In early February 1994, Alan Greenspan’s Fed would begin to raise the federal funds rate target for the first time in five years. Not since February 1989 had the FOMC thought economic conditions warranted an increase. In between, the 1990-91 recession which wasn’t especially bad, certainly not by contemporary standards set by the contractions in the seventies and early eighties.

Still, many were unprepared for an extra-aggressive Greenspan determined to make interest rate targeting stick. When there is money in monetary policy, you know just what to do when. Expectations management, on the contrary, requires more blunt force used very publicly.

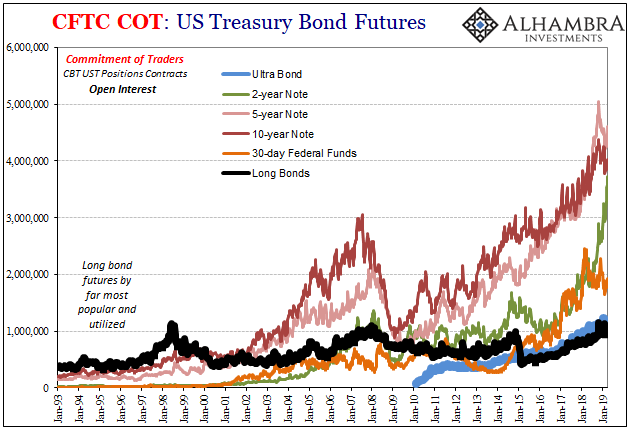

Back then, the futures market was very fragmented. There was no single one. What was available was basically long bond futures and little else where you could go for protection.

The week of that first hike, there was open interest of 205 thousand contracts for the 5-year space, 259 thousand at around the 10-year, and just 36 thousand near the 2s. There wasn’t even 9 thousand in 30-day federal funds futures.

By contrast, there were more than 400 thousand contracts open for the long bond (defined back then as any UST having a maturity greater than 15 years in the same month as contract delivery). And that was just what was trading in Chicago at the Board of Trade. There were thousands more at the mid-America Commodity Exchange, and even a few thousand open on New York’s Cotton Exchange.

Consolidation of these derivatives markets unlocked massive growth potential and an explosion in use. It helped, obviously, that the eurodollar system’s increasing depth and reach had meant already existent demand for these products. The exchanges may have started out in commodities, quite naturally they became more and more devoted to financial futures more than anything else.

The financialization of the world, so to speak, driven by monetary and financial evolution.

In terms of trying to determine a useful signal from these markets, open interest specifically, it makes for a noisy process.

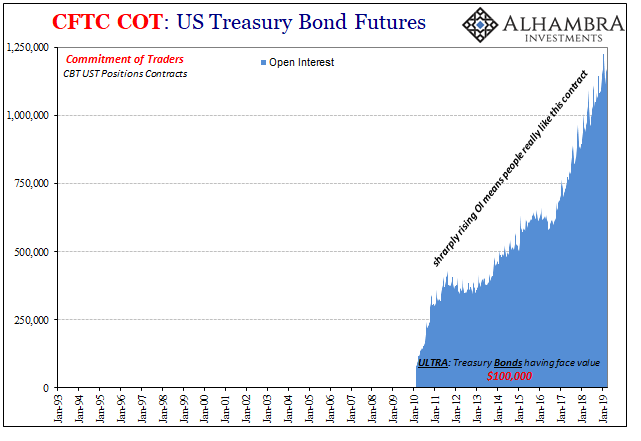

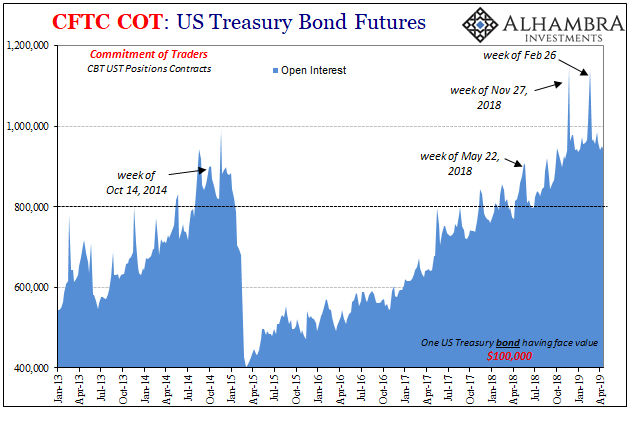

This is why I stick to the long bond. It is the exception to the rule that nothing stands still. Interest, meaning open interest, has been pretty darn constant for more than a quarter century. Unlike the futures for the other tenors, the long bond is what it has always been.

