Yesterday, the FOMC altered its view of household spending and business capex. It wasn’t a huge difference, they never are. Figuratively, these sorts of downgrades are little by little even though if things were ever to go the right way the language upgrades wouldn’t be subject to so much reservation.

There isn’t much in the official statements anyway, just a few sentences. Still, the Economists at the Fed felt it necessary to admit consumer and business spending “slowed in the first quarter.” That’s not good.

Not to worry, Powell says at his press conference, because it’s all transitory. Behind that otherwise alarming shift is the labor market. “Job gains have been solid, on average, in recent months, and the unemployment rate has remained low.” See? So long as the labor market is this way, any sort of weakness can only be a minor speedbump on the road to full recovery.

The unemployment rate strikes again. As I wrote also yesterday:

Jay Powell looks at the unemployment rate and from it alone he, like Yellen and Bernanke, concludes a whole bunch of sweeping generalizations that are about to blow up in his face. At less than 4%, to officials it must mean: the financial system is totally healed; the economy is fully mended; and all because central bankers know what they are talking about. QE was genius.

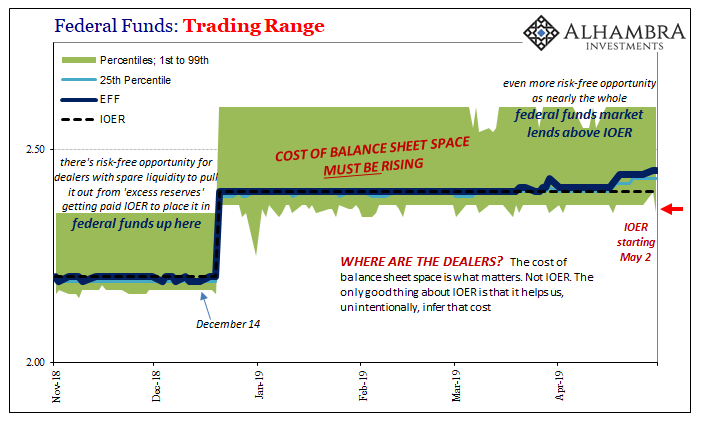

We already know about the first one. Three technical adjustments to IOER, the latest to be instituted today, all intended to placate growing embarrassment. Federal funds is the one thing the Federal Reserve is supposed to easily handle blindfolded. People should never be talking about it, but lately even the mainstream financial press is being forced to cover the topic for reasons nobody quite understands.

That’s how much the myth of the maestro lingers on against all evidence and history.

What it says is that the financial system may not be healed after all. Even this late in the game, EFF is showing up what is merely an assumption made on everyone’s behalf. The central bankers all claim things were made right after 2008, but why does anyone believe them?

It’s supposed to be a matter of technical expertise. These guys should know because that’s their job. So, when EFF comes along and exposes such gross incompetence; holy sh&%.

That’s just the first step. The bigger issue is the unemployment rate. If EFF opens the door to the economic justification for doubting the number, the lack of corroboration actually serves as evidence against it. It’s the one actually consistent story top to bottom.

The latest batch of data from the BLS is totally damning. Not only does the LABOR SHORTAGE!!! fail to appear one quarter into 2019, there are many signs of serious deterioration in the labor market. The Fed deploys the unemployment rate like some medieval incantation to ward off pessimistic spirits rather than it being solid analysis.

Once more the mainstream narrative: years of an unbelievably low unemployment rate means an exceptionally tight labor market, one where workers are so scarce, this labor shortage, that businesses fight for them. Wages have to rise so very quickly as a result, pushing up first labor costs to businesses who then pass them along to consumers in the form of consumer price inflation.

We already know, and the Fed has already admitted, the last part isn’t happening. They’re now trying to blame airline ticket prices and financial services in the same way they blamed wireless data plans a few years ago. There’s always something in the way for these people.

Even if that was all true, then we’d still see wages rising. There isn’t some kind of transitory factor which would get in the way of exploding pay. A labor shortage works on simple supply and demand, where if the demand is rising sharply and supply remains restricted the price can only go in one direction.

And the BLS says it is going the other way. Not only is there no labor shortage showing up in wage data for 2018, in 2019 there is the hint of downturn maybe recession. As you go through the series, it only gets worse.

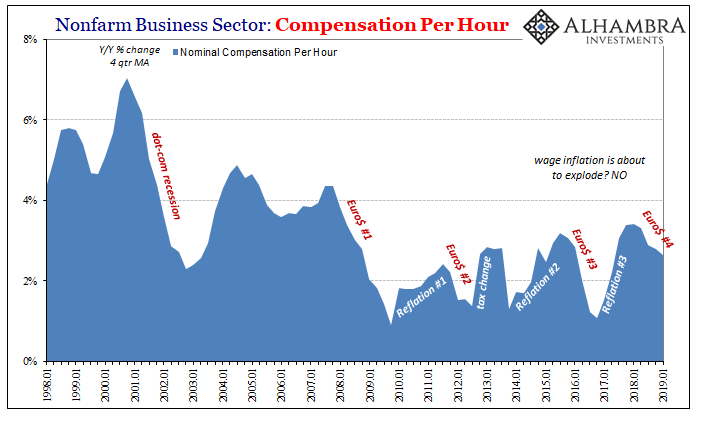

Nominal Compensation per Hour is exactly where a labor shortage would show up. Whether it is inflationary or not doesn’t matter. Businesses pay more for scarce workers, so this is the first place to start.

