There was nothing really shocking about China’s monthly economic statistics for October 2018. The Big 3, Industrial Production, Retail Sales, and Fixed Asset Investment, all continue along in the same way. The Chinese economy is not crashing, it may be slowing, but most of all there isn’t any more upside. It’s the last one that is important.

As such, Communist officials are driving toward another mandate, somewhat in a panic, where the goal is not really growth. In a sense, they seem intent on managing the decline as best as they might, realizing it’s not going to get better anytime soon (“L”) but not wanting the downward slope to accelerate too far toward an impossible-to-control scenario (the so-called hard landing).

I’m not sure it’s possible, though at this point what other choice may they have realistically available?

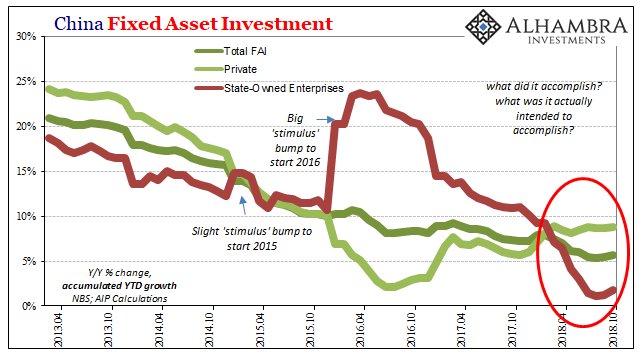

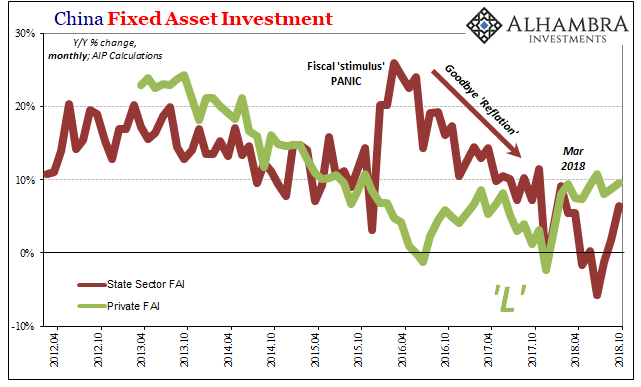

To that end, we have seen in the last few months a restart in State-owned FAI of sorts. It’s not nearly the “stimulus” program that was unleashed in early 2016 with the same intent – to stabilize, if possible, China’s economic decline. Public FAI had been contracting earlier in the year I believe on the premise Economists knew what they were talking about with regard to globally synchronized growth.

In other words, a worldwide upturn could have provided Chinese authorities the chance to remove some of the waste and excesses always associated with this kind of economic behavior. CNY’s “miraculous” rebirth in 2017 along with often sky-high sentiment gave them a modest tailwind to do it.

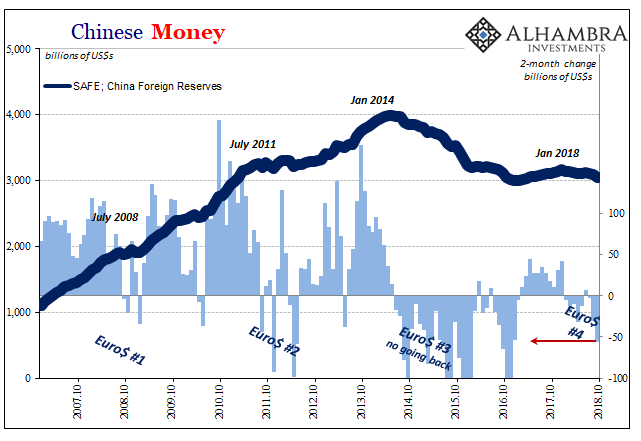

With CNY now right around 7.0 to the dollar, which is very much a line in the sand (so far), there’s no margin in the monetary system nor the economy. State-owned FAI has rebounded in the last two months just as things got to their worst in currency and money. On an accumulated basis, State-owned FAI has improved from 1.1% (YTD) in August to now 1.8% in October.

