I, for one, am sick of still writing about 2017’s tropical season. It’s been well more than a year and yet we are just now finally moving past them. It would’ve been healthier and more honest had there been more appreciation for what they really were going to do for/to the US economy.

Without any more artificial interventions left, the US system really begins to look shaky again. It is surprising to far too many maybe otherwise rational people. In the manufacturing business, Harvey and Irma were a boom as was the looming trade war with China. For certain discrete months, it was good to be in the goods trade and some in it began expecting big things.

You could tell it was going to be temporary, not that anyone would have known it from mainstream coverage. Last year’s Gulf Coast storms were a gift in those terms, a temporary reprieve that would’ve made Keynes extraordinarily proud. I noted in early October last year how the tone had already shifted after a pretty dismal summer:

It’s a bit weird, however, in light of the past few years where winter storms were a cause for dismissing weakness that was now in favor of summer hurricanes that might somehow fix all the labor problems that weren’t supposed to have existed.

We reiterated the expectation several times; one from February 2018:

And as we’ve stated from the moment of Harvey’s strike, the broken windows fallacy will be proved yet again. Though a temporary boost, at some point that will fade and demand should adjust back to the prior pre-storm baseline (which was slightly lower imports and demand) if not worse because someone will have to pay for all those literal broken (car) windows.

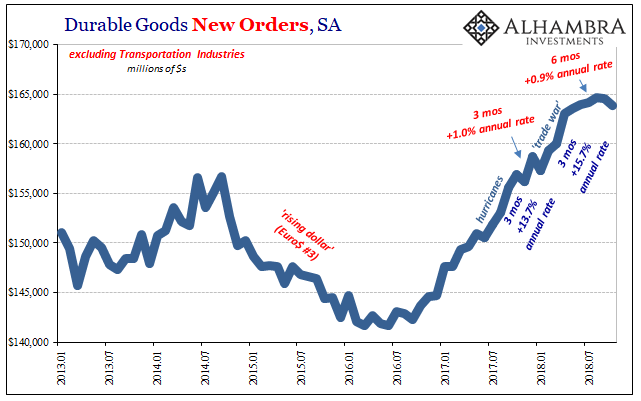

The payback started somewhere around April or May depending on the particular data set. For something like durable goods, new figures for October 2018 released today, April was the last of it. Seasonally-adjusted, new orders for durable goods have basically flatlined for now six straight months. Half a year and less than 0.5% growth, a very different annual rate of just 0.9%.

That’s flirting with an economic stall.

September’s estimated was revised lower, leaving the series to have contracted in each of the past two months.

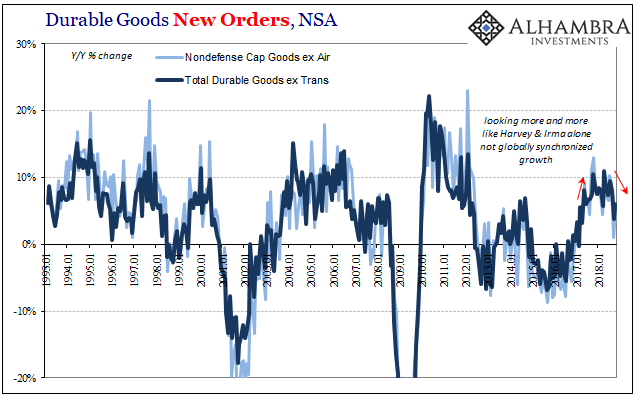

The pattern is making its way into the annual figures, obviously. New orders were up by a revised 3.8% year-over-year (unadjusted) in September and just 6.0% in October. It was the lowest two-month average since, unsurprisingly, the month Harvey struck. The 6-month average is likewise the smallest since last August.

Capital goods orders rose 3.3% and 5.4% September and October, respectively. Those were the slowest two months since April 2017. Again, comparisons are the worst since before the hurricanes.

This actually presents us with a bit of a counterintuitive challenge. With the statistical shoe now on the other foot, how much of the weakening in durable goods is “real” perhaps related to the forming global slowdown already striking in many other places? How much is simple reversion to the same reduced post-2015 baseline as the numbers normalize past 2017’s irrational euphoria?

The answer doesn’t have to be mutually exclusive of those two options, either. I suspect we won’t know for sure for several more months still, particularly if we start seeing a proliferation of minus signs, even small negatives, to end 2018 on an even more sour note. Unexpected it won’t be.

There was no economic boom, not a real one, anyway. Kudos to Janet Yellen, though. She can just blame Jay Powell for screwing up her final economic gift and everyone will believe it. It doesn’t matter that the current “rate hike” trend began all the way back in December 2016 and at 2% isn’t anything like a burden. I expect this will become a common theme regardless long after people have forgotten all about Harvey and Irma.

Stay In Touch