The FOMC had voted to taper the final purchasing levels of its third and fourth QE programs at the end of October 2014. Just two days later, the Bank of Japan’s policy committee would vote to expand theirs (already with the extra “Q”). The diverging outlooks punctuated a period of high uncertainty.

No more so than global asset markets. When Federal Reserve Chairman Janet Yellen appeared in front of the cameras the following policy meeting in December 2014, she did so with WTI in total freefall. Whatever anyone tried to make of it, the oil crash was rightly unnerving. These things just don’t happen like that, not during normal times.

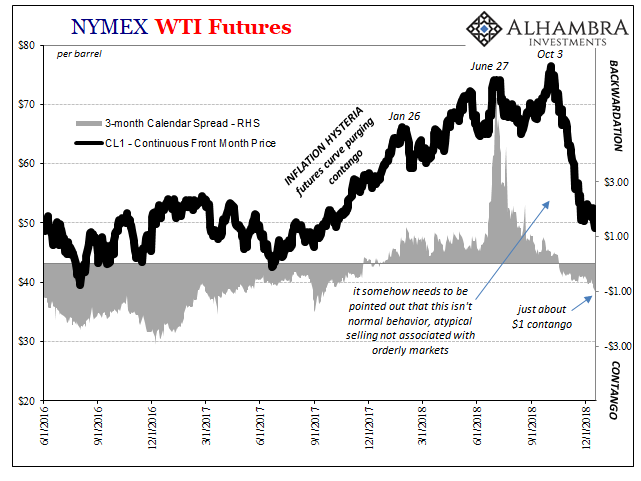

On December 18, the front month oil contract fell below $55 for the first time since 2009, the big one five years before. The 3-month calendar spread, that is the difference between the first contract on the board (effectively the spot price) and the one three months later had just surpassed $1 in contango (a higher front month price). Functioning oil markets in balance fundamentally, as would be the case with economic growth picking up, should have meant a backwardated oil futures curve not contango.

Yellen was undeterred, at least in public. We won’t know what she might’ve said in private discussions until the transcripts for 2014 are released in January or February 2020. The Chairman reassured the public anyway.

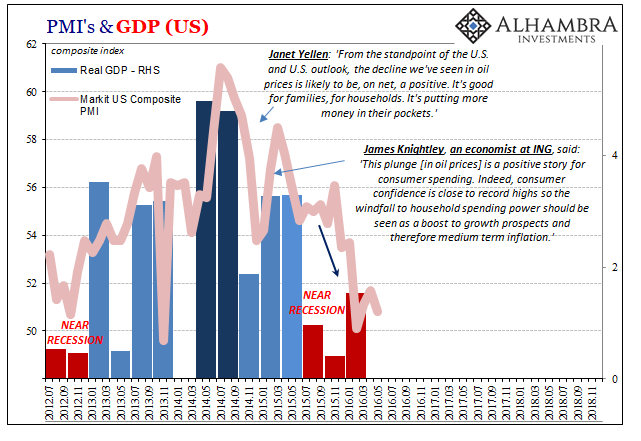

From the standpoint of the U.S. and U.S. outlook, the decline we’ve seen in oil prices is likely to be, on net, a positive. It’s good for families, for households. It’s putting more money in their pockets.

This became the major talking point which would eventually define the galling cluelessness. The big, scary thing out there causing all this financial uncertainty, the oil crash, was really just this huge, misunderstood boost to an already great economic situation? Throughout early 2015, this apologue was repeated over and over and over as if it was, like the unemployment rate, some witch’s enchantment intended to ward off the evil economic spirits.

Here’s but one example from a few months after Yellen in February 2015:

James Knightley, an economist at ING, said: “This plunge [in oil prices] is a positive story for consumer spending. Indeed, consumer confidence is close to record highs so the windfall to household spending power should be seen as a boost to growth prospects and therefore medium term inflation.”

I don’t know if Jay Powell was paying much attention back then, even if he was it’s a good bet the Fed’s current Chairman will resurrect the canard this week. After all, the oil market is returned to practically the same state already. WTI fell below $50 today for the first time in over a year, but more so it’s the way in which it has that raises, or should, alarms.

This isn’t a normal selloff, the usual back and forth that happens in every market. No typical “volatility”, this is another paradigm shift of the same variety back toward global downturn. The 3-month calendar spread for WTI, as it happens, settles just shy of $1 contango today. The ghosts of late 2014 are being set upon Jay Powell as he attempts to make the same ultimately wrong prediction as his predecessor.

The eurodollar cycle merely repeats, often in very close fashion.

He will have to say something positive, therefore “an oil crash is like a tax cut” will probably make an appearance.

