Jerome Powell may be hawkish, relatively speaking, but his case rests on one data point alone. There is nothing other than the unemployment right now indicating he’s got the right forecast in mind. This wasn’t true just months ago. At the end of 2017 and for a few months in 2018, inflation was moving upward and above targets and benchmarks. Inflation expectations, especially in a recalcitrant Treasury market, were pushing higher, too.

These things were supposed to be consistent and related. Orthodox theory posits that a tight labor market means companies have to compete for workers. In turn, they have to raise prices to pay for the raises they’ll have to give new workers and eventually existing ones. Consumers as workers can afford the higher prices with wages matching the underlying condition in the labor market.

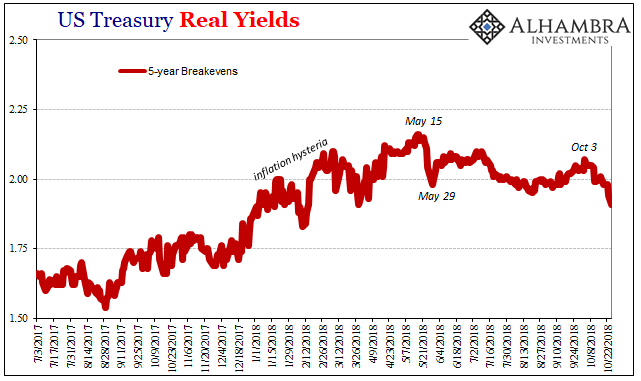

The unemployment rate now firmly entrenched below 4% seems to suggest an extremely tight labor market. Therefore, rising inflation at the end of last year as the unemployment number inched lower and lower triggered the inflation hysteria; markets for a time wondering if the Fed might be right about all this and so much commentary seizing on it with unwarranted certainty.

That’s all gone now. The unemployment is still behaving as it was, only consumer prices weren’t accelerating. Not really. Outside of oil and energy, there wasn’t ever anything to indicate the kind of broad-based pressure along the lines of the tight labor market theory.

In truth, we already knew as much given how wages have lagged. It was always a long shot, but for a few months the idea was mildly plausible. Desperately seeking vindication after more than a decade without success, that small window was hyped as the most conclusive evidence ever assembled. True hysteria.

The GDP reports include, obviously, data on prices. There are deflators and indices for all the components; that’s how you get from nominal GDP to real GDP in whole and in parts.

There is nothing but disappointment in today’s report for the chicken hawks.

The price index for overall GDP dropped considerably. Hitting 3.3% (Q/Q, annual rate) in Q2, the highest since 2007, the volatile index rose just 1.3% in Q3.

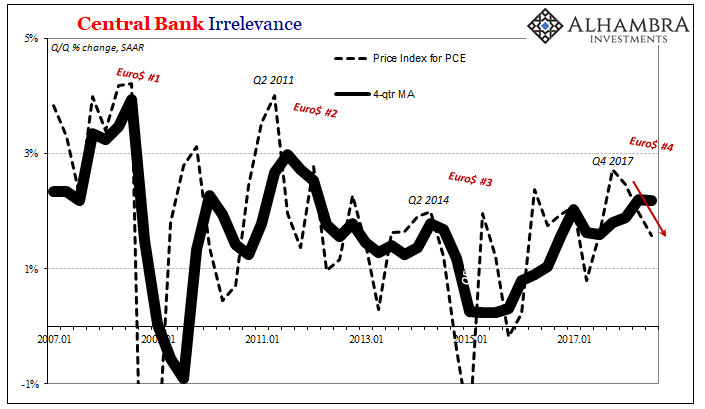

For Personal Consumption Expenditures, which is what Fed officials pay attention to, consumer price inflation has been decelerating since inflation hysteria in that last quarter of 2017. Getting up as high as 2.7% during those particular three months, it has been lower at each interval this year. As of Q3, the measured price gain is under 2% again, pegged at just 1.6%.

