Did Bear Stearns fail, or was it rescued? In March 2008, how you answered that particular question bled into your outlook on the rest of that year (and, apparently, forever after). If you chose to believe that the subprime crisis had been successfully handled by uneasy negotiation, the challenges everyone was confronting in early 2008 might not have seemed so insurmountable.

It was bad, sure, but the worst had been done and authorites rose to the occasion.

If, however, you took from Bear Stearns the possibility that “this” was only the beginning, that policymakers were faced with problems they didn’t even begin to understand, nothing much was left for surprise. I don’t just mean the technical specifics of why something like the Primary Dealer Credit Facility or dollar swaps were thought necessary, rather more big picture than all that.

The week after Bear’s demise/rescue was announced to the world, the FOMC gathered for its regular scheduled March 2008 meeting. There wasn’t really much talk about that one specific firm, though on the several occasions it was mentioned officials touched on what has come to define the world after this one investment bank was removed from the Wall Street ranks.

Here’s Bill Dudley, of all people, effectively characterizing why it’s not regulations but rather attitude that has plagued the global banking therefore monetary system ever since:

MR. DUDLEY. The fact that to the extent that there is stigma, they are not going to want to come, and that is going to reinforce the deleveraging process that is clearly under way, as is the fact that they just saw Bear Stearns go from a troubled but viable firm to a nonviable firm in three days. The lesson from that for a lot of firms is going to be, oh, I need more liquidity, I need to be less leveraged, and that lesson, from what happened to Bear Stearns, isn’t going to go away. [emphasis added]

Where Dudley, Bernanke, and the rest of the world’s central bankers went wrong was in misunderstanding the nature of what was right in front of them. Dudley gets this right, but adds the wrong context; it was rather more profound than he was making it out to be.

This wasn’t a short-term reassessment, as the FOMC was thinking, it was systemic re-evaluation, the permanent kind. In other words, Bear’s final chapter didn’t just cause firms to rethink their liquidity strategies for tomorrow, it caused every single global eurodollar bank to really consider, most for the first time, what was actually at stake.

Prior it was believed by everyone to be riskless returns. Bear taught them, via global dollar liquidity, it had really been the reverse.

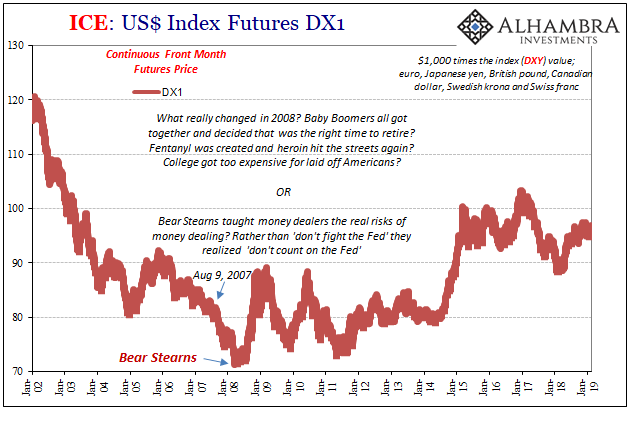

Bear wasn’t some subprime peddler, it was everyone. For the first time, liquidity risks had proven to be very real and immediate. Bill Dudley had earlier stated: “…the $2 per share purchase price for Bear Stearns was a shock given the firm’s $70 per share price a week earlier and its stated book value of $84 per share at the end of the last fiscal year.”

Why did DXY bottom out for good right then, or so many other indications point to the day of Bear’s announcement as the definitive break? Dudley provides our answer. Liquidity risk is paramount. Unfortunately neither he nor any other central banker could truly reckon its complete meaning.

Officials never saw it that way and still don’t; they were, and are, incapable of such a realization. Economies are, in the orthodox textbook, treated as closed systems. There is no global economy to a central banker.

Because of that, there is a role at least in expectations for “global growth.” In short, even if we policymakers think our local system is in trouble we can expect the other economies around the world to prevail and help us out. Ironically, in that same March 2008 FOMC meeting Ben Bernanke made that very claim, a single source of shining optimism that stands out even from Bear Stearns’ “rescue”:

CHAIRMAN BERNANKE. Exports continue to be an important source of final demand and will continue to contribute significantly to growth, although it’s possible that growth abroad may slow.

Within months, of course, “global growth” abroad would somehow subtract even more from everyone’s local output once everyone was sucked into the hellish monetary vortex. Global money, global economy. Massive problems in global money, it’s only a matter of time before the rest of the global economy gets whacked, too. There can be no decoupling.

Yet, over the many years since, the idea of global growth remains a powerful agent to set expectations. Decoupling is reborn every time monetary problems are. It happened in 2014, how when central bankers had trouble justifying their local optimism they would point to “global growth.” We may be struggling still, but someone out there isn’t and they will pull us out of the mess before it goes awry (again).

It didn’t end up that way in 2015, obviously, but that didn’t stop an even more fanciful version from being sloganeered just a few years later. I wrote about this “globally synchronized growth” in June 2017, just as it was getting started in its fourth narrative form:

One of the offshoots of that vagueness was “global growth”; as in “the global economy is improving” so the local one will certainly follow. In many ways this was even more convenient because of its impreciseness. It essentially established an unfalsifiable premise: somewhere out there in the vast world there is growth, so soon there will everywhere be growth. It’s not logic so much as desperation.

And it works both ways. That is, when things appear to be going the right way as in 2014 or 2017 global growth is a reason it should stay the right way. And when things start to go the wrong way, as in 2018, you can blame the sudden and unexpected lack of global growth for befouling a local system otherwise performing admirably. This was Janet Yellen’s message in 2015, the “overseas turmoil” which the US economy abruptly had to deal with.

