GDP was better than 3% in the first quarter, the payroll report was greater than +250k, and the unemployment rate was the lowest in fifty years. The economy in the US must (still) be booming.

But:

The vast US services sector recorded a surprise slowdown in April, according to the Institute for Supply Management’s latest survey.

The group said Friday its non-manufacturing index slipped to 55.5 last month, down from 56.1 in March and confounding economists who expected the gauge would jump to 57. It also marked back-to-back months in which the index posted its weakest level of growth since August 2017. A reading above 50 indicates expansion.

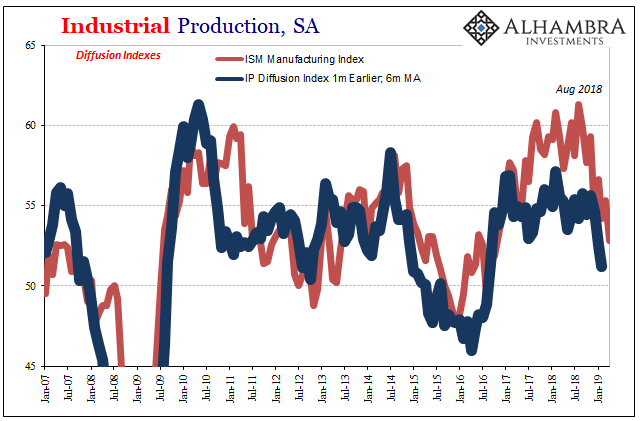

The ISM’s Manufacturing PMI has been dropping since last summer. Just two days ago, the same outfit reported that this other index was the lowest in thirty months.

Why is weakness or even weakening “a surprise?” This is, after all, what markets have been pointing toward for more than a year. Eurodollar futures and UST’s still suggest rate cuts on the horizon, even after GDP and this latest Payroll Friday.

These are, from the mainstream perspective, the wrong markets, though. Stocks are at record highs having completely erased all that December stuff. Overblown worries got the best of everyone and we can finally put it all behind us. Jay Powell said so.

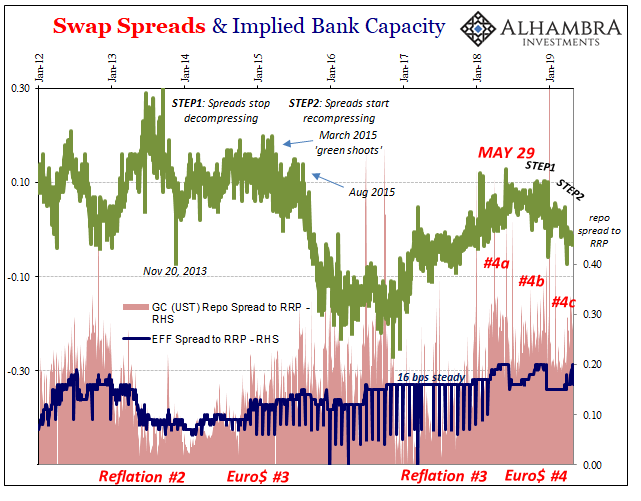

This is why EFF matters. If you really believe all that, and you really want to believe Powell, then you better have an explanation for why this irrelevant market is garnering so much deserved attention and embarrassing the FOMC. It was ignored for the better part of a year until every excuse thrown at it was debunked by how it has kept on going and going.

They don’t yet have an answer for it. And if the one they ultimately settle on is a standing repo facility, that’s actually a bad sign. Why, after planning for years and years, would the Fed with the economy supposedly booming need to come up with still more tools for its toolkit? Something just doesn’t add up.

Funny how the more EFF gets pulled further out of line the more the economic “surprises” to the downside. As if there might be a connection.

Stay In Touch