The problem with the claim is not really about oil at all, a fact even the most optimistic Economist or policymaker (redundant) should know. What worries anyone in this situation is why oil is crashing rather than descending gracefully. It’s “overseas turmoil” that cuts a little too close to home. Contango versus backwardation isn’t just simple math.

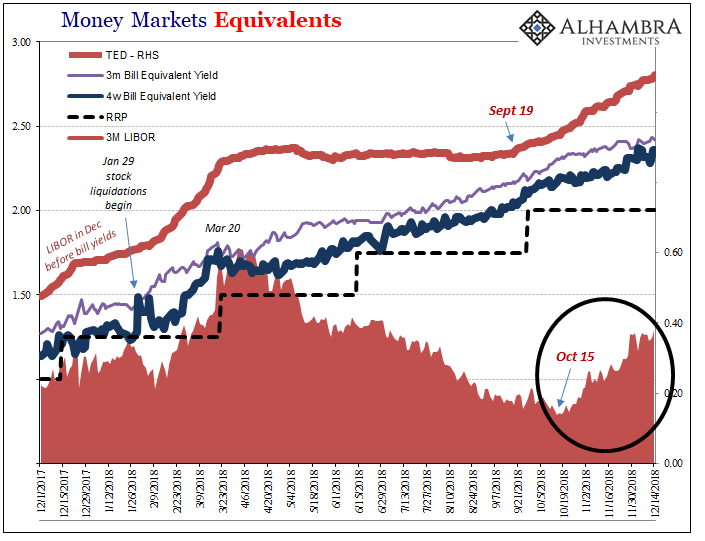

It’s the correlation with all the other stuff. Sure, the FOMC claims it is raising rates but money markets aren’t acting on Federal Reserve policy. LIBOR keeps going up even though everything that would have suggested Jay Powell was right about the economy is moving the other way. In other words, inflation and economic expectations are dropping (rapidly) which would be consistent with the downturn in 2015 (therefore “lower for longer”) not the economic acceleration first Yellen and now Powell has been counting on.

Once again, rate hikes in name only (RHINO) just like the very first that eventually happened in December 2015. The basis for them has rapidly disappeared into what is starting to look like the worst case – self-reinforcing widespread pullback.

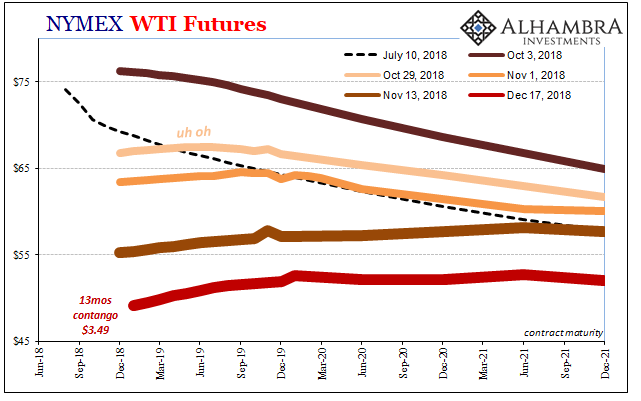

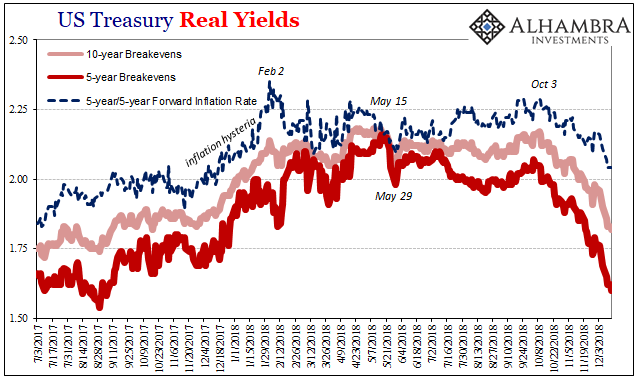

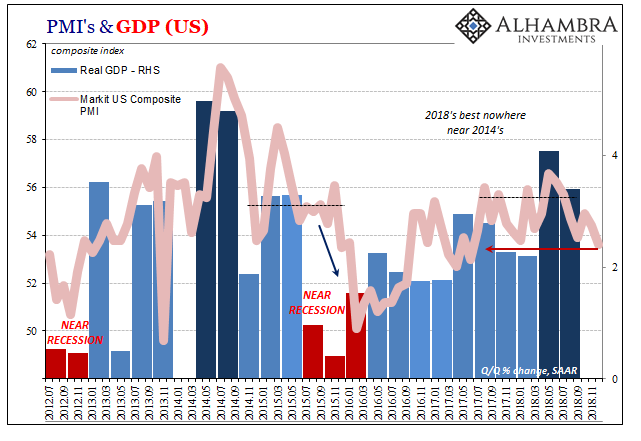

As oil goes obviously that contributes a lot to financial expectations about inflation. Breakevens have absolutely collapsed with WTI in contango. The market for much of 2018 was wondering if the balance between “overseas turmoil” and the US unemployment rate might eventually fall in Powell’s favor. For many, a sub-4% labor market was compelling, though never too compelling.