Nominal compensation increased 2.6% per hour (annual rate) in Q1 2019 from Q4 2018. That’s not good. The 4-quarter average, this series is somewhat noisy from quarter to quarter, is just 2.5%. That’s down from 4.0%, a peak registered when? Like so many, many economic indications from all around the world, the top falls conspicuously at the third quarter of 2017. What happened in Q4 2017?

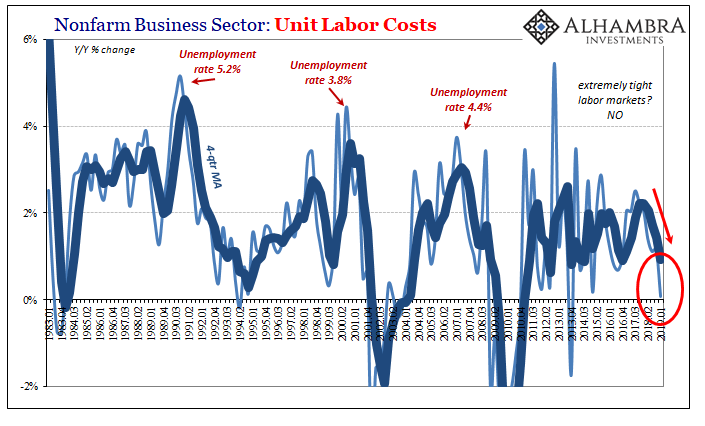

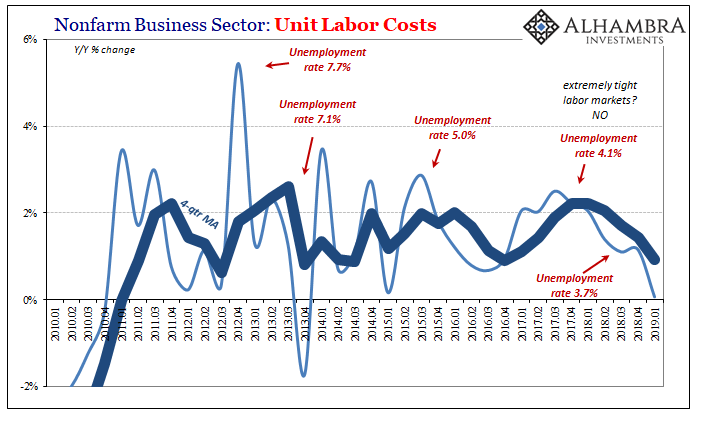

Looking at the problem from the perspective of Unit Labor Costs, more bad news for Jay Powell (and the global economy). For reasons I doubt he could begin to explain given an unemployment rate at or less than 4% for over a year, Unit Labor Costs in Q1 2019 were somehow about the same as they were in Q1 2018. Up just 0.1% year-over-year, that’s really not good.

Peak growth in Unit Labor Costs? Also Q3 2017. Euro$ #4 more and more pops out in the labor market all across 2018, meaning 2019 started much, much differently from the way it was described.

If businesses are actually being more cautious about labor costs, as the data here demonstrates, then it makes sense they’d have done the same in capex. That sort of uncertainty would certainly translate into a more cautious consumer. Americans may like to spend, but they do tighten up when they’re not sure about their own work prospects.

The final piece of evidence puts the exclamation point on it.

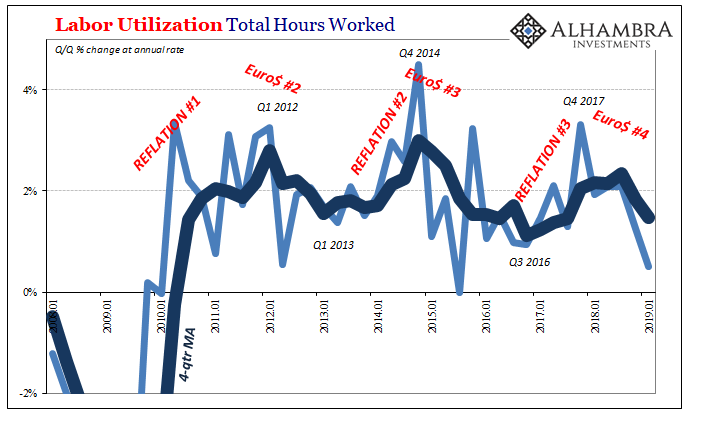

According to the latest BLS estimates, total hours worked rose just 0.5% (annual rate) in Q1 above Q4. The labor market practically came to a screeching halt in the first quarter in a way it hasn’t since the third quarter of 2015. That’s a pretty startling comparison, given what happened three and a half years ago.

It also corroborates the shocking income numbers reported by the BEA over the past few months. Less hours plus slower not exploding wages equals less income.

How can the FOMC claim it’s all just transitory?

Again, the data here regarding the US labor market is consistent in each series. It’s as if it has been slowly strangled for a year if not a year and a half already. And it is this way all over the world, a growing downturn that’s already pretty long and established.

In Janet Yellen’s dictionary that may be transitory, but over here in reality it’s something to take very seriously.

Not only is there still no evidence for a labor shortage, this year is shaping up more and more on the downside all the way to the economic foundation. If the FOMC is counting on the labor market, then the actual labor market data says they should only count on some form of downturn.

Euro$ #4 is all over the Federal Reserve: from federal funds to the unemployment rate.

Rate cuts really do make sense; not that they will help but that this becomes so obvious even Jay Powell will, kicking and screaming, acknowledge he has no other choice. Sooner than you might think.

Stay In Touch