And that seems to be liquidity risk protection. It calibrates near perfectly.

When Alan Greenspan set about to raise interest rates ten years after ‘94, in June 2004, by then the landscape had changed. There were almost 1.3 million contracts for the 10-year and 1.1 million more for the 5-year. The long bond was still right around 500 thousand.

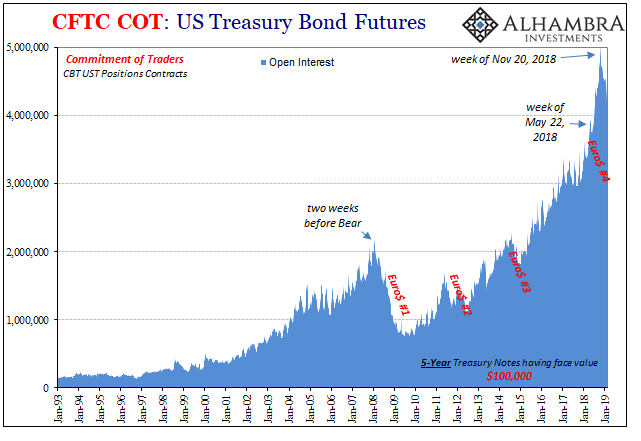

By December 2015, when Janet Yellen meekly tried her hand at these “rate hikes”, there had come to be a million in 2-year contracts, nearly 2.6 million in 10-years, and 2.4 million of 5s. There were even 637 thousand contracts open for something called the ultra-bond launched in 2010 (UST’s with at least 25 years left to maturity in the month of delivery).

In just the three years since then, contract volume has nearly doubled again. There’s today about 4 million open in 2s, more than 4 million in 10s, and what is now the most popular more than 4.5 million in 5s.

And the long bond remains pretty much unto itself. The lack of true growth a benefit to what we seek for information. The big financial players seem to like this one type of contract the most when things are about to go down (the bad way).

This isn’t to say, however, there aren’t potential clues and corroboration in the other more widely used futures types. They just aren’t so straightforward as it appears to be here.

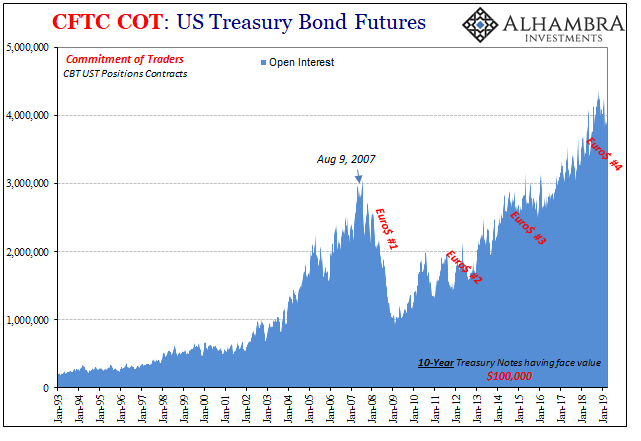

The 10s, for example, seem to display a similar if somewhat inverse signal. In the intital stages, open interest in these contracts falls when the that for the long bond is rising. The emphasis for more OI are likely more about growth in the overall futures business as much as inflation expectations. Seemingly very little about liquidity concerns (even collateral).

There are also technical considerations here, too, an obvious quarterly pattern which you have to take into account for reasons that have nothing to do with our purposes.

In other words, unlike the bond contracts the rise in popularity of the 10-year note futures cannot be so easily distilled into the one element. It may be that overall the remarkable gain in open interest since 2009 is more about the way the market works than the way the market is thinking.

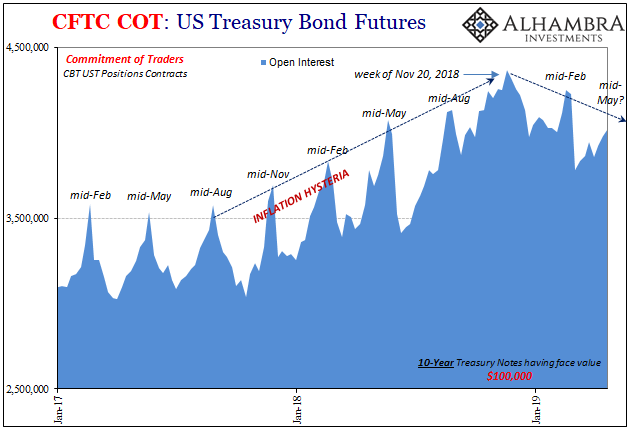

And it may also be true at the same time how over the last two years the one signal has become more aggressive than the other factor. It does seem to be that 10-year UST futures contracts were becoming more popular for possible inflation hedges after the middle of 2017.

