banks (Citigroup, Bank of America, Wells Fargo, Goldman Sachs and JPMorgan Chase, primarily) with small and mid-sized institutions receiving the other half.

TARP at that point should’ve been renamed to something more appropriate; the We Really Don’t Know What We Are Doing Act of 2008. If you don’t have any idea what’s really wrong, you aren’t going to fix it no matter what. That about sums up 2007-09.

In response to the change, Ken Rogoff, a Harvard Economist and advisor to Republican Presidential nominee John McCain, dryly observed “We’re trying to prevent wholesale carnage in the financial system.” Small wonder Mr. Obama would win the vote just a few weeks further into the disaster.

An unused mental health bill becomes the law into which government officials would in the emergency attempt to stabilize the economy by starting from a position where they don’t understand the emergency nor how it was creating so much global instability. Apart from the still unfolding tragedy, it is too perfect. The entire time it has been just that surreal.

You can always tell what won’t happen by how these fools label their laws: the Emergency Economic Stabilization Act of 2008 arose from an emergency “they” said was impossible, an irrational smear upon the good standing of the financial system, and its passage and usage did absolutely nothing to stabilize the economy. What followed throughout Q4 2008 and Q1 2009 all the while TARP was being dispersed was, by far, the worst contraction since the Great Depression.

As Senator Dodd challenged, distinguish between fear and facts – only it was him and the government that failed to live up to any minimal standard. Adversity doesn’t build character, it reveals it.

What’s much worse, however, is that in the ten years since HR 1424 the economy that has come out of it is on track to “somehow” underperform the Great Depression. They had no idea what was wrong then, are we to just believe they ever sorted it out? Not a chance.

Stay In Touch