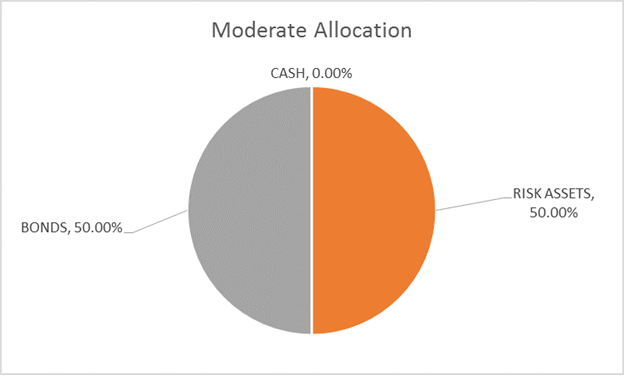

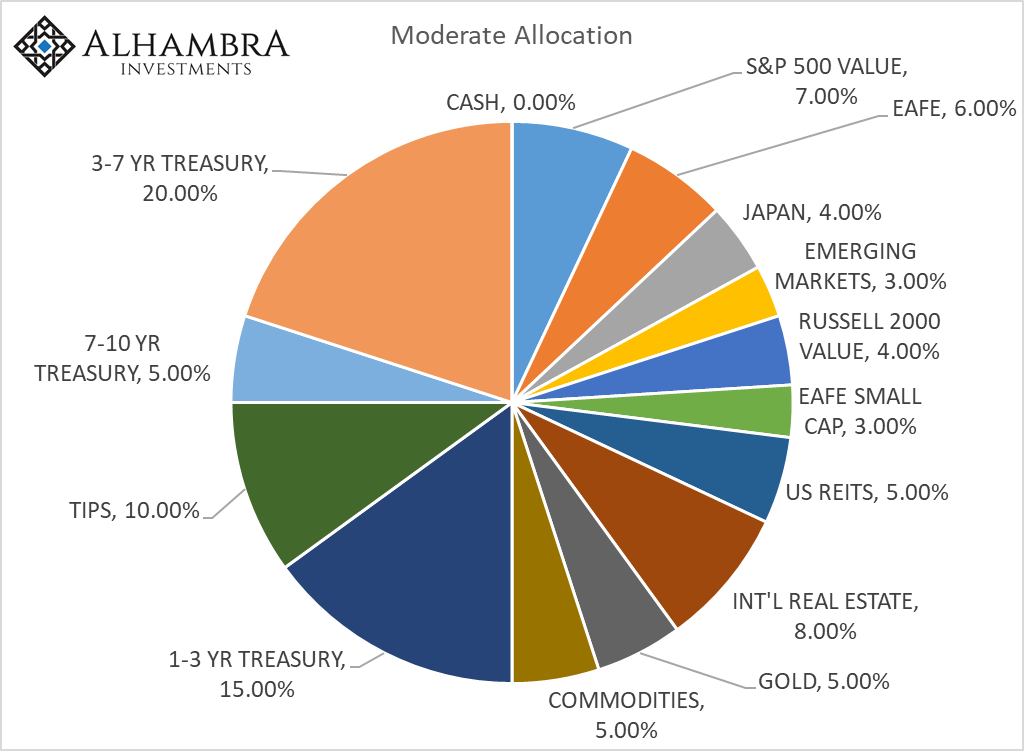

The risk budget is unchanged again this month. For the moderate risk investor, the allocation between bonds and risk assets is 50/50. There is a minor change in the bond allocation.

