I’ve never actually seen a chicken running around with its head cut off, though I suppose there’s a video of it somewhere on YouTube I could access. Neither you or I, however, need to partake of the actual gruesome spectacle. We need only monitor the behavior of European monetary officials in order to gain a perfect sense of what it must be like.

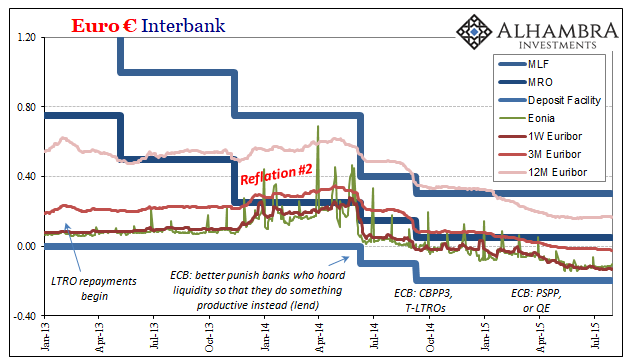

Six years ago, back in January 2013 European banks began to repay their LTRO balances. These were programs initiated in the very dark days of December 2011 when the global banking system “unexpectedly” teetered on the verge of renewed panic. The ECB offered tremendous “liquidity” in the form of term euro financing, the first a three-year allotment settled on December 22, 2011, followed by a second also for three years settled on March 1, 2012.

The initial gate for eligible repayment was set for January 30, 2013. Days beforehand, the ECB announced 278 banks were going to retire €137.2 billion, or about 30% of what was outstanding. This was taken as a very good sign that the LTRO’s had worked. European banks were so confident in the recovery that there were perfectly willing to give up on the ECB’s “cheap money.”

Speaking for this conventional view, one analyst claimed:

“If euro-zone banks are willing to repay borrowed funds from the peak of the financial aspect part of the crisis, then it is assumed that the interbank market has to be healthy,” said Christopher Vecchio, currency analyst at DailyFX.

The key word: assumed.

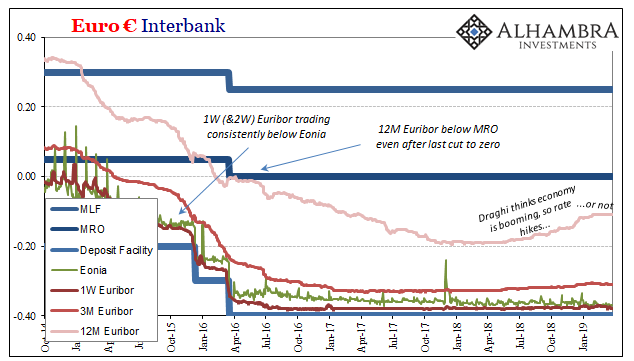

That assumption prevailed throughout much of the rest of 2013. Reflation #2 globally took hold registering in Europe as the continent pulled out of its re-recession. In euro money markets, further LTRO repayments along with rising optimism had pushed even short interbank rates (Eonia, Euribor) notably upward (shown above).

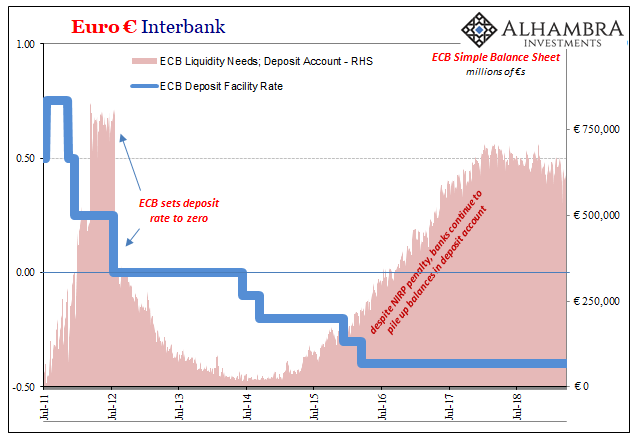

That all changed in June 2014. The ECB began to worry about the weak state of this “recovery”, a second one that was following along too shallow. Inflation wasn’t rising, either, and there were notable risks “overseas.” On June 18, Mario Draghi took a drastic step to ensure the economy wouldn’t slip: NIRP.

In raw mechanical terms, the ECB’s deposit rate was set to -10 bps. This applied to a large balance of funds European banks might maintain on account with the central bank. The idea was very simple: the central bank would expand the aggregate level of reserves through coming programs and to make sure banks didn’t simply hold them idle in this account they were to be penalized for doing so.

Either lend in the real economy or pay a price.