On a monthly basis, FAI through public companies was contracting at a near 6% year-over-year rate in July but expanded by a 6.4% rate in October. These are not huge changes, State-owned FAI growth in October 2017 was a weak 7.2%, though they do seem to indicate some sensitivity to China’s precarious economic state consistent with other policy measures (expanded use of reserves to stabilize CNY, for one) being added and altered concurrently.

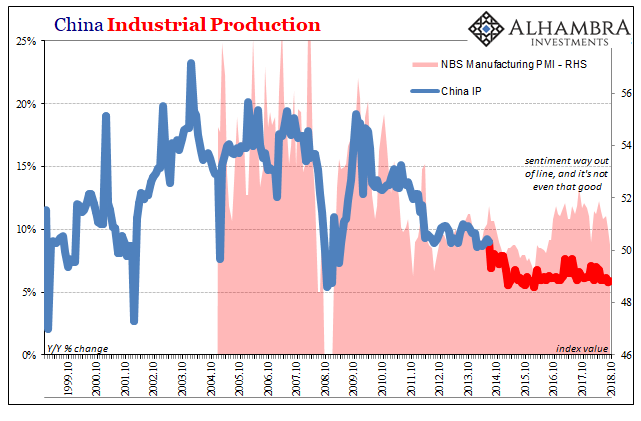

Industrial Production was estimated to have grown at 5.9% year-over-year in October, up slightly from 5.8% in September. It was the fifth month of growth at 6.1% or less. China has not posted two consecutive IP figures below 6% since the trough of the last downturn in December 2015 through February 2016 (January and February statistics are always combined into a single number due to the Golden Week holiday skews).

In fact, the current low levels of IP rate at almost exactly the same levels as the last half of 2015. Not exactly encouraging results. Again, China’s economy doesn’t appear to be crashing, it does appear to be slowing, and therefore there can’t be much if any upside indicated here.

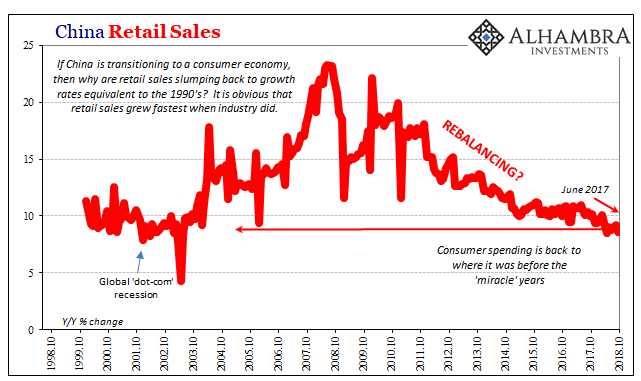

Retail Sales growth has clearly stalled over the past year, year and a half, rising just 8.6% in October. That’s only a tenth of a percent better than May 2018 which was the lowest gain since 2003. Consumer spending in China is supposed to be the balance to the country’s industrial/investment decline. To some extent it has been, but that overall has been exaggerated greatly for years.

With retail sales now certainly resuming a weakened trend, there’s renewed pressure on authorities to try and stabilize the decline.

In short, there are too many things moving in the wrong direction this year when compared to last year. As a quite understandable response, Chinese authorities are seeking often desperately to counteract them though limited to basically more of the same things that haven’t really worked (unless your standard for success is to buy time, but buy time for what?) This, I think, explains the utter lack of enthusiasm about these measures, while also indicating just how little choice there is available for the government.

They say that Father Time is undefeated, and that’s true, but the eurodollar system is giving the old guy a run for his money. The world’s money. It created the Chinese’ miracle on the way up, and it has since taken it away on the way down. That direction is being continued.

The only difference in 2018 as opposed to, say, 2013, is who knows it. Half a decade ago, many were still betting on a return to normalcy with Chinese economic supremacy at the forefront. Even some authorities as late as 2014 were arguing for conventional.

Not so much anymore.

Stay In Touch