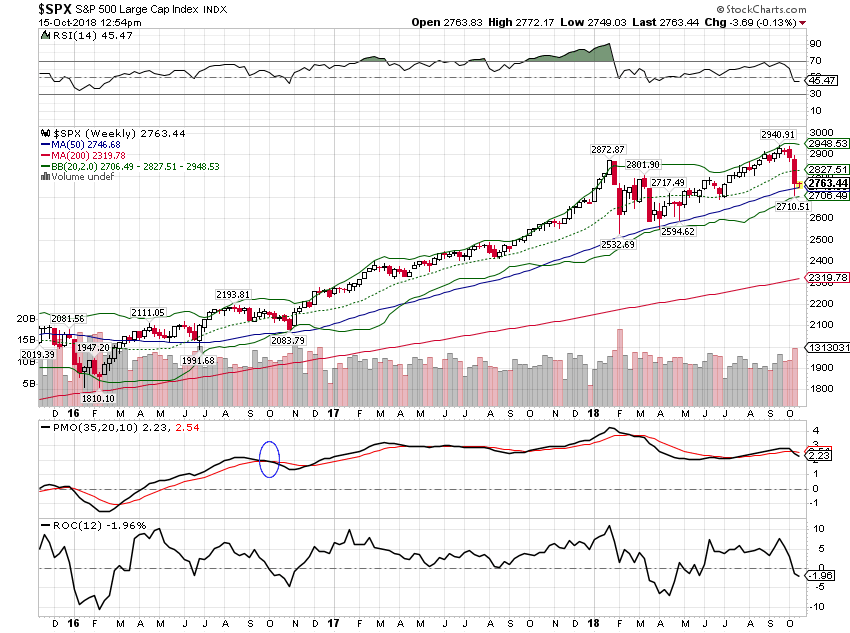

So much for decoupling. US stocks – and specifically the technology sector – finally joined the rest of the world’s stock markets last week. The NASDAQ, which last month was closing in on a 20 handle for the year is now trying to hang onto double digits after giving up a third of its gains in about 6 trading days. The S&P 500 lost half its gain for the year over that same time and is now up less than 5% for the year. The spread between growth and value has shrunk as well, with value outperforming slightly during the correction.

“Correction” is actually stretching the traditional definition. The S&P 500 is down about 6% in October, which is well short of the generally accepted definition of a correction of down 10%. The NASDAQ 100 and the Russell 2000 were down in excess of 10% at their lows last week so I guess that qualifies. But the “downdraft” this month is really just normal market action. It just seems extreme because we’ve had so little of “normal” in recent years that it seems shocking when it returns.

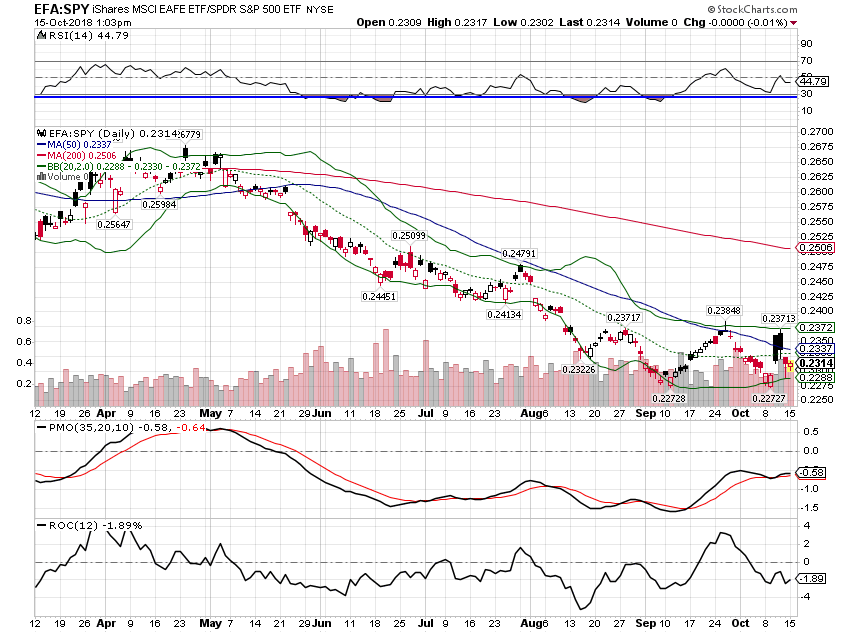

Diversification, which has this year mostly served to make the prudent look foolish, paid some small dividends over the last week. Gold and commodities (DJP) are up early in the quarter, offsetting, somewhat, the decline in stocks. Foreign stocks haven’t offered much haven but at least EAFE performed pretty much in line with US stocks. Emerging market stocks are also holding their own as Latin American stocks, of all things, have actually gained since the beginning of the quarter. Yeah, you can’t predict this stuff.

The question on everyone’s mind these days is what triggered the fall in stock prices. President Trump blames the Federal Reserve and he isn’t alone in doing so but that explanation is wanting in a number of respects. It is certainly logical to acknowledge that a higher discount rate on future earnings should reduce stock prices today but interest rates aren’t the only variable in that equation. Earnings – more specifically, future earnings – matter too and that may be the more important factor in this case.

The fact of rising interest rates is not exactly news these days. Indeed, rising rates is so far in the consensus that my handyman recently told me that rates had nowhere to go but up. His rationale at least made sense, as he believes that the President’s tariffs will be positive for growth or actually “the working man” as he put it, which may or may not amount to the same thing. And like President Trump and his Fed bashing, he apparently isn’t alone in his beliefs about the benefits of taxing imports. The recent rise in the 10-year Treasury note yield has been driven by rising real rates. Inflation expectations have barely budged during a roughly 40 basis point rise in the nominal rate.