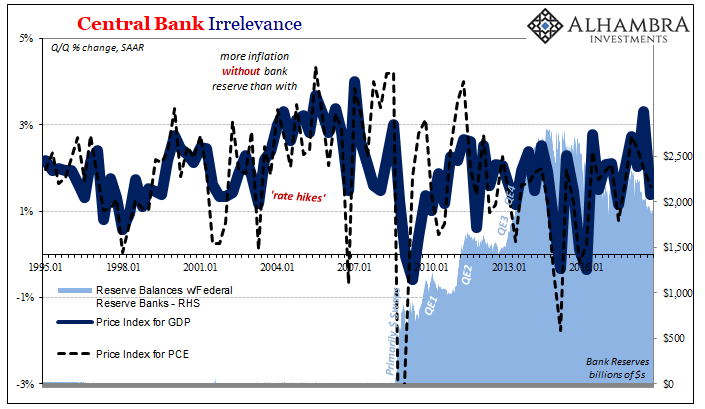

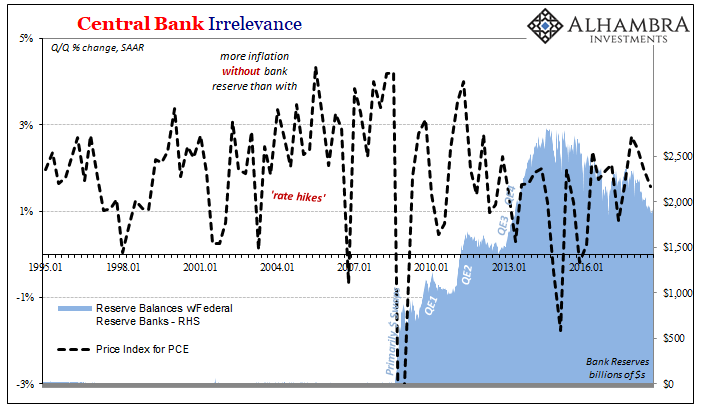

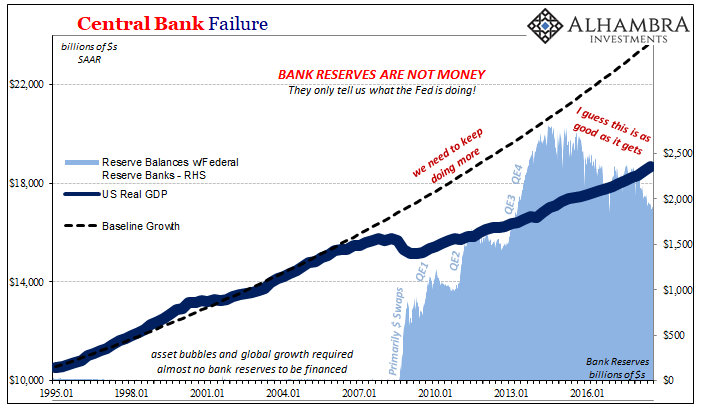

Analyzed against the backdrop of monetary policy, it’s as if what the Federal Reserve does or doesn’t do doesn’t matter. There was far more consumer price inflation when there were practically no bank reserves (the byproduct of LSAP’s or other programs like foreign dollar swaps expanding the central bank balance sheet). It was also true of the mid-2000’s rate hikes.

For four years now, the FOMC has been counting on the unemployment rate to indicate the point which will trigger the wage process to finally change all that. It didn’t happen last year, and more and more it appears as if this year it won’t, either. In fact, the longer 2018 drags on the likelihood of the opposite case gains at Powell and the FOMC’s expense.

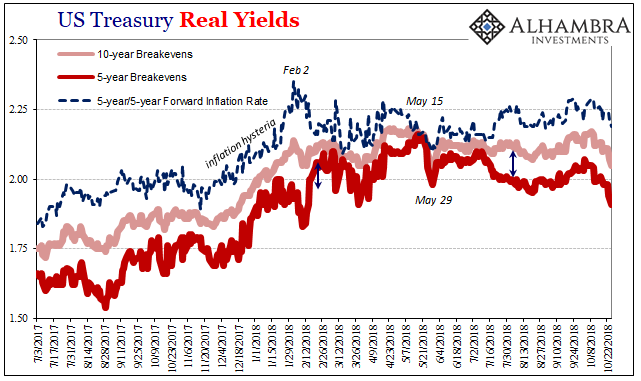

That’s what markets are saying right now. Having been reminded of what central bankers don’t consider, meaning actual monetary conditions, you can clearly see the change in mindset. Up until the collateral call in mid-May, what the Fed later attempted to dismiss as the “strong worldwide demand for safe assets”, inflation hysteria has been turned back into baseline skepticism.

Today’s GDP estimates provide more ammunition for those doubts, not the supposed boom.

Stay In Touch