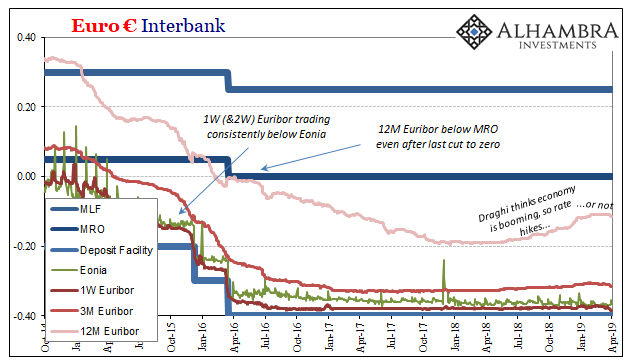

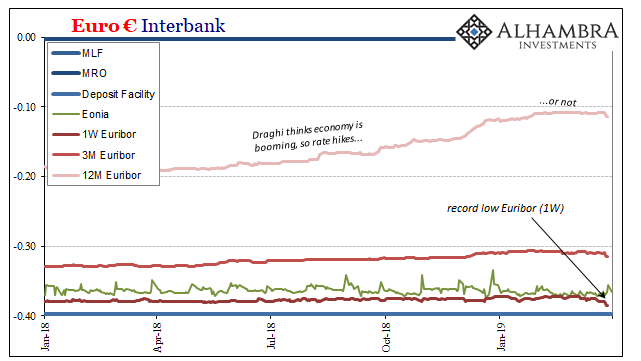

It is now Mario Draghi’s message in 2019 as he tries to explain how one year Europe was booming in near epic fashion and the very next it is on the verge of, if not already partway plunged into, contraction.

The last year has seen a loss of growth momentum in the euro area, which has extended into 2019. This has been predominantly driven by pervasive uncertainty in the global economy that has spilled over into the external sector. So far, the domestic economy has remained relatively resilient and the drivers of the current expansion remain in place.

The domestic European economy is awesome, thanks to Draghi, but the “external sector” crippled by “pervasive uncertainty” is in danger of spoiling everything. The true miracle of global growth; it can be whatever your narrative needs it to be.

European money markets aren’t buying it, not that anyone should have expected they would. One-week Euribor set a record low last week. The 12-month and 3-month rates which had perked up slightly taking Draghi at his 2018 word about how rate hikes were on the horizon, have slumped again. Fool me once with global growth…

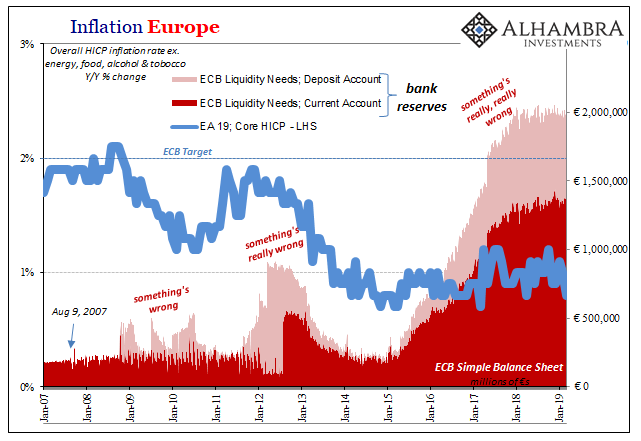

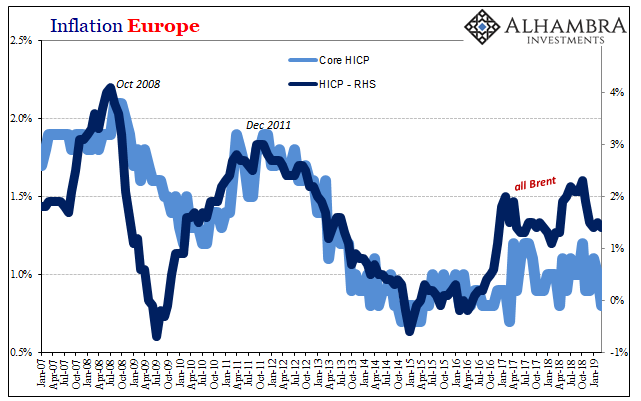

It is, therefore, no mystery as to why no matter what the ECB does or doesn’t do nothing ever changes. Not really, certainly not meaningfully. It’s not within the central bank’s power. European inflation in March 2019 was marked downward again, the core HICP rate just 0.8% and closer to a record low than anything resembling even the start of the boom Draghi was talking about not all that long ago.

It is, put together, the two factors central bankers aren’t able to comprehend. And these may be the only two factors that matter. Bear showed the system’s necessary banks the real downside to liquidity, eurodollar liquidity (in all its various degrees of dark leverage, dark or shadow money forms). “Global growth” means how a global monetary system wrecks every idea about closed systems with central banks central to each (a major theme of my presentation at Harvard this past weekend).

This should have been apparent from the very first. I wrote on the ten-year anniversary of August 9, 2007, the significance of what happened that day which would lead into Bear’s fateful participation. “These were European money market funds domiciled in France and Liechtenstein sponsored by a French bank invested primarily in US$ ABS to beat euro money market rates. What matters about geography here?”

The banks are broken and this worldwide economy needs them not to be. That didn’t change in 2017, just like it didn’t in the weeks and months and years following Bear Stearns’ “rescue.”

Stay In Touch