The move to 3.25% on the 10-year isn’t much of a surprise; I’ve written several times this year that a move to that level was not out of the question. We did arrive there in rapid fashion though, as nearly half the move up in rates happened over just 2 days. What exactly prompted that move is a matter of great debate right now, although President Trump may be right for all the wrong reasons. Jerome Powell, during an interview with Judy Woodruff on PBS on October 3rd, said:

“The really extremely accommodative low-interest rates that we needed when the economy was quite weak, we don’t need those anymore. They’re not appropriate anymore,” Powell said.

“Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral,” he added. “We may go past neutral, but we’re a long way from neutral at this point, probably.”

Markets today don’t really move on fundamentals; they move on language, on narrative. The Fed and its forward guidance have, in my opinion, been a disaster for markets as investors spend an inordinate amount of time and energy trying to parse Fed speeches, trying to figure out what the Fed thinks and might do. There is an underlying assumption there that the Fed knows what the economy will do in the future and that its actions are of utmost importance to markets and the economy, assumptions that lack only evidence. The Fed has no idea what the economy will do and they have proven it repeatedly. And yes, the Fed is important but not nearly as much as modern investors give it credit for.

Anyway, this quote from Powell moved rates higher immediately and yes stocks moved lower but I still find it a bit hard to connect these dots. The Powell news hit on October 3rd and the stock market didn’t start selling off in earnest until October 10th. Did it really take a week for this news to make it to stock investors? Bond investors reacted immediately but stock investors didn’t notice rising rates for a week?

Here’s some news that did come out on October 10th:

“Ford is having a bad year in 2018. Its stock is down 29%, and the tariffs imposed by President Trump have reportedly cost the company $1 billion, as the company is in the midst of a reorganization. Now, the company is announcing layoffs.

Jim Hackett, Ford’s CEO, is working to engineer a $25.5 billion restructuring of the automaker, hoping to cut costs and remain competitive, the Wall Street Journal reports. But auto sales are down, and one reason is the trade tariffs that Trump has imposed on metals and other goods. According to Bloomberg, Hackett has said they have already cost the company $1 billion in profit and could do “more damage” if the disputes aren’t resolved quickly.”

And:

“Fastenal Co. slumped the most in six months after warning that new U.S. tariffs on China-sourced goods are “directly impacting” customers of the distributor of industrial and construction supplies.

While the company wasn’t hurt much by the first wave of tariffs in the China-U.S. trade war, the outlook changed with duties that went into effect Sept. 24, Chief Executive Officer Daniel Florness said on a call with analysts as Fastenal reported third-quarter earnings Wednesday.”

The Powell quote moved interest rates higher, but as I said the interesting part of that is that it was driven by a rise in real rates, not inflation expectations. In other words, the Powell quote was taken by the bond market as an economic positive – growth is good. Of course, it makes perfect sense why that would be bearish for bonds but why would it be negative for stocks? Wouldn’t an economy growing so fast that the neutral interest rate is still “a long way” away be a positive for growth-sensitive equities?

I think what really moved stocks last week was the Ford and Fastenal news which merely echoed what we’ve been hearing from other companies for a few weeks now. Negative earnings warnings are piling up with Ford and Fastenal just two of the many companies warning about the negative impact of tariffs on their bottom line. And remember, this is only the latest round; the administration has already said it will raise the tariffs to 25% in the new year. The spurt of growth we’ve seen recently is no doubt being aided by anticipation of that hike. We see that in the inventory numbers as well as the trade figures as companies buy ahead of the higher tariffs.

There is already a negative impact on the US economy from the Trump administration tariffs. If the tariff rate on Chinese goods rises to 25% and stays in place – as I think they will – the impact is only going to grow. There may be good geopolitical reasons to keep the pressure on China but we should not pretend that it will be cost-free. Fighting a war – even a cold one – has a cost.

Chairman Powell may believe that interest rates are a long way from neutral but he may also be assuming, as a lot of people are, that the tariffs on China are temporary, a negotiating tactic. If he’s wrong about that, neutral may be a lot closer than he thinks. If the China tariffs prove more permanent – and I don’t see a reason to believe otherwise – the price will be paid, at least partially, in US corporate profit margins.

