True to form, whoever holds the government it is for them the best economy ever. It doesn’t matter political parties or otherwise affiliations. The rhetoric has become so unhinged that in the US former President Obama is trying to take credit for current President Trump’s economic “miracle” – that doesn’t actually exist.

In India, the Modi government is following the pattern. A prominent member of the Prime Minister’s Economic Advisory Council, Surjit Bhalla, said today that the last four years under that government have been the “best years” for the Indian economy. If he so chooses, Bhalla would fit right in inside the DC beltway.

If you look at any macro parameters then these (Modi government’s four years) are the best four years of the Indian economy…so without a doubt, the macro performance is better.

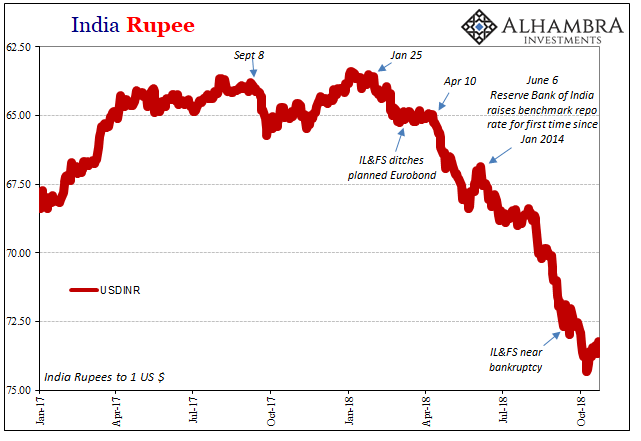

Unlike current American politics, however, Indian officials are being stung by the sudden appearance of an unmistakable banking crisis. Unable to yet get a handle on it, Bhalla would go on to also admit, “We have the NPA [non-performing assets] crisis that by all account is a lot worse now as a share of GDP or as a share of loans.”

Who is to blame for this? The central bank, of course, channeling recent official sentiment on this side of the world. In the government’s considered opinion it has been the high rates and “tight monetary policy” pursued by the Reserve Bank of India’s Monetary Policy Committee (their version of the FOMC) that has somehow restrained economic growth during the “best four years of the Indian economy.”

Things are awesome, but if they aren’t it’s definitely someone else’s fault.

Unlike 2013-15, India is punching far above its weight on the scale of marginal importance. It’s not that the near failure and bailout of IL&FS, India’s big shadow eurodollar borrower, threatens the world with 2011, European-style contagion. The banking troubles on the subcontinent will likely only trouble Indians.

But that matters more than it may seem. The eurodollar tide that began destroying the perceived fruits of decades of globalization is still swallowing up national economies eleven years later. Just not all at once. The US and Europe were hit in 2008, and those haven’t recovered (sorry, Mr. President; either of you). Emerging markets especially those in Asia were expected to at least pick up some of the slack, to keep open in part the lines of opportunity for this worldwide economy.

And then 2014 happened, the spillover into 2015 becoming a major hit to those very same economies. It became increasingly clear, at least to those outside the Economics profession, that China in particular would no longer be able to lead the world carrying the bulk of the load back to shared prosperity.

While officials went on and on about globally synchronized growth in 2017, in truth there was very little growth. That was, in the end, the whole problem (lack of actual opportunity). What that meant was, in deference to Modi and Bhalla, India’s economy became the only major performing anywhere close to legitimately. Despite the currency crisis of 2013-15, India managed fairly well.

But if this latest outbreak of eurodollar trouble now takes out India, who around the world would that leave for anyone anywhere to pin their hopes on?

The US and Europe are out; China, too. If India suffers the tidal wave of deflation as one of the last untouched inland economic outposts, then the worldwide economic “L” will truly be global. It would finally be synchronized, but in every way abhorrent to the original idea.

This is why, I believe, India matters in 2018 whereas it might’ve skirted along under the surface three years ago. People rightly focused on China in 2015 since the Indian economy remained largely stable. If India gets the worst of the eurodollar, too, then there is nothing left but risk.

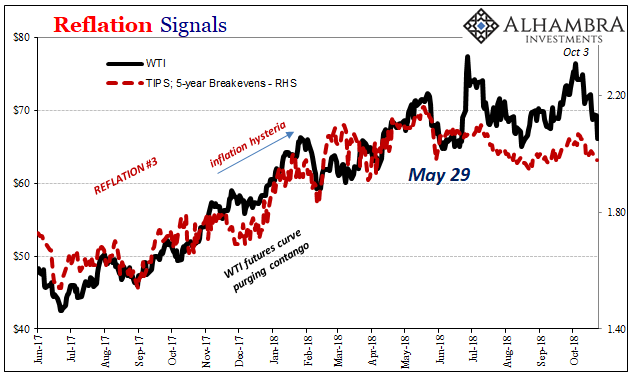

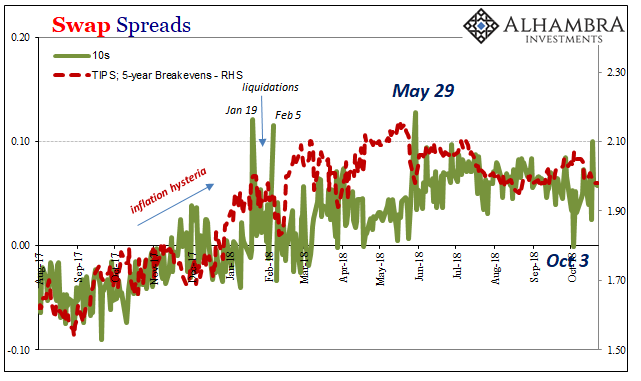

I also think that’s what hit global markets on October 3. The IL&FS fiasco forced Indian authorities, or financial agents acting on their behalf, to pony up and subsidize that country’s more limited “dollar short.” That was the day the UST market experienced its last “big” BOND ROUT!!!!, the one that took the 10s yield to its highest since 2011. Rising risk surely spread to other susceptible eurodollar participants.

Western attention fixed on Jay Powell and so-called rate hikes, but the aftermath of October 3 has been otherwise. I wrote back on October 5:

In other words, India’s was having (big) dollar problems before the selloff in UST’s. What do banks and central banks do when faced with a local or systemic dollar shortage, having always to feed their dollar short?

They sell UST’s.

Since then, there has been a lot more liquidation-type behavior even in stock markets. Inflation expectations here in the US have fallen along with nominal UST yields. And the price of crude oil.

Convention is gearing up for another “supply glut” in oil (OPEC pumping this time), but like 2015 it is more likely the oil patch fears demand. Without China and now with perhaps India at great risk, where will growth actually come from?

We are left more and more confronting only risk, and by that we mean the absence of realistic economic opportunity. It falls out from under these very crucial places. Jay Powell and his comrades at the FOMC may not pay any attention to India’s MPC but they should. Urjit Patel, the Governor of the Reserve Bank of India, already called him out once this year. Though it was for the wrong reasons, it’s always the wrong reasons with central bankers, ultimately what mattered was gathering distress about India.

When the last hope for stable, genuine economic growth goes up against the eurodollar nobody is going to win. There may be nothing left afterward. Markets are catching on, especially after May 29, some are maybe even fearful. With good reason.

Stay In Touch