It may also be true that is no longer the case after the last week in November 2018. I doubt that’s coincidence, but it’s not a straight shot given so many other factors driving contract dynamics. Fortunately, our analysis isn’t being conducted in isolation.

There is a similar pattern to the 5s. Interest in this part of UST curve via the futures market has simply exploded. More like the 2s, here you are hedging Janet Yellen and Jay Powell as much as economic perceptions. Much less purely liquidity or direct economic considerations.

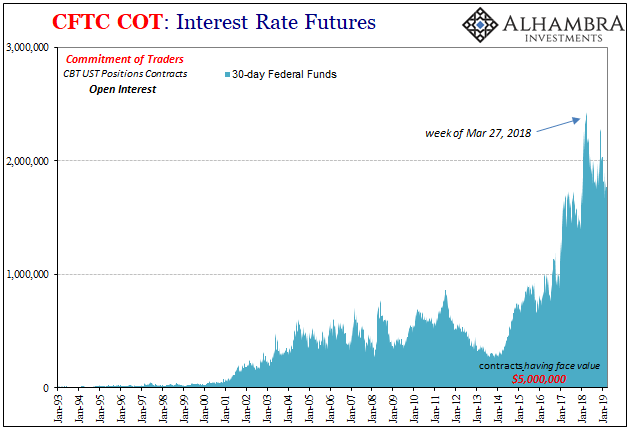

Even as the federal funds market itself is practically nothing anymore, open interest in 30-day interest rate futures tied to the rate has likewise exploded for reasons that have nothing to do with the mechanics of the federal funds market. The massive expansion in futures contracts since Yellen’s first ill-advised misstep in December 2015 is the whole financial world hedging against higher policy-driven rates in general.

These have been notably less popular since just before April 2018. Another way of saying that is, going back to the EM/dollar/collateral eruption toward the middle of last year there hasn’t been nearly as much overall demand for futures contracts tied to the federal funds rate. It may be for other reasons, but, again, in concert with everything else there does seem to be some meaning behind the futures market becoming less and less interested in the FOMC.

What we are trying to get at is confirmation of the bond market. Nominal yields are down again recently but not by all that much. Economists expect yields to surge again as what they see as a growth scare gets put behind. The entirety of the futures market, however, judging by open interest, would suggest a continuing bias toward the deflationary side, less inflation more liquidity hedging and whatnot, but not yet another rush all the way in that direction.

For the long bond, demand for futures contracts remains unusually high, still about 950 thousand, but not surging like it did in November just before the sharp drop in yields and again in February prior to the second outbreak of the same thing.

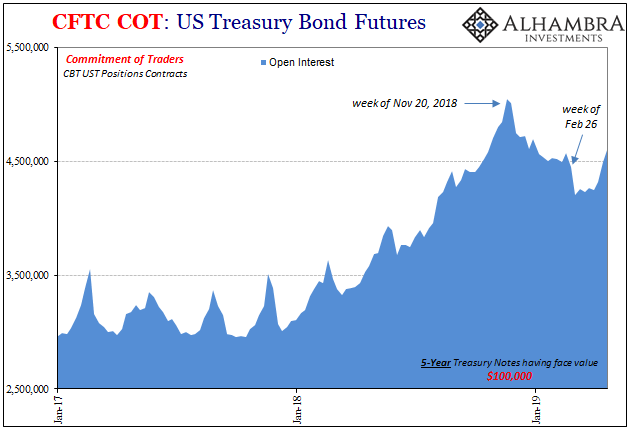

Meanwhile in the 10s, OI seems to be on track for a lower mid-quarter peak consistent with less inflation hedging, but we won’t know for sure for several more weeks. At the 5-year, OI is up again rather than declining as it had during those same yield curve bending periods.

This isn’t the recipe for higher rates, and it’s also not the stance from which we would expect the next plunge in yields. That could all change, and when it does there is value in broad corroboration. Watch the OI’s.

Stay In Touch