Yield Curve/Rates

The yield curve has steepened since the last update but the flattening trend is intact on a longer-term basis. The steepening was driven by the rise in the long end, a so-called bear steepener. It is known as a bear steepener because it is usually associated with rising inflation fears but in this case, the rise in the long end was driven primarily by rising growth expectations.

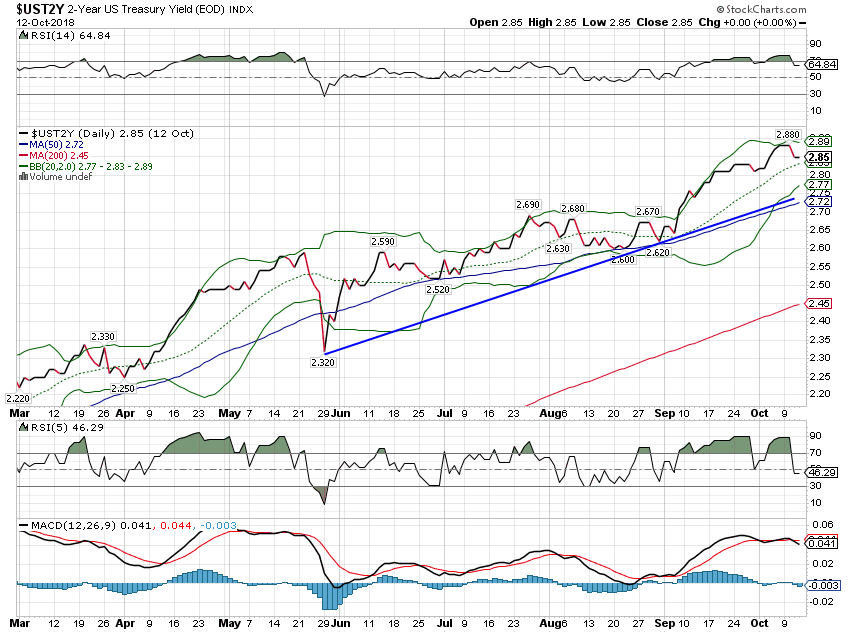

The 2-year note yield also broke out of its recent range as Powell’s comments reinforced expectations for future rate hikes.

The 10-year note yield moved higher and has now completed a move up to the 200-month moving average. That isn’t a technical level so much as a secular marker. Moving averages of that length just aren’t considered by traders or investors. But in this case, the 10-year yield hasn’t traded above that 200-month average since the late 80s and I think that may be significant. In addition, our long-term momentum indicators are at extremes never seen.

I do think the long-term trend for rates may be shifting to an upward bias but just as rates didn’t fall in a straight line, neither will they rise continuously. If tariffs are indeed a drag on growth – and I don’t see how higher taxes can’t be – then rates may have peaked for the cycle. A wild card is the anticipation of higher tariffs on China in January. If we continue to see companies building inventory ahead of that increase, economic activity may stay stronger than otherwise for the rest of the year.

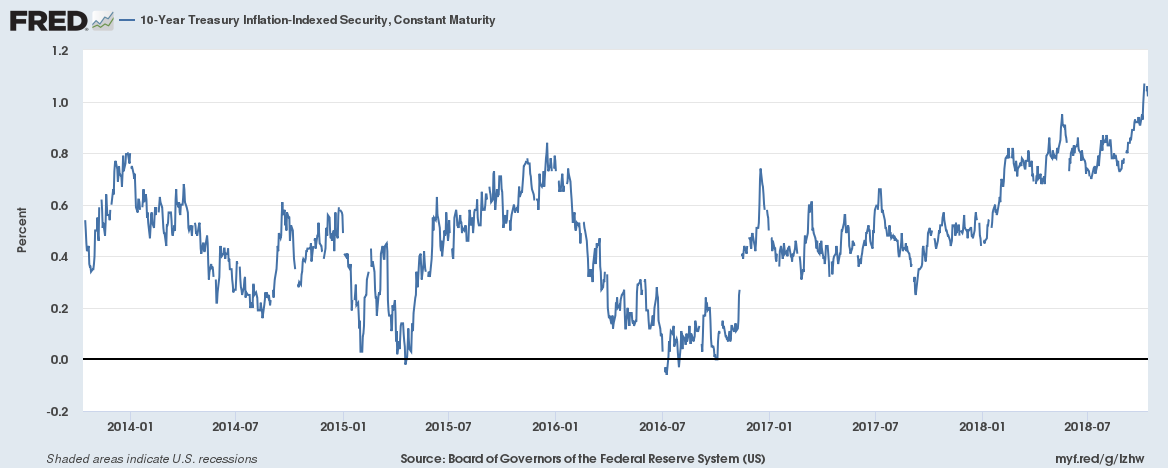

As I said, the rise in long-term rates was driven by a rise in real yields. The 10-year TIPS yield has risen 24 basis points since my last update and is now above 1%. We’ll see how long it holds up there. Earnings season is getting started after a lot of negative warnings and economic data appears to be softening a bit.