Then came May 29.

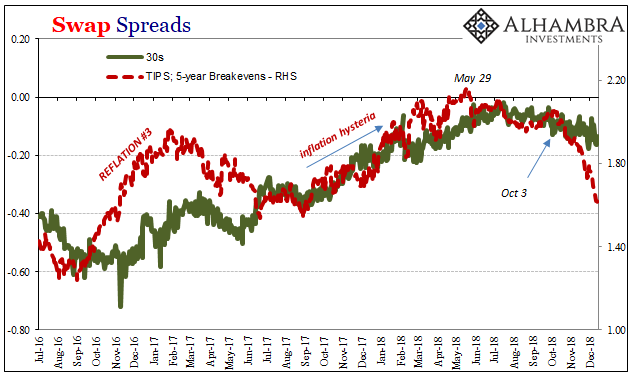

Now? There’s not even an argument anymore. The unemployment rate has been totally disregarded, just as it was in 2015. These kinds of settling subtle shifts spillover. Inflation expectations, for one, play a central role in lots of different processes and markets. Interest rate swaps take many cues from TIPS, and therefore pass along the oil crash into the deep shadows of global money – and then pass that illiquidity back into WTI futures trading.

And as they do, money dealers pull back even more (indicated by compressing more negative swap spreads) leading to more general market liquidations, depressing inflation and economic expectations that much more, and so on and so on. Self-reinforcing, the unwanted sinking toward the deeper red (below).

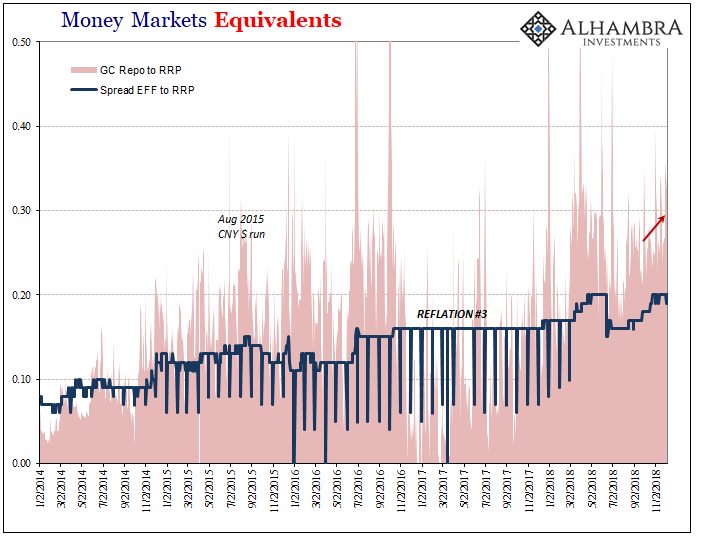

We see it in a lot of different places, not just IRS or LIBOR. The repo rate, for example, has gotten as much out of hand, too; also inconsistent with Powell and indicating back to RHINO’s more than anything. The GC repo rate UST collateral in today’s session jumped by nearly 11 bps, MBS GC a little more than 11 bps, with stock liquidations seemingly in agreement with that shown non-policy global money tightening.

It is the kind of thing you expect alarmingly consistent with an oil crash that doesn’t, cannot lead the economy to a place where “It’s good for families.” This isn’t likely to be good for anyone, even central bankers (eventually).

Like Yellen, Powell is now trapped as a bystander. Eventually, the FOMC would vote to raise the federal funds rate that one time in 2015 because they almost had to. The Committee had been claiming for so long how great things were becoming (and how lower oil prices would make everything even better), for them to hold off beyond December 2015 would’ve just made a bad situation that much worse; confirming that mainstream expectations were all wrong.

This week, Federal Reserve policymakers are confronting pretty much the same suite of bad choices. They’ve already to face another oil crash front and center. I expect they’ll try to use it, though this time around some people will remember what palpable nonsense is commonplace during desperate times. In the end, both the Fed and BoJ though they seemingly did opposite things four years ago they ended up in the same fit of distress anyway.

Stay In Touch