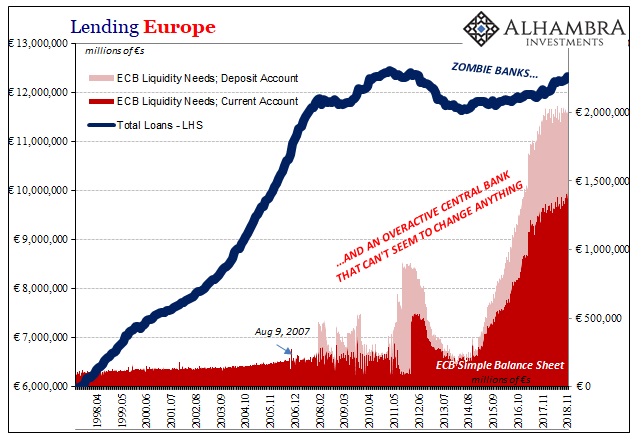

Previously in 2012 under both LTRO’s, Europe’s central bankers noticed how banks were piling up reserves in the deposit account. On July 11 that year, officials reduced the interest rate for it to zero. Funds flooded out (but were just transferred to the current account). It appears that the ECB was expecting the deposit account to be similarly empty by going to NIRP in 2014 (with a better overall outcome as banks this time would surely lend).

The penalty was doubled to -20 bps in October 2014. With the level of bank reserves growing under the combined LSAP’s – CBPP3, CBPP, and PSPP (QE) – the stockpile in the deposit account continued to rise even as this liquidity levy was increased to -40 bps by March 2016. This is all classified as ultra-loose monetary policy.

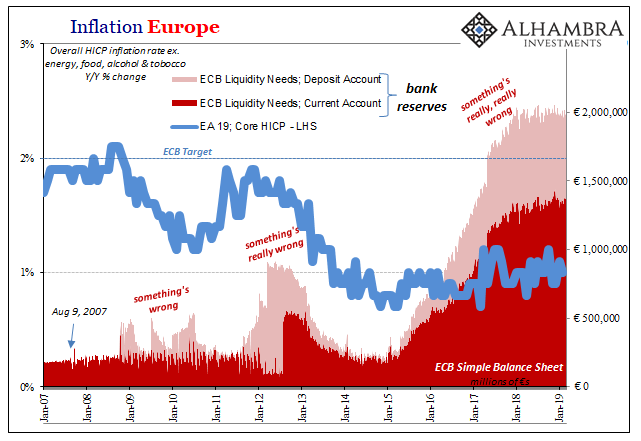

In 2017, the classification was upgraded to successful. Europe’s economy was booming, officials claimed, and by 2018 it was expected that all this emergency “stimulus” would be unwound. Only, as we know early in 2019, that’s not what is going to happen. Europe may already be in recession, or at least significant parts of it, and there is still growing concern (bund yields) there’s more negatives to come.

The result of all these years is what has to be one of the most inane, perfectly absurd conversations to ever take place in any central bank anywhere. The first paragraph of a suspiciously short article published in Reuters today describes our headless chicken:

The European Central Bank is studying options to lower the charge that banks pay on some of their excess cash as a possible way to offset the side-effects of its ultra-easy policy, two sources told Reuters.

It is so ultra-easy, this overall policy, that it hurts those involved in it. Too much, it appears.

We have to make sure banks lend from our reserves, so we will penalize them harshly for not doing what we want them to. They didn’t lend, so now we won’t penalize them as much because maybe our harm is too harmful, and by reducing the penalty that will get lending going again!

Just in time for another prospective recession.

The less corrupt among you might conclude that these people have no idea what they are doing. It all sounds very good on the chalkboard, in the regression analysis of complex yet oversimplified computer models. Give banks reserves and then punish them when they aren’t put to good use; problem solved.

The real world, however, is much more complicated – and in many ways far simpler. Maybe banks don’t want to use reserves because the implications, meaning risks, of doing so are perceived to be consistently much greater than the deposit rate NIRP penalty.

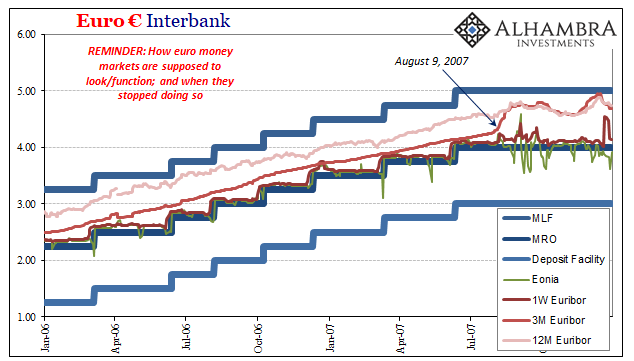

Thus, the real solution would instead be to figure out why banks are perceiving the world this way rather than rejiggering the NIRP nonsense one more time. And it really is nonsense. Euro money markets are an absolute mess, a disaster which begins to explain those very bank perceptions. Compare and contrast how money markets are supposed to function (pre-crisis) with what is happening now.

Monetary competence does not come easily to the modern central bank. It has morphed into expectations manipulation, which, ironically, requires everyone to believe that it is the most technically capable instrument for policy there is. This is why we are all taught from Econ 101 forward the near infallibility of the central banker, and also why at the very same time through experience and observation we see that’s just not the case.

They really have no idea what they are doing. The ECB is not a collection of newfound doves, they are chickens without their heads. Either way, it does not amount to anything good, and adds more weight to the considerable and growing list of everything bad.

Stay In Touch