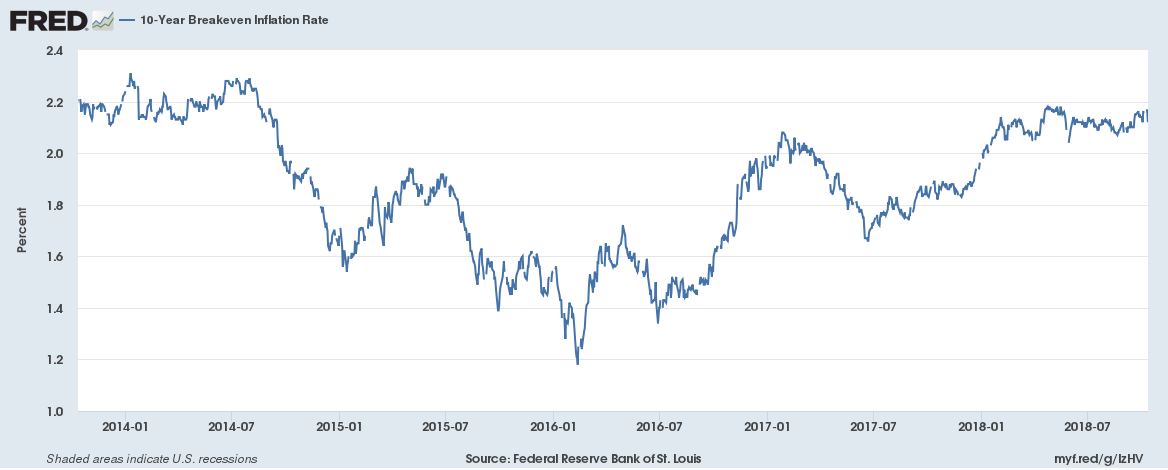

Long-term inflation expectations remain anchored and barely budged during the rate rise. Tariffs are inflationary though so it will be interesting to see how these expectations change in coming months.

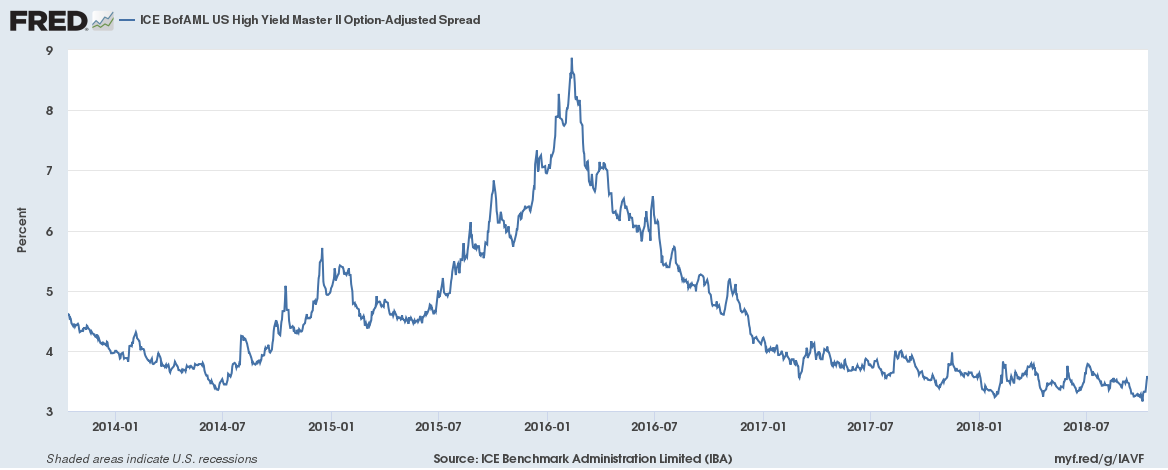

Credit Spreads

Credit spreads are wider since the beginning of September but only by 5 basis points. Spreads narrowed first, hitting new lows for the cycle in early October. The widening since then is, so far, moderate and offers no warning about the economy or stocks.

Valuations

Valuations are still stretched for US stocks despite the small correction. Earnings for the quarter will be positive but after repeated warnings, probably not as good as expected a couple of months ago.

I’ve been seeing a lot of commentary recently that stocks are not that expensive. These commentaries invariably concentrate on some measure of earnings to make their case. The most common is the use of forward earnings estimates (I even saw one recently that looked at forward 2-year earnings estimates). I can’t think of a methodology that is more prone to mistake than relying on Wall Street analyst guesses about the future. They’re always wrong at turning points and usually by a large amount.

The other argument I’ve seen recently is that the Shiller P/E will fall significantly soon because 2008 and 2009 earnings will come out of the calculation. That is certainly true and the ratio will drop if earnings rise and price just remains the same. That assumes, of course, that those estimates about 2019 earnings are correct or at least roughly so. If not, well maybe Shiller P/E won’t fall as much as these “analysts” think. It is also interesting – at least to me – that even if earnings do come in as expected, the ratio only drops to the low 20s. Yes, as these studies point out, that is near the average of the last 20 years. But that period is itself an outlier in my opinion, including as it does the late 90s period when Shiller hit its highest level ever.

I would also point out that the entire period since the mid-80s is one of falling interest rates and as I said above, that period may well be on its last legs. Valuing stocks in a long-term rising rate environment is something with which few have any experience at all. I suspect predicting the stock market in that environment will not be as easy as putting an ever higher multiple – due to a lower discount rate – on earnings estimates that rise every year.

One last note on valuation and attempts to characterize this market as cheaper than it really is. There are other measures of valuation which will not be relieved by the calendar as Shiller may be. Market cap/GDP and price/sales ratios are still at or near record highs.

Momentum

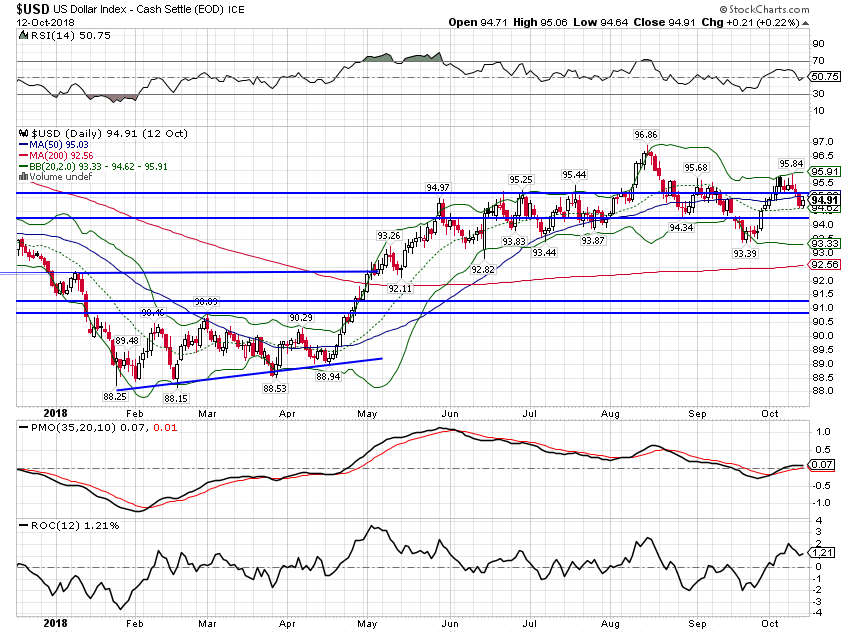

The US dollar index is back in the range that has prevailed since the spring surge. The narrative in markets for most of this year is that the US economy is accelerating and doing much better than the rest of the world. As I’ve said a number of times there is some evidence to support that but it isn’t as clear-cut as most seem to think. Growth and growth expectations have risen in the US, which we can see through the economic statistics and interest rates. But the change is actually rather mild with the year-over-year change in GDP still in the high 2% range. Yes, that is better than the low to mid 2% range that prevailed previously but it isn’t a huge change. We appear to be growing just slightly above trend – which is maybe a bit surprising given the magnitude of the fiscal push. But that’s the truth, and the move in the dollar is right in sync with that conclusion. It has moved up this year but the change is minor and has not changed the longer-term downward momentum.

Furthermore, shorter momentum now looks to be turning lower despite the recent rise in rates. Dollar bulls might want to think about why the dollar hasn’t responded as one would expect.

Obviously, short-term momentum for US stocks has shifted. And while long-term momentum is still positive, intermediate measures have joined short-term in pointing south. Weekly momentum peaked with the early year surge and while stocks made new highs, momentum did not. The market seems to be trying to hold these levels and make another surge but the effort so far is rather anemic. This market has been amazingly resilient though so maybe it will get off the canvas one more time. If not, monthly momentum is not far from turning negative as well.

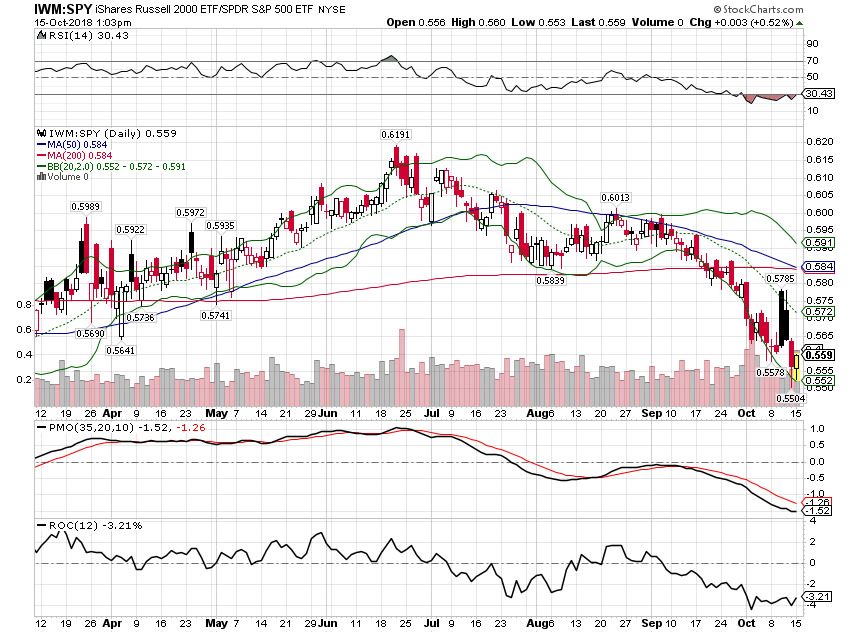

Small caps are once again leading – on the downside.

As I said, foreign markets managed to perform in line with the US since early September. That is a victory of sorts, I suppose, but it will probably take more dollar weakness to see any outperformance. And even that won’t help if the US economy really starts to look winded.

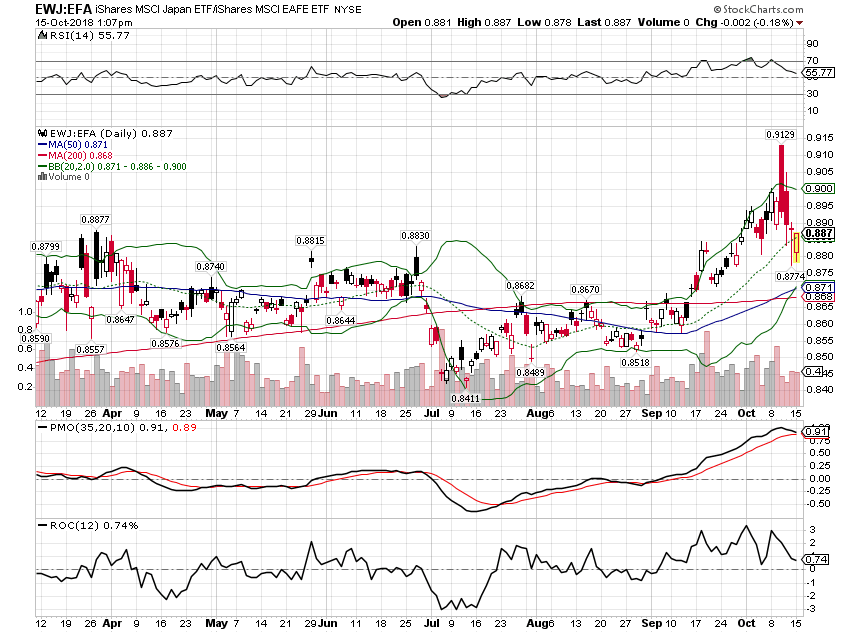

The uptrend of Japanese stocks versus the wider EAFE continues with short-term measures now matching longer-term ones.

The underperformance of EM versus EAFE appears to be running out of steam.

Maybe the best evidence of that is the outperformance of Latin American shares. A lot of this has to do with the upcoming election in Brazil but other countries have recently come off their lows as well. As for Brazil, even if the market’s preferred candidate wins – and that looks likely – the road ahead looks decidedly bumpy. Reality will likely set in after the election when campaign promises turn out to be easier to make than implement.

Another canary in the coal mine may be EM local currency bonds. EM stocks are still struggling but bonds appear to have already made a bottom. EM local currency bonds outperformed during the recent correction.

Diversification did make a bit of a comeback recently. With the dollar struggling, commodities turned higher, posting a positive performance in September and October even as stocks turned south.

Holding some gold in reserve also paid some dividends.

The shift in momentum from stocks to commodities, which I’ve been writing about for several years now, continues. With commodities up and stocks down recently, the ratio has surged. This also fits well with the idea that we are in the process of a secular shift from declining to rising rates. If US economic growth moderates – or worse – because of the tariffs, gold will probably outperform the general commodity indexes. That is the long-term trend in any case and it may be just now starting to reassert itself.

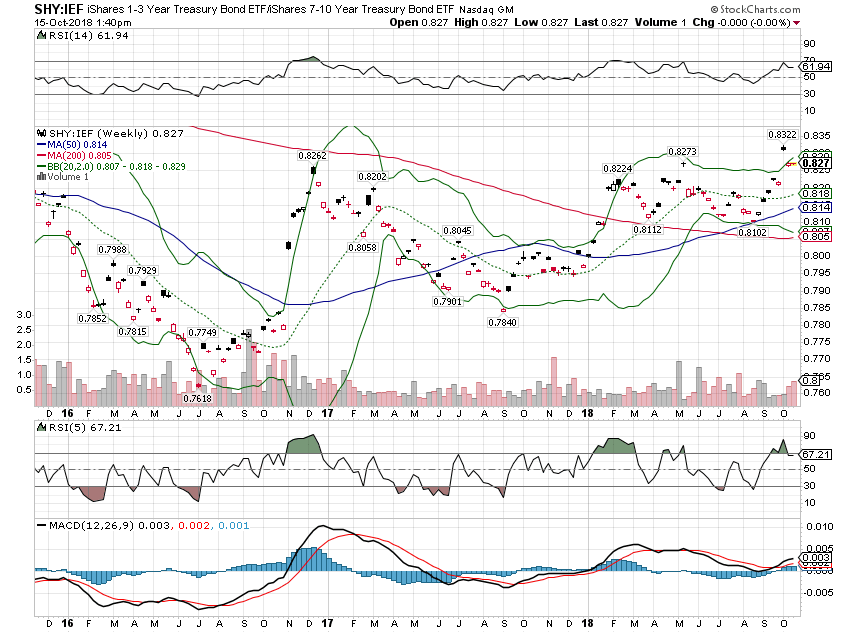

Bonds have obviously performed poorly recently with rates rising. While emerging market bonds may be outperforming, they aren’t really appropriate for more conservative investors. But short-term rates have risen enough now to make them at least somewhat appealing.

While I think long-term rates are probably peaking here, I can’t be sure. For now, short duration bonds are outperforming.

And that highlights the one change to the portfolio this month; a shift of some of our longer duration bond allocation to shorter-term. I am shifting half the position in IEF (7-10 year Treasury) to SHY (1-3 year Treasury). As I said, I can’t be sure that rates have actually peaked and with commodities starting to outperform the odds of me being wrong are probably higher than I’d like to admit. The conservative move here is to reduce duration until we have more support for the peaking rates thesis.

This has been a tough year for diversified investors. Heck, the last decade hasn’t been kind to anyone trying to invest using the traditional risk reduction tools available to the prudent investor. It has been a period dominated by US stocks, interrupted only briefly last year. That doesn’t mean that diversification isn’t necessary or prudent still. It is, and the last few weeks of stock market correction have proven that again. Yes, bonds and stocks have been more correlated lately but when stocks really started to get hit hard last week, bonds did what they are supposed to do for a balanced investor. They moved higher, offsetting some of the loss in stocks with the 10-year yield dropping over 10 basis points from its high in a matter of days. Commodities and gold have also worked to offset the weakness in stocks. Even REITs outperformed in the most intense part of the equity selling. So yes, diversification still works as advertised.

I believe there are big changes afoot in markets and the global economy. Some of that is related to the Trump administration and their pursuit of mercantilist trade policies. Some of it is more related to monetary policy and more still from the several decade-long build-up of debt worldwide. Changes to long-term trends are not easy to digest and they can take considerable time for investors to fully accept. During that period, volatility will likely be the rule rather than the exception. Diversification hasn’t worked in the age of the central banker but their control is an illusion. The only real protection for an investor is the same as it has always been – don’t put all your eggs in one basket